Downloaded 48 times

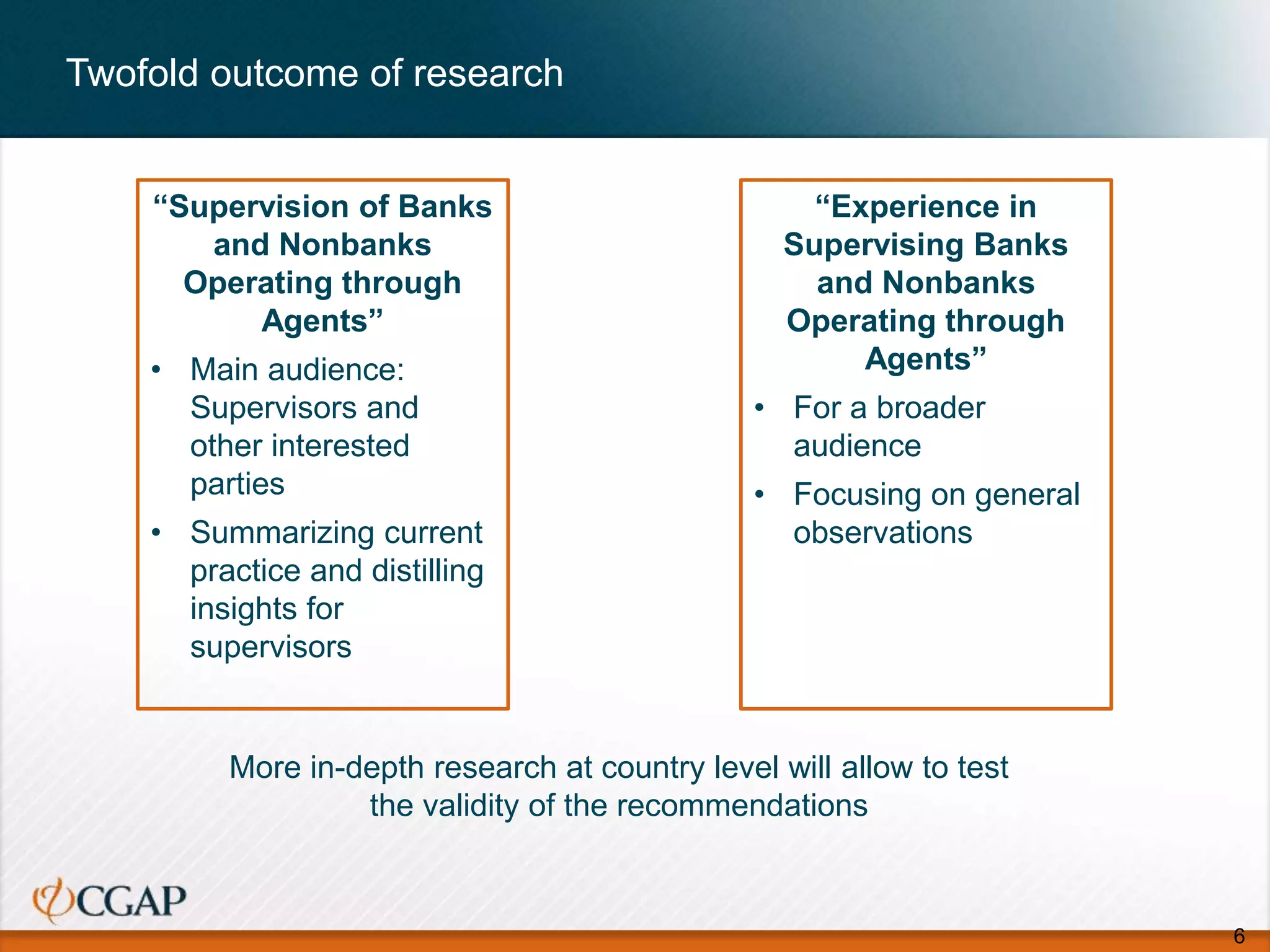

