Downloaded 1,017 times

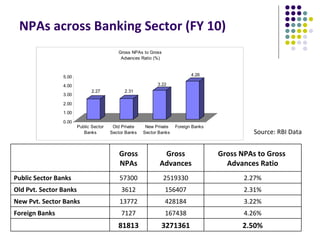

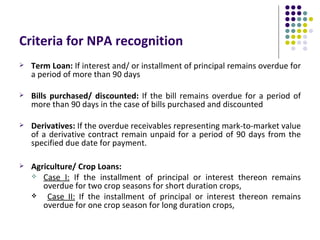

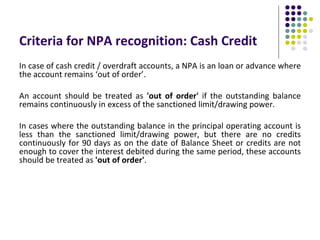

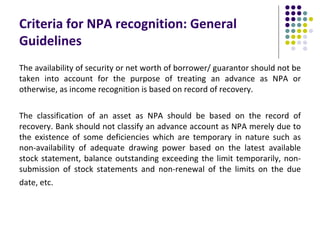

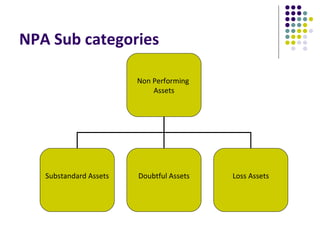

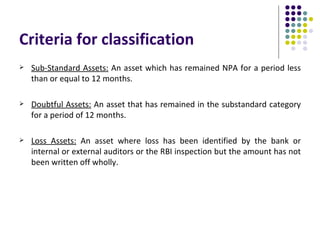

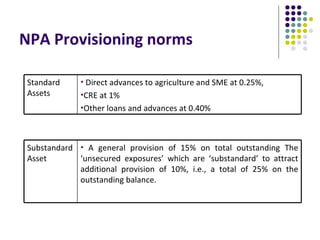

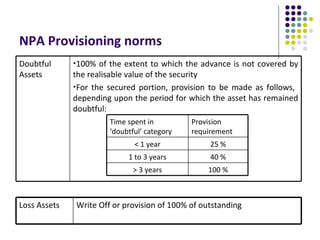

The document discusses Non-Performing Assets (NPAs) in the Indian banking sector. It defines an NPA as an asset that ceases to generate income for the bank. It provides data showing that public sector banks had the highest NPA ratio in FY2010 at 2.27%, while foreign banks had the lowest at 4.26%. The criteria for classifying different types of loans as NPAs, including term loans, cash credits, project loans and more, are explained in detail. NPAs are further classified as substandard, doubtful or loss assets based on the period of delinquency. Banks are required to make provisions against NPAs as per RBI guidelines.