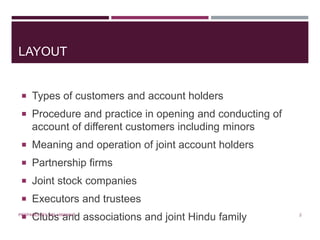

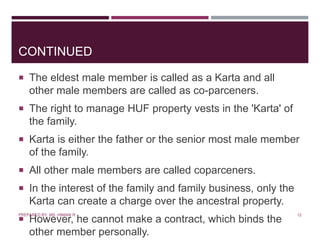

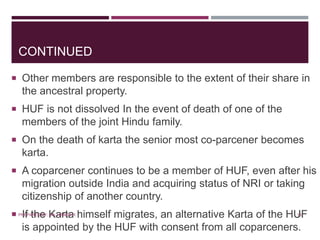

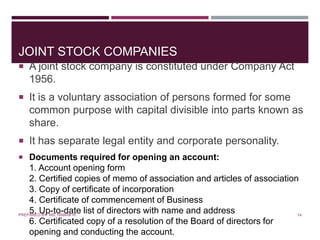

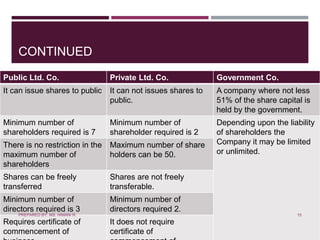

This document discusses various types of customers and account holders that banks deal with. It describes ordinary customers as well as special customers like minors, partnership firms, joint Hindu families, joint stock companies, and more. For each type of special customer, it provides details on legal considerations for opening and operating accounts, required documents, authorized signatories, and other precautions banks must take. The document aims to outline procedures and legal compliance for properly handling different customer accounts.

![Ch04 evans mcq_aise[1]](https://cdn.slidesharecdn.com/ss_thumbnails/ch04evansmcqaise1-160126040309-thumbnail.jpg?width=640&height=640&fit=bounds)