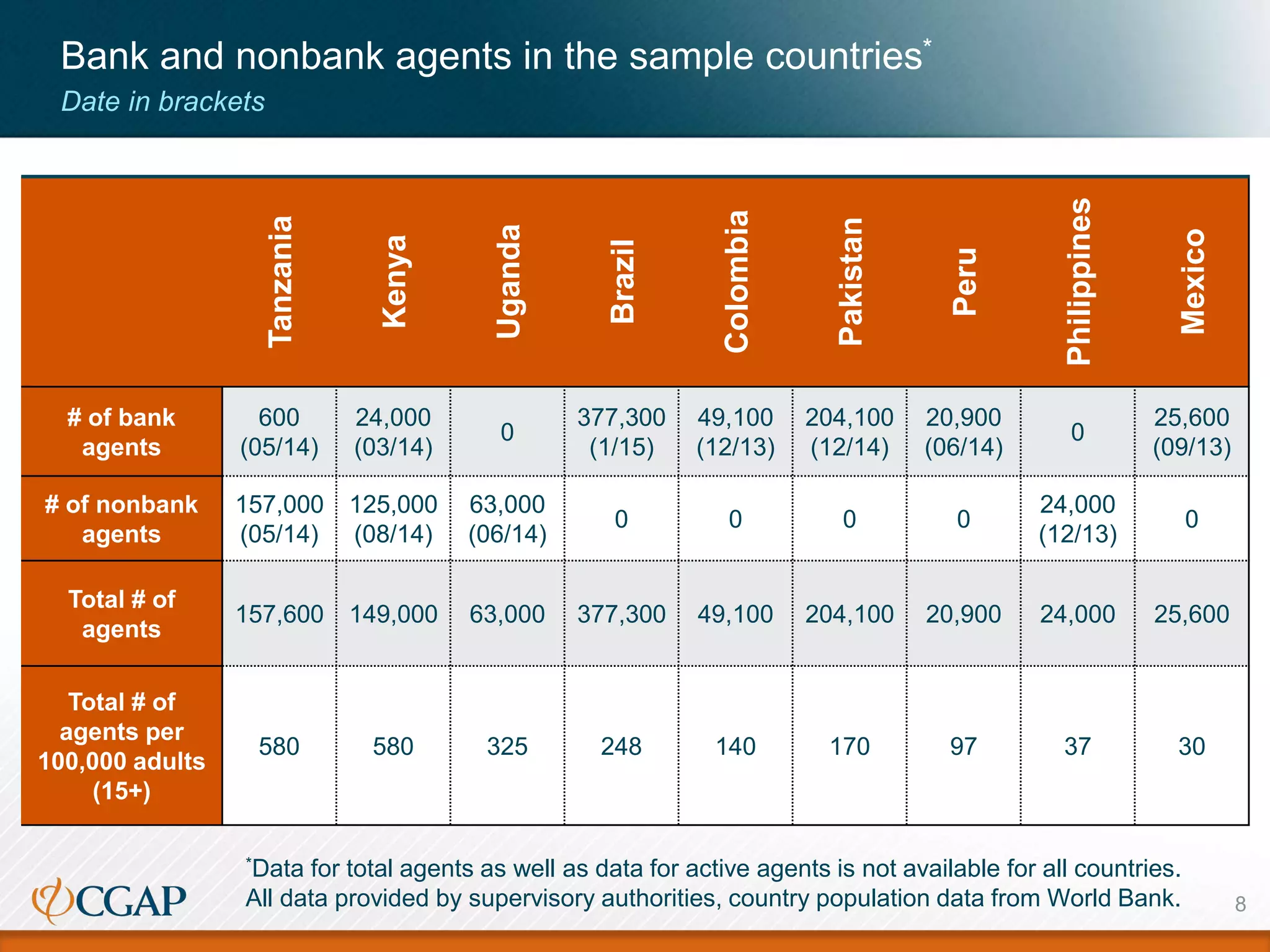

