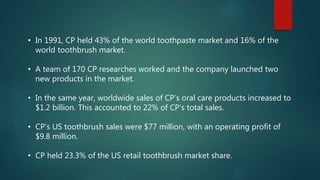

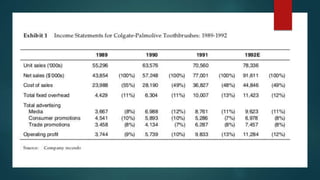

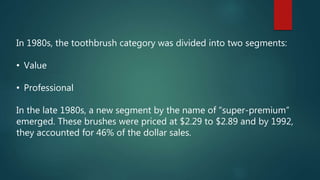

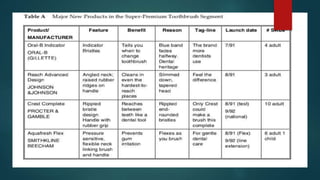

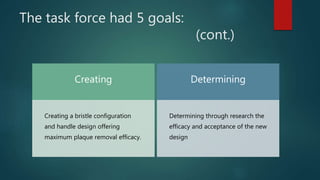

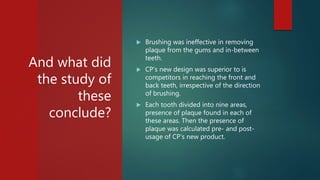

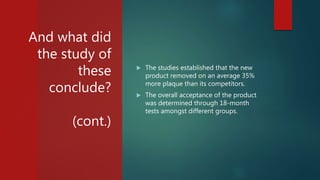

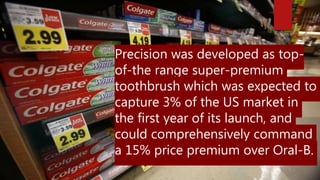

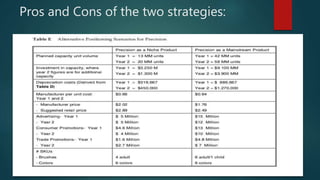

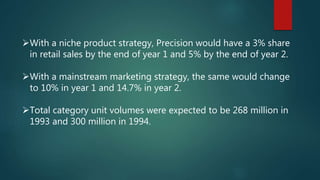

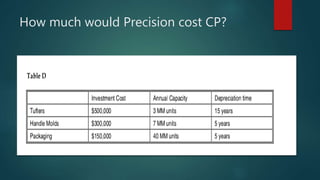

The document is a case study about Colgate Palmolive's launch of their Precision toothbrush. It provides background on the US oral care market and Colgate Palmolive's position. It then details Colgate's research and development of Precision, including clinical tests that found it removed 35% more plaque than competitors. The case discusses whether to position Precision as a niche or mainstream product. It also examines Precision's projected costs, capacity needs, and $24.1 million marketing budget for its 1992 launch. The case provides insight into Colgate Palmolive's strategic decision-making for the Precision toothbrush.