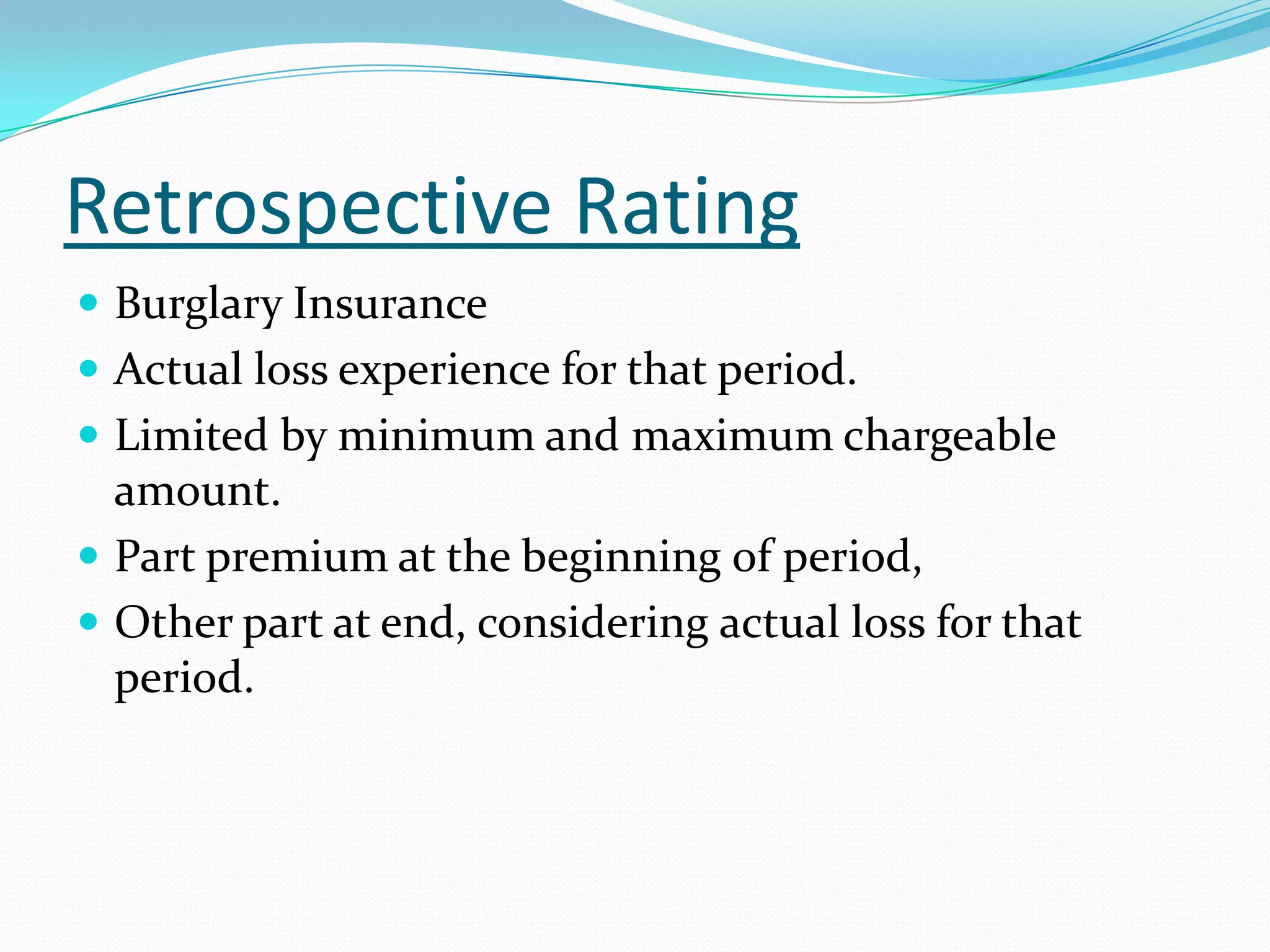

Property & Liability insurance involves the equitable transfer of risk, where many policyholders share the financial losses of a few through premium contributions. P&L insurance company investments total around $789 billion, with most assets invested in securities to pay claims if needed. Net premiums written for all lines were around $300 billion. P&L policies are short-term, and claims payments can vary greatly depending on catastrophes. Various rating systems like schedule, experience and retrospective ratings adjust premiums based on risk factors of individual policies.

![Chapter 1[definition and nature of insurance]](https://cdn.slidesharecdn.com/ss_thumbnails/chapter1definitionandnatureofinsurance-150912031826-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)