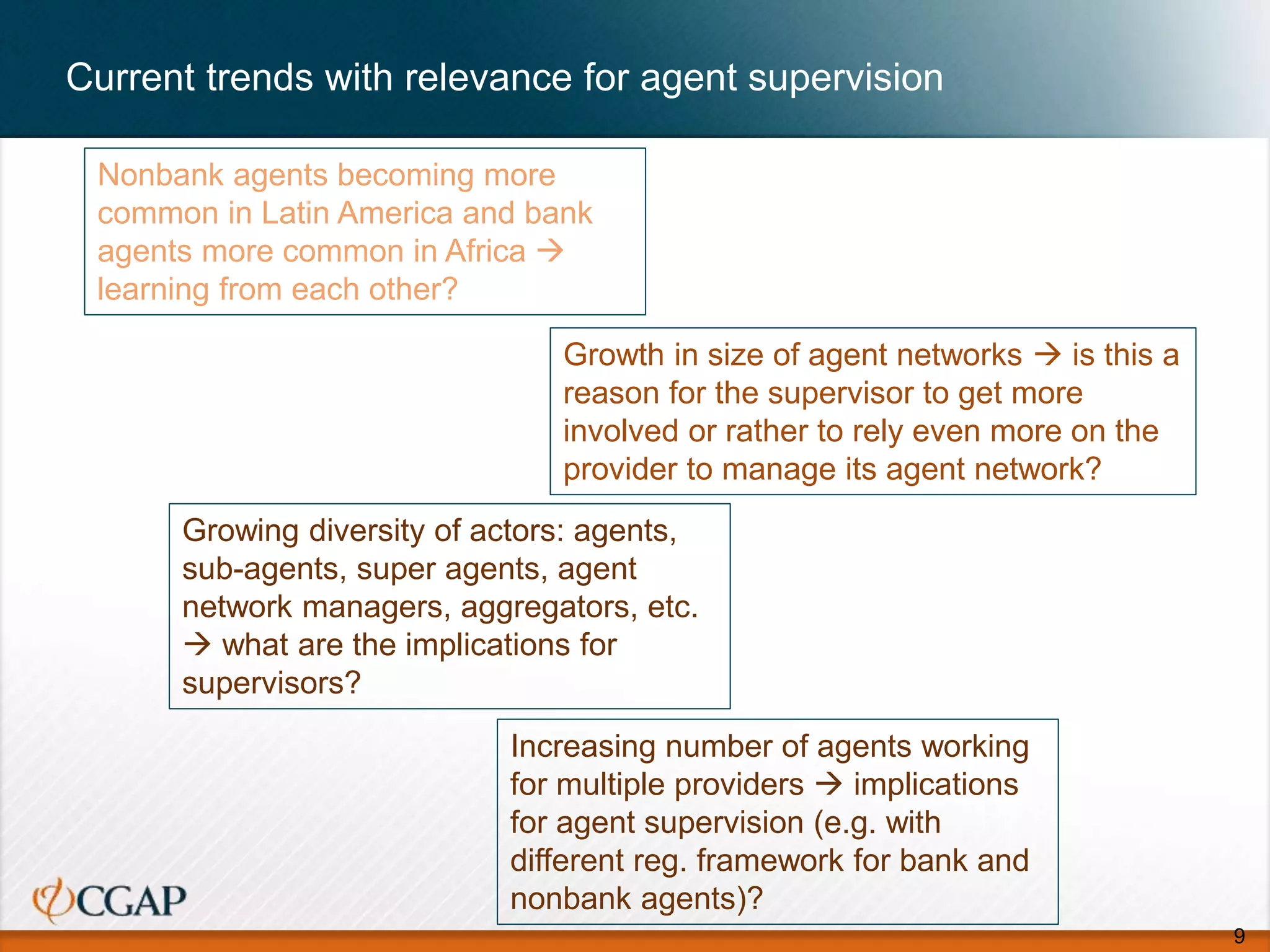

