Download as PDF, PPTX

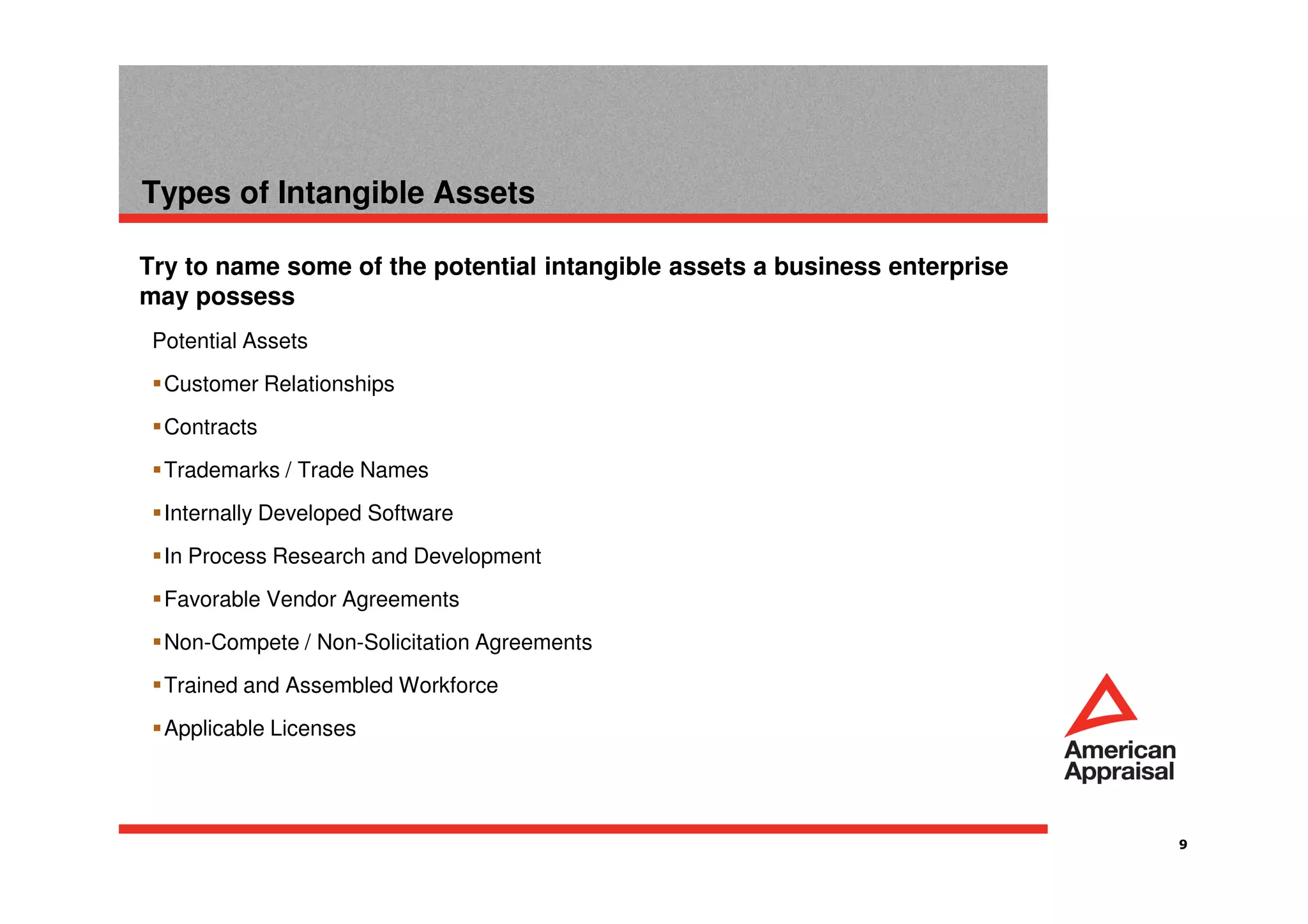

This document provides an overview and introduction to intangible assets. It discusses the key types of intangible assets including marketing-related assets like trademarks and trade names, customer-related assets like customer lists and relationships, technology-based assets like patented technology and computer software, and contract-based assets like licenses and non-compete agreements. The document defines each type of intangible asset and provides examples to illustrate the different categories.

![Brennan, Niamh and Connell, Brenda [2000] Intellectual Capital: Current Issue...](https://cdn.slidesharecdn.com/ss_thumbnails/0410brennanconnellintellectualcapitalcurrentissuesandpolicyimplications-121116102513-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)