Downloaded 202 times

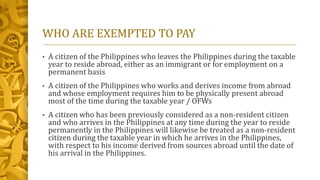

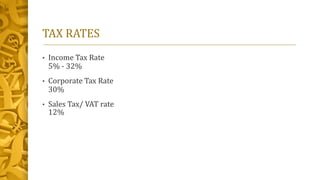

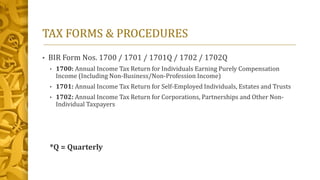

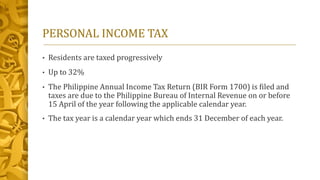

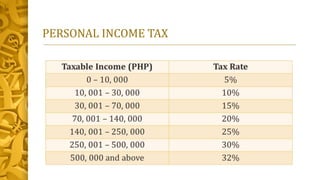

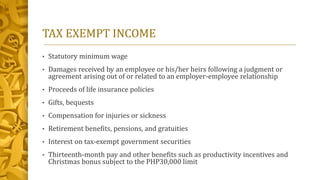

Philippines has an income tax system that taxes residents and citizens on income earned within or outside the country, as well as taxes non-residents on income from Philippine sources. Tax rates range from 5% to 32% for individuals and 30% for corporations. Common tax forms include BIR Form 1700 for individual compensation income and BIR Form 1701 for self-employed individuals. Some exemptions include statutory minimum wage, damages from employer lawsuits, life insurance payouts, and some retirement benefits.

![Philippine%20taxation..[1]](https://cdn.slidesharecdn.com/ss_thumbnails/philippine20taxation-150909111327-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)

![Taxation lectures[1]](https://cdn.slidesharecdn.com/ss_thumbnails/taxation-lectures1-101011032905-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Culture of Poverty in the Philippines [REPORT]](https://cdn.slidesharecdn.com/ss_thumbnails/assignment2-povertyinthephilippinesjariyapornseenay-181210133033-thumbnail.jpg?width=640&height=640&fit=bounds)