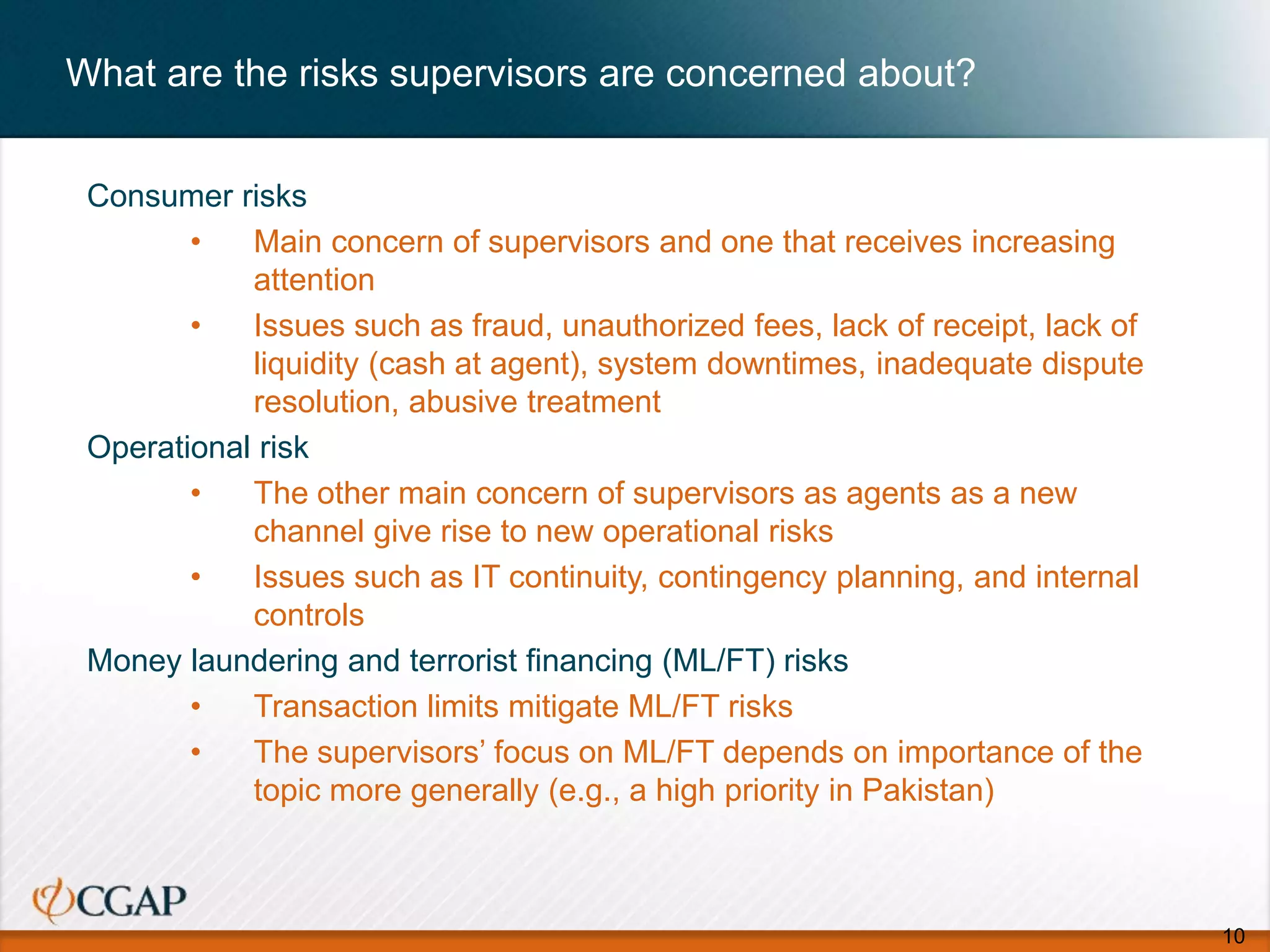

