Downloaded 102 times

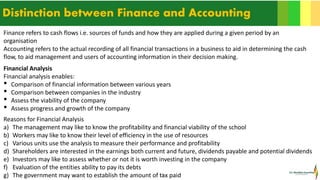

The document provides an overview of financial management practices essential for schools, highlighting the importance of managing resources effectively to enhance educational outcomes. It covers key components such as treasury management, budgeting, internal controls, and the distinction between finance and accounting. The emphasis is on ensuring value for money in all financial dealings to support sustainable and viable educational institutions.