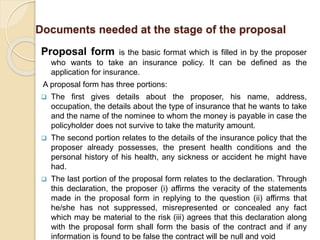

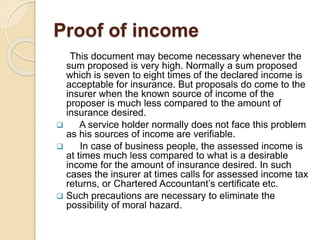

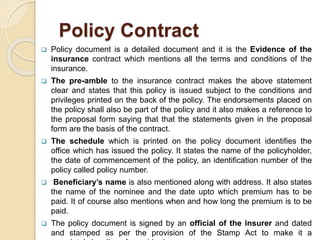

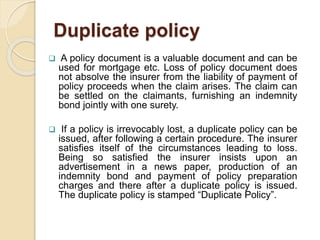

This document discusses various insurance documents needed at different stages of a life insurance policy. It explains that a proposal form is needed initially to apply for a policy and provide details. If approved, a policy document is issued which serves as the contract. Other documents include premium receipts, endorsements for any policy changes, proof of identity and age. Documents are also needed to make nominations, assign policies, or get duplicates if originals are lost. Renewal notices are sent as a courtesy to help policies stay active. Overall, documentation establishes the agreement and protects both insurer and insured.