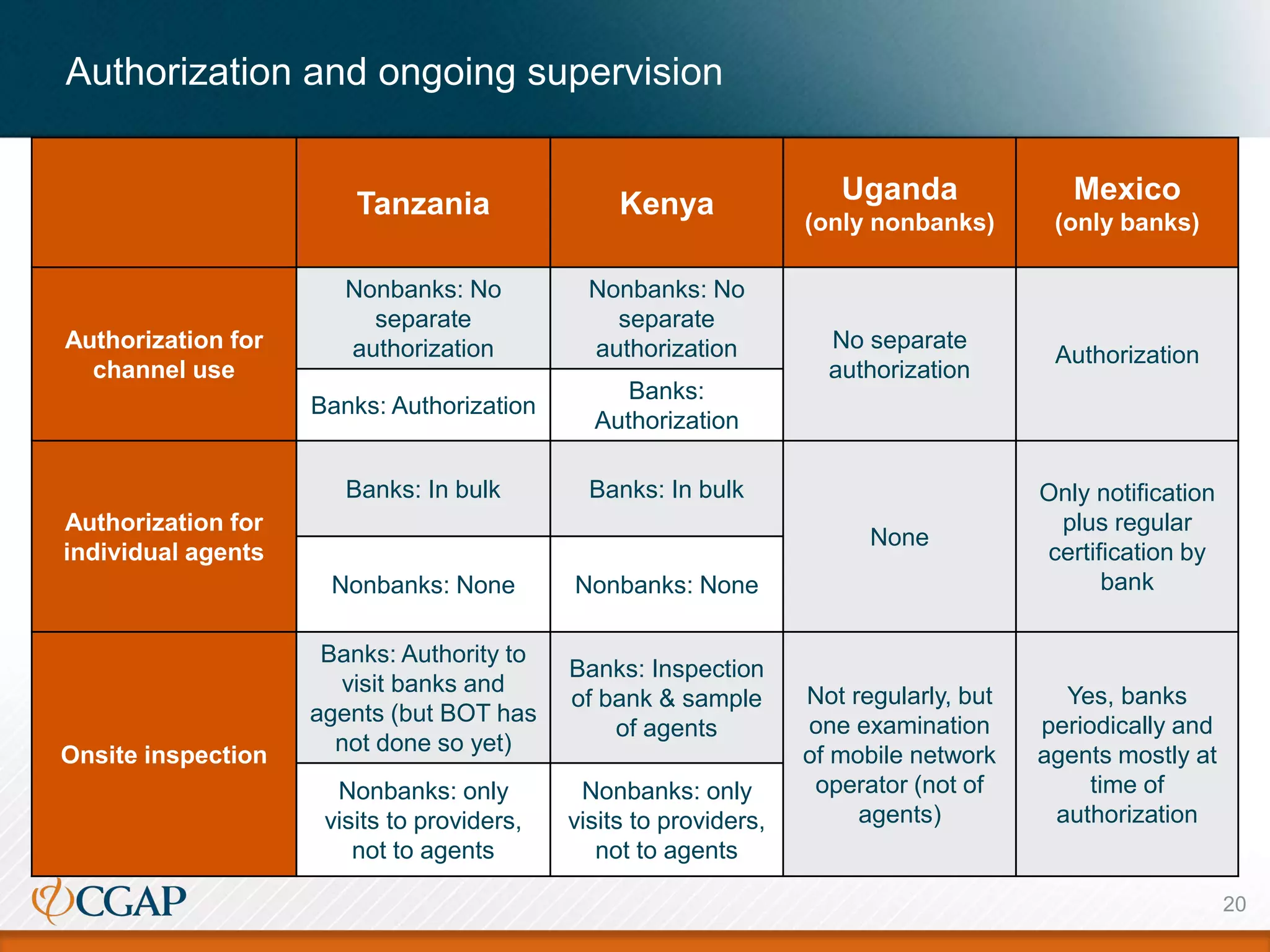

