Downloaded 19 times

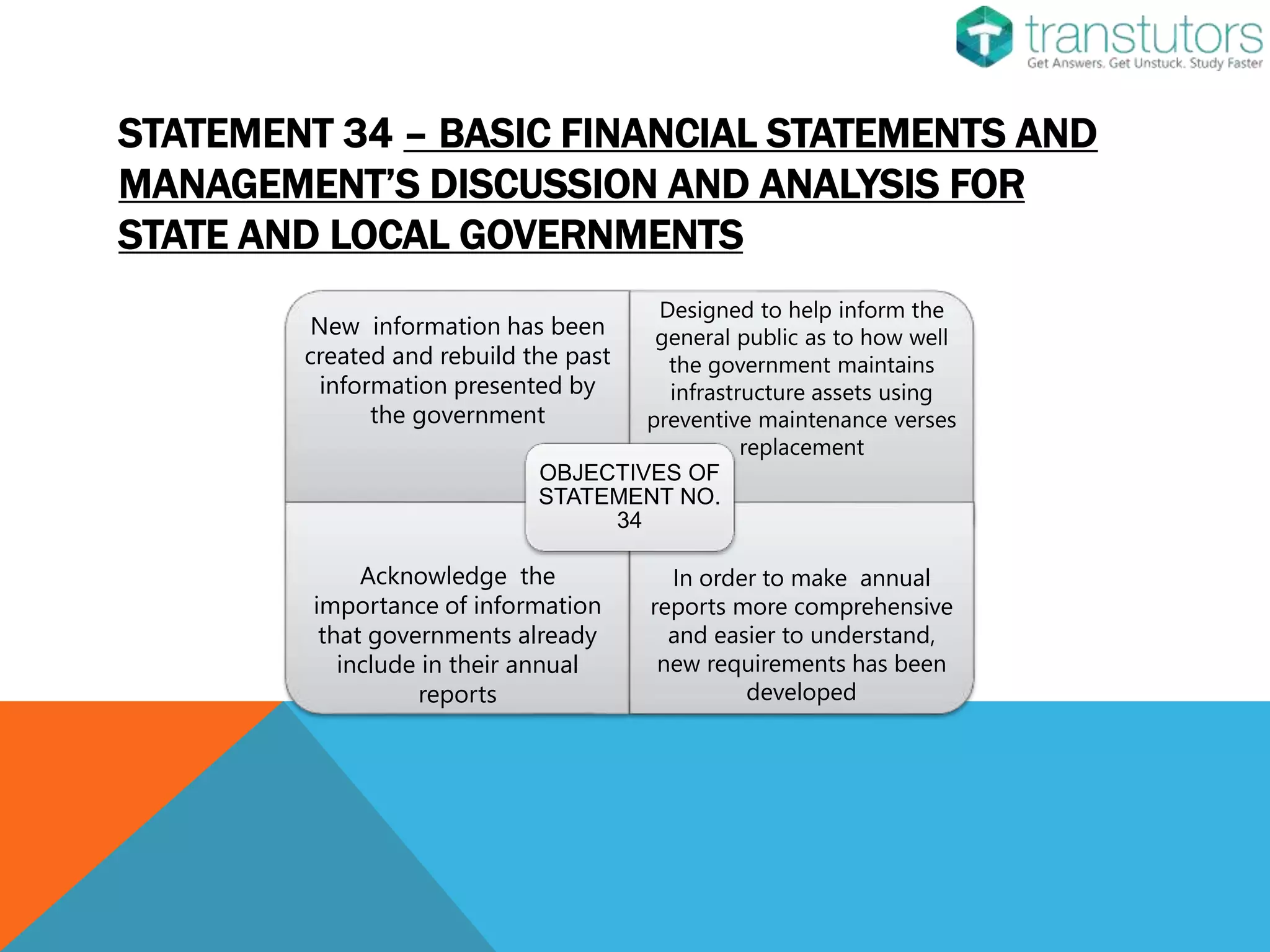

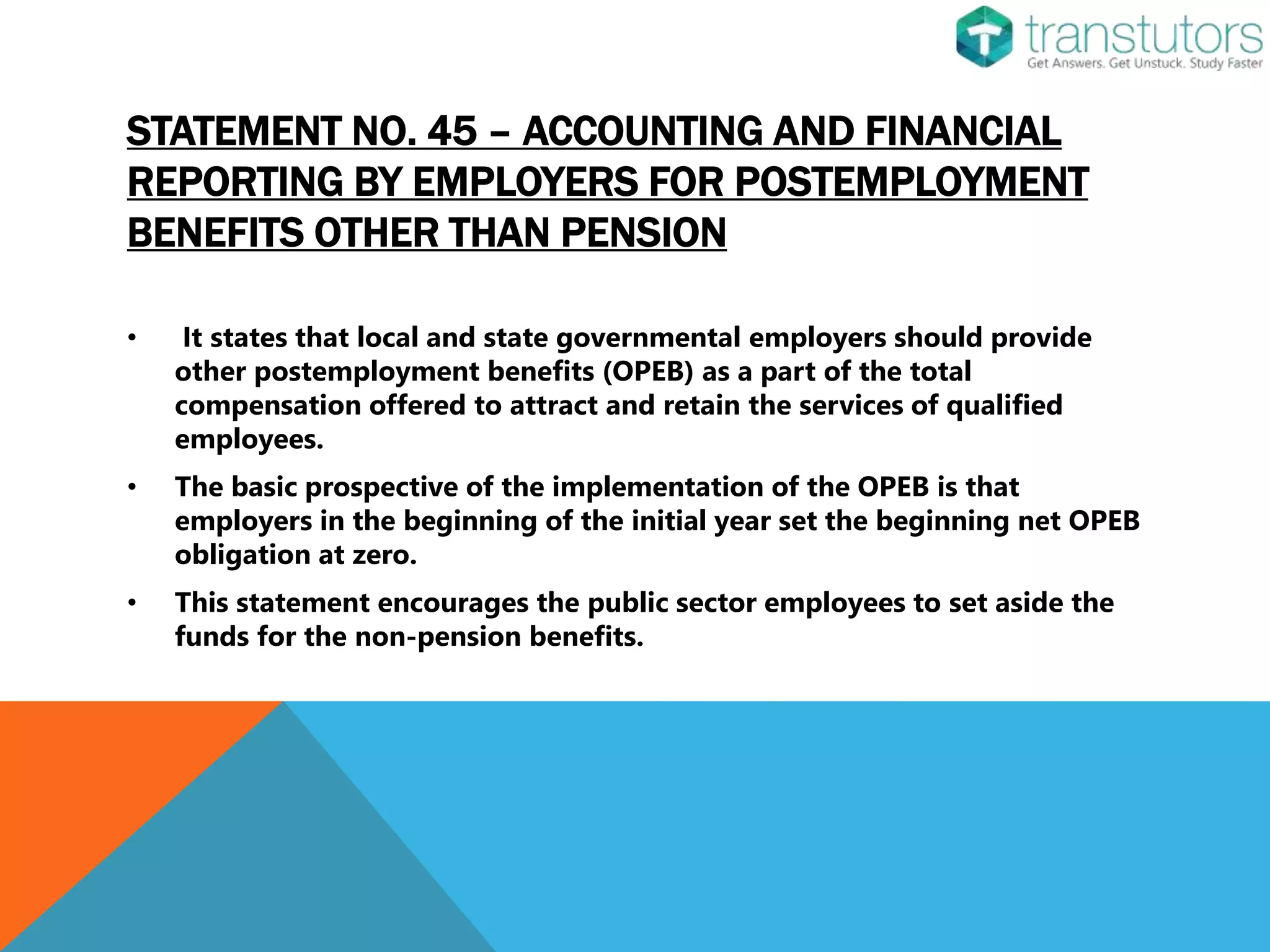

The document discusses the Governmental Accounting Standards Board (GASB) and its role in establishing accounting standards for state and local governments in the U.S. It highlights key GASB statements, such as Statement No. 34 on financial statements, Statement No. 68 on pensions, Statement No. 45 on other postemployment benefits, Statement No. 54 on fund balance reporting, and Statement No. 62 on codification guidance. Additionally, it compares GASB with the Federal Accounting Standards Advisory Board (FASAB) and outlines the objectives and significance of each GASB statement.