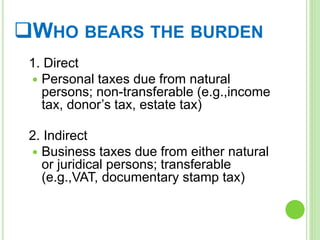

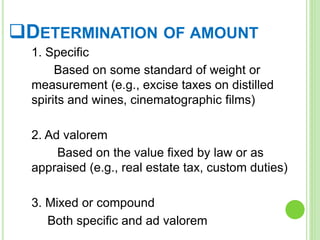

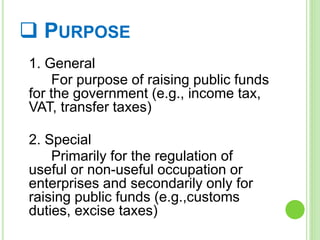

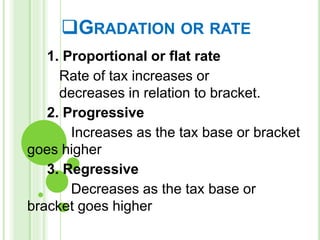

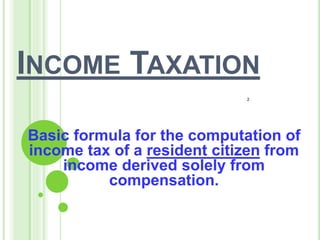

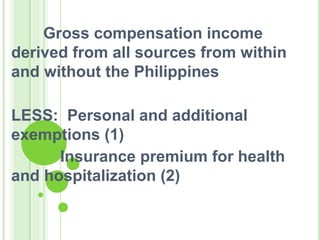

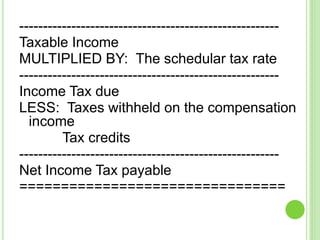

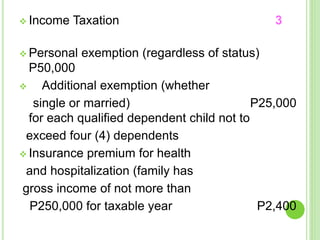

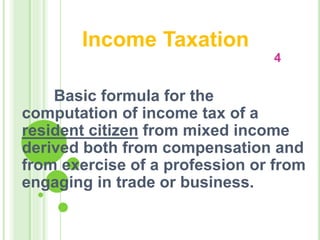

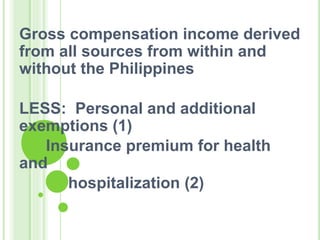

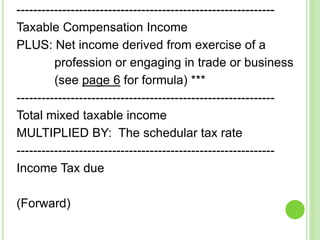

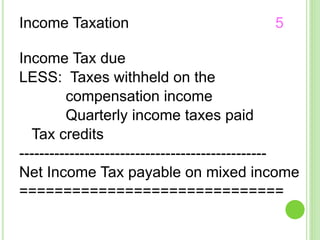

This document provides an overview of Philippine taxation. It begins with definitions of taxation and discusses principles like the necessity of taxes to fund government. It describes different types of taxes according to criteria like subject, burden, determination of amount, and purpose. Key points include taxes being compulsory, levied by the state for public purposes, and classified as direct or indirect. The document also covers tax system objectives, stages of taxation, laws, and the power and limitations of taxation. It discusses concepts like double taxation, tax exemptions, and interpreting tax laws. The last sections focus on income taxation principles and computing individual income tax.

![[] In Luke, 20:22-25, Jesus was

asked by the Pharisees, “Tell us,

is it against our law for us to pay

taxes to the Roman Emperor or

not?”

