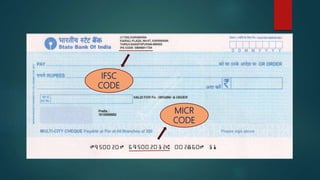

The Indian Financial System Code (IFSC) is an 11-character alphanumeric code assigned to each bank branch by the Reserve Bank of India, facilitating electronic fund transfers through NEFT, RTGS, and IMPS. The code helps identify banks and branches during transactions and is critical for transferring money without limitations. Users can find an IFSC code by selecting their bank name, state, district, and branch.