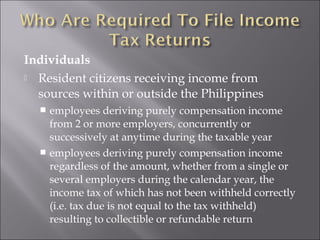

This document discusses key concepts related to income tax in the Philippines. It defines income as profit, gains, or cash flows received within a specified period. Income can come from employment, investments, or business operations. The Philippines uses both a global and schedular system for taxing income. Under the global system, all categories of income are taxed the same. The schedular system taxes different income types differently. Individuals are taxed based on their residency and source of income. Corporations are taxed differently depending on if they are domestic or foreign. The goals of income tax include generating government revenue and offsetting other taxes in a progressive manner.

![Taxation lectures[1]](https://cdn.slidesharecdn.com/ss_thumbnails/taxation-lectures1-101011032905-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Philippine%20taxation..[1]](https://cdn.slidesharecdn.com/ss_thumbnails/philippine20taxation-150909111327-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)