Downloaded 559 times

The document discusses letter of credit, which is a payment mechanism in international trade. It defines key terms like applicant, beneficiary, issuing bank. It describes different types of letters of credit like revocable, irrevocable, confirmed, sight, usance, back-to-back and transferable letters of credit. It also discusses standby letters of credit and fees involved like opening charges, retirement charges. Finally, it mentions some common uses of export letters of credit.

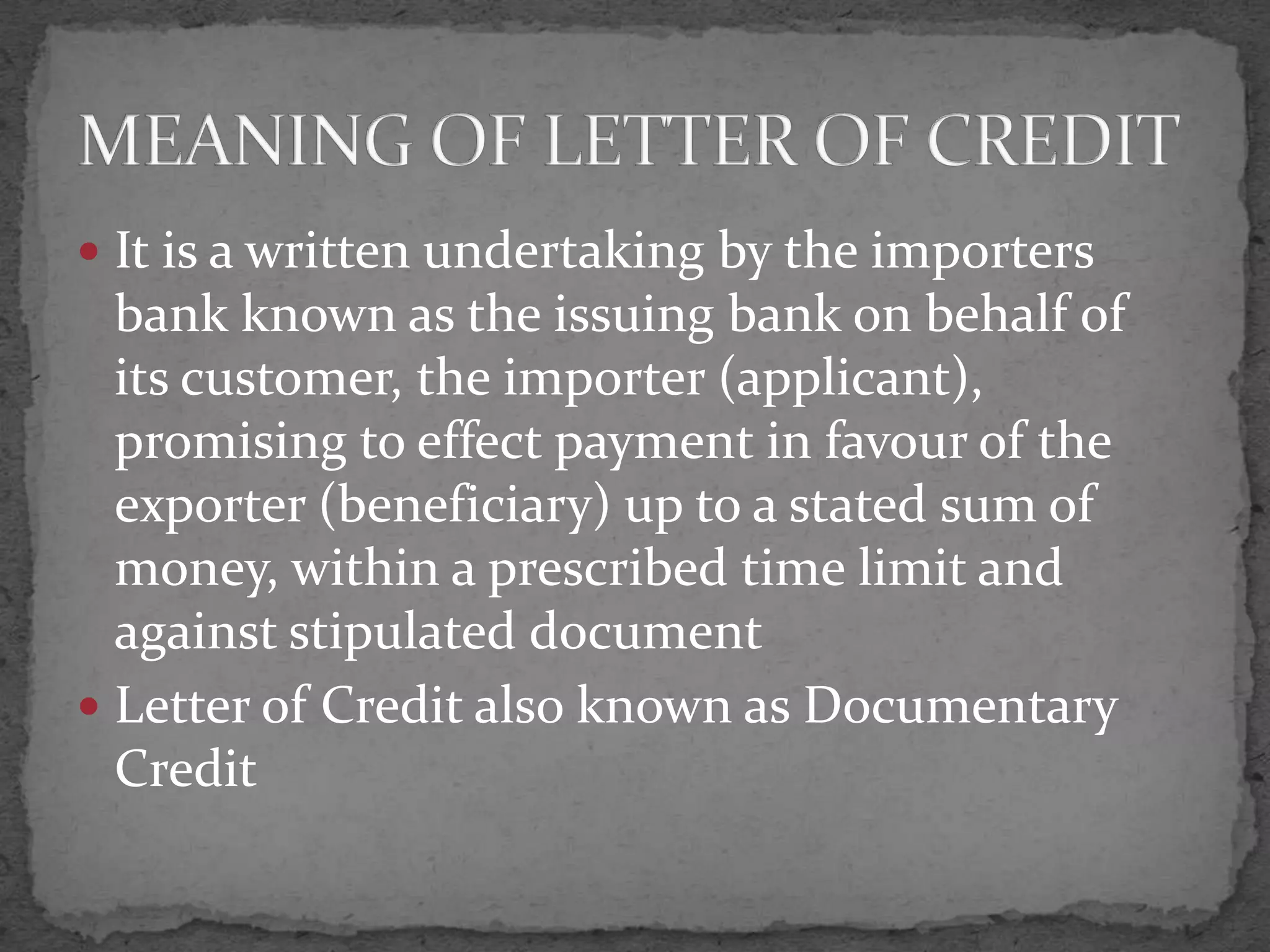

Overview of Letter of Credit as a financial instrument used in international trade for securing payments.