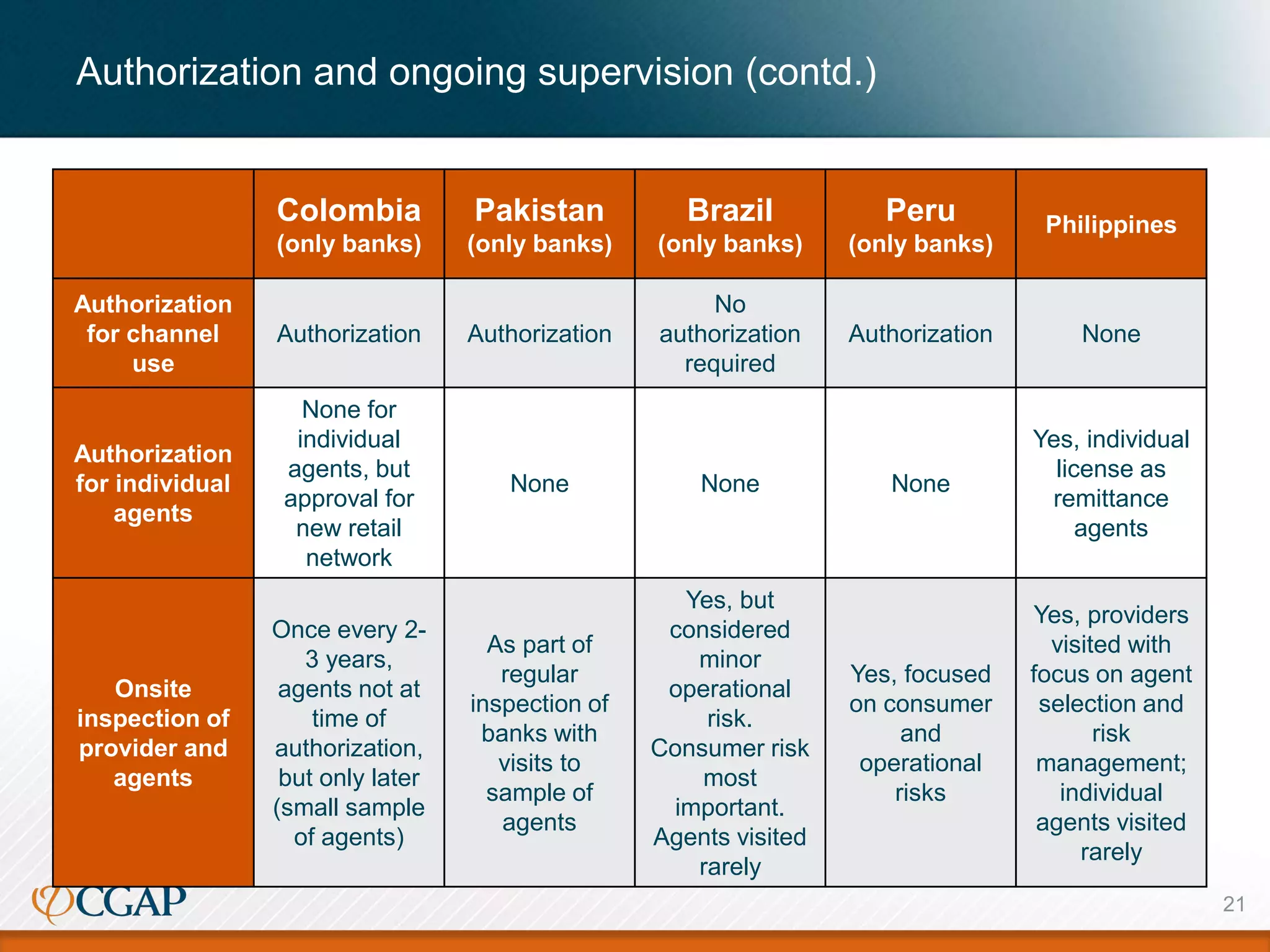