Taxation is in Accord with

the Bible](https://image.slidesharecdn.com/philippine20taxation-150909111327-lva1-app6892/85/Philippine-20taxation-1-6-320.jpg)

![DEFINITION

[] An inherent power of

sovereign

[] Imposes burden upon

persons and property

[] Raises revenues for

public purposes](https://image.slidesharecdn.com/philippine20taxation-150909111327-lva1-app6892/85/Philippine-20taxation-1-9-320.jpg)

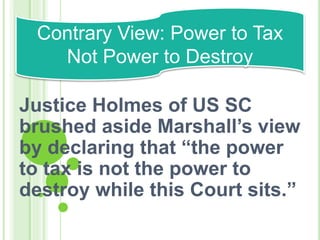

![[] A valid tax should not be judicially

restrained merely because it would

prejudice taxpayer’s property.

[] An illegal tax could be judicially

declared invalid.

Reconciliation of

Marshall’s View with

Holmes View](https://image.slidesharecdn.com/philippine20taxation-150909111327-lva1-app6892/85/Philippine-20taxation-1-12-320.jpg)

![THEORY AND BASIS OF

TAXATION

[] Necessity theory

[] Benefits-Protection

theory](https://image.slidesharecdn.com/philippine20taxation-150909111327-lva1-app6892/85/Philippine-20taxation-1-13-320.jpg)

![OBJECTIVES OF

TAXATION

[] Revenue

[] Regulatory

[] Compensatory](https://image.slidesharecdn.com/philippine20taxation-150909111327-lva1-app6892/85/Philippine-20taxation-1-14-320.jpg)

![STAGES OF TAXATION

[] Levy or imposition of tax

[] Collection (including

assessment)](https://image.slidesharecdn.com/philippine20taxation-150909111327-lva1-app6892/85/Philippine-20taxation-1-15-320.jpg)

![[] National Tax Laws

NIRC and Tariff and Customs Code

[] Local Tax Laws

Local Government Code on Local Tax

Ordinances

[] Miscellaneous Tax Laws

Philippine Tax Laws](https://image.slidesharecdn.com/philippine20taxation-150909111327-lva1-app6892/85/Philippine-20taxation-1-16-320.jpg)

![CHARACTERISTICS OF

TAXES

[] An enforced contribution

[] Generally payable in money

[] Proportionate in character

[] Levied on persons, property or exercise

of a right or privilege

[] Levied by state having jurisdiction

[] Levied by legislature

[] Levied for public purpose

[] Paid at regular a periods or intervals](https://image.slidesharecdn.com/philippine20taxation-150909111327-lva1-app6892/85/Philippine-20taxation-1-19-320.jpg)

![BASIC PRINCIPLES OF A

SOUND TAX SYSTEM

[] Fiscal adequacy

[] Administrative feasibility

[] Theoretical justice](https://image.slidesharecdn.com/philippine20taxation-150909111327-lva1-app6892/85/Philippine-20taxation-1-20-320.jpg)

![Sources

[] Philippine Constitution

[] Existing tax laws of the Philippines

(National, Local and Miscellaneous

tax laws)

Tax Laws, In

General](https://image.slidesharecdn.com/philippine20taxation-150909111327-lva1-app6892/85/Philippine-20taxation-1-27-320.jpg)

![NATURE

[] Not political in character

[] Civil in nature and not subject

to

ex post facto law prohibition

[] Not penal in character](https://image.slidesharecdn.com/philippine20taxation-150909111327-lva1-app6892/85/Philippine-20taxation-1-28-320.jpg)

![[] Tax evasion

[] Tax avoidance

Escape from

Taxation](https://image.slidesharecdn.com/philippine20taxation-150909111327-lva1-app6892/85/Philippine-20taxation-1-29-320.jpg)

![Taxation lectures[1]](https://cdn.slidesharecdn.com/ss_thumbnails/taxation-lectures1-101011032905-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)