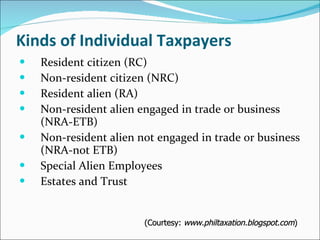

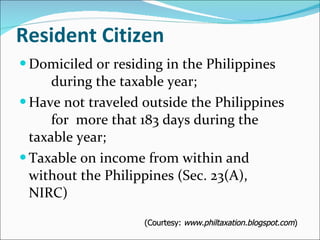

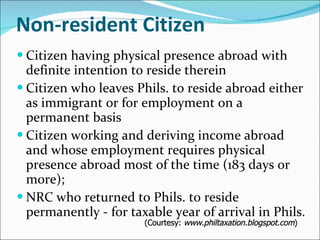

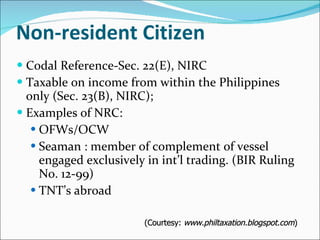

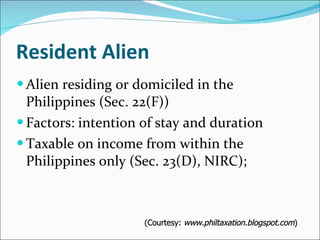

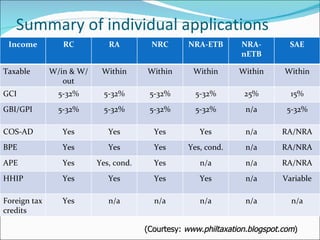

The document outlines different types of individual taxpayers in the Philippines based on citizenship and residency status, including resident citizens, non-resident citizens, resident aliens, and various categories of non-resident aliens. It discusses how tax treatment varies between these groups in terms of taxable income, applicable tax rates, allowable deductions, and other tax considerations. The classifications are important because an individual's tax obligations depend on whether they are considered a resident or non-resident and whether any tax treaties apply based on their citizenship.

![Philippine%20taxation..[1]](https://cdn.slidesharecdn.com/ss_thumbnails/philippine20taxation-150909111327-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)

![Taxation lectures[1]](https://cdn.slidesharecdn.com/ss_thumbnails/taxation-lectures1-101011032905-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)