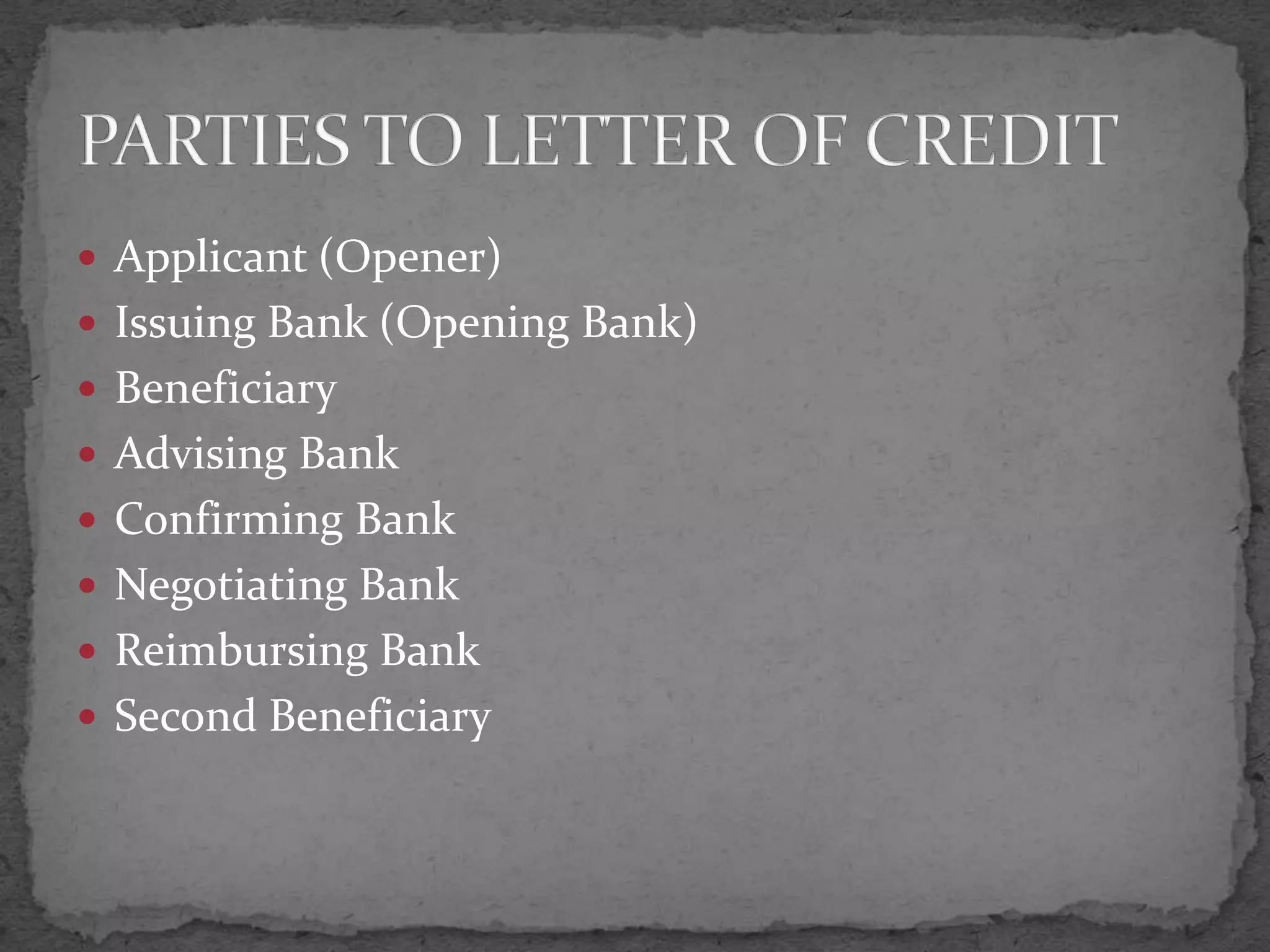

Identifies key players involved in a Letter of Credit transaction including applicant, issuing bank, and beneficiary.

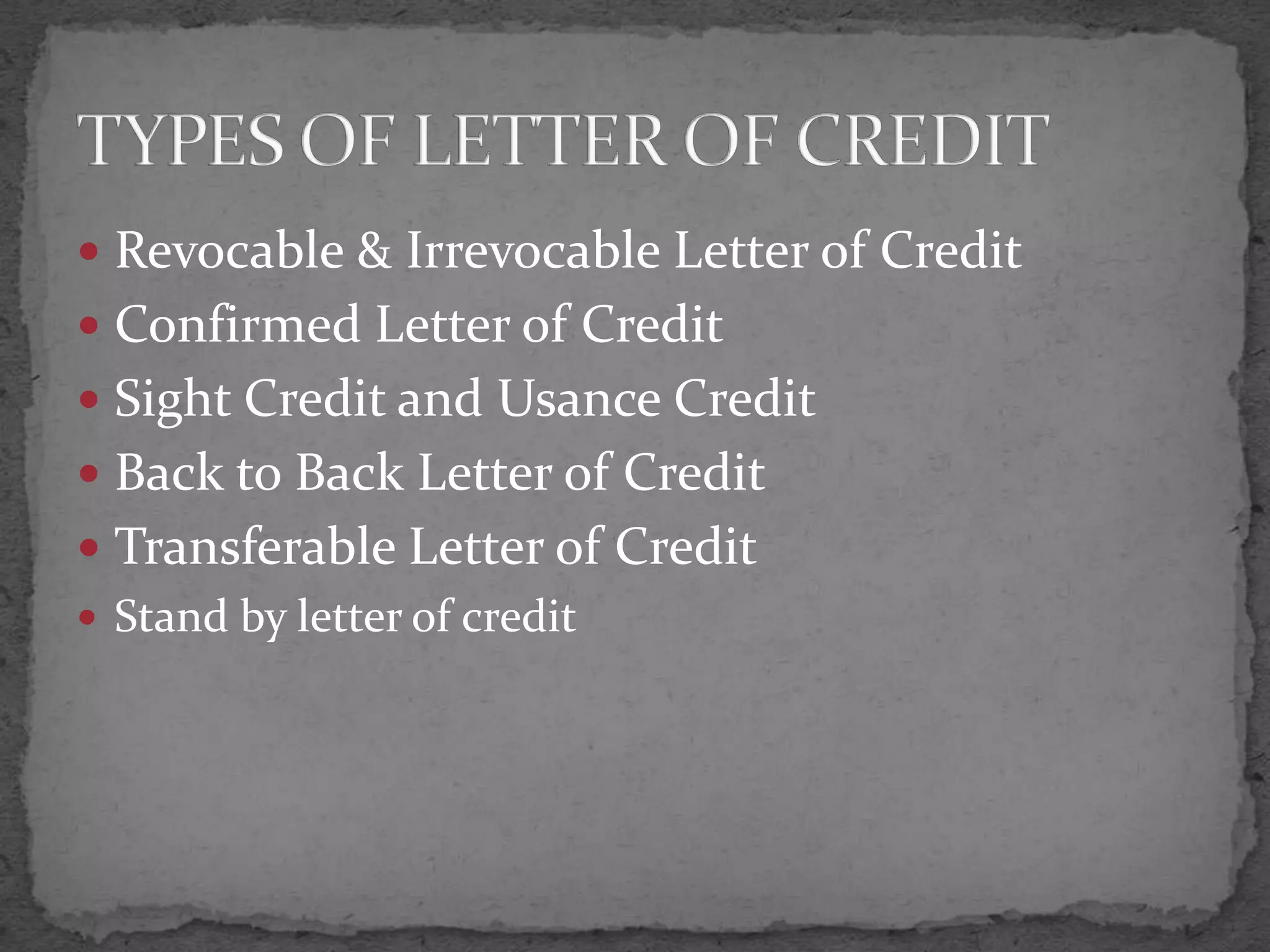

Details various types of Letters of Credit: Revocable, Irrevocable, Confirmed, and others.

Explains characteristics and drawbacks of revocable Letters of Credit in international trade.

Describes the benefits of irrevocable Letters of Credit from an exporter's perspective.

Discusses confirmed Letters of Credit and their advantages, especially for beneficiaries.

Clarifies the differences between sight credits that require immediate payment and usance credits allowing deferred payment.

Defines Back to Back Letter of Credit as a financial method to finance transactions for middlemen.

Outlines the parties involved in a Back to Back Letter of Credit, including buyer, seller and subcontractor.

Describes transferable Letters of Credit that allow benefits to be transferred from one beneficiary to another.

Explains Standby Letters of Credit as a security mechanism for bank loans similar to bank guarantees.

Outlines scenarios in which Letters of Credit are utilized in trade transactions.

Details opening charges and commitment fees involved in Letters of Credit.

Explains retirement charges for Letters of Credit and responsibilities of the applicant.

Identifies various risk factors affecting Letter of Credit transactions including country and foreign exchange risks.

Discusses purposes of Export Letters of Credit for Indian traders and exporters.

Outlines the processes involved in advising, confirming, and managing Export Letters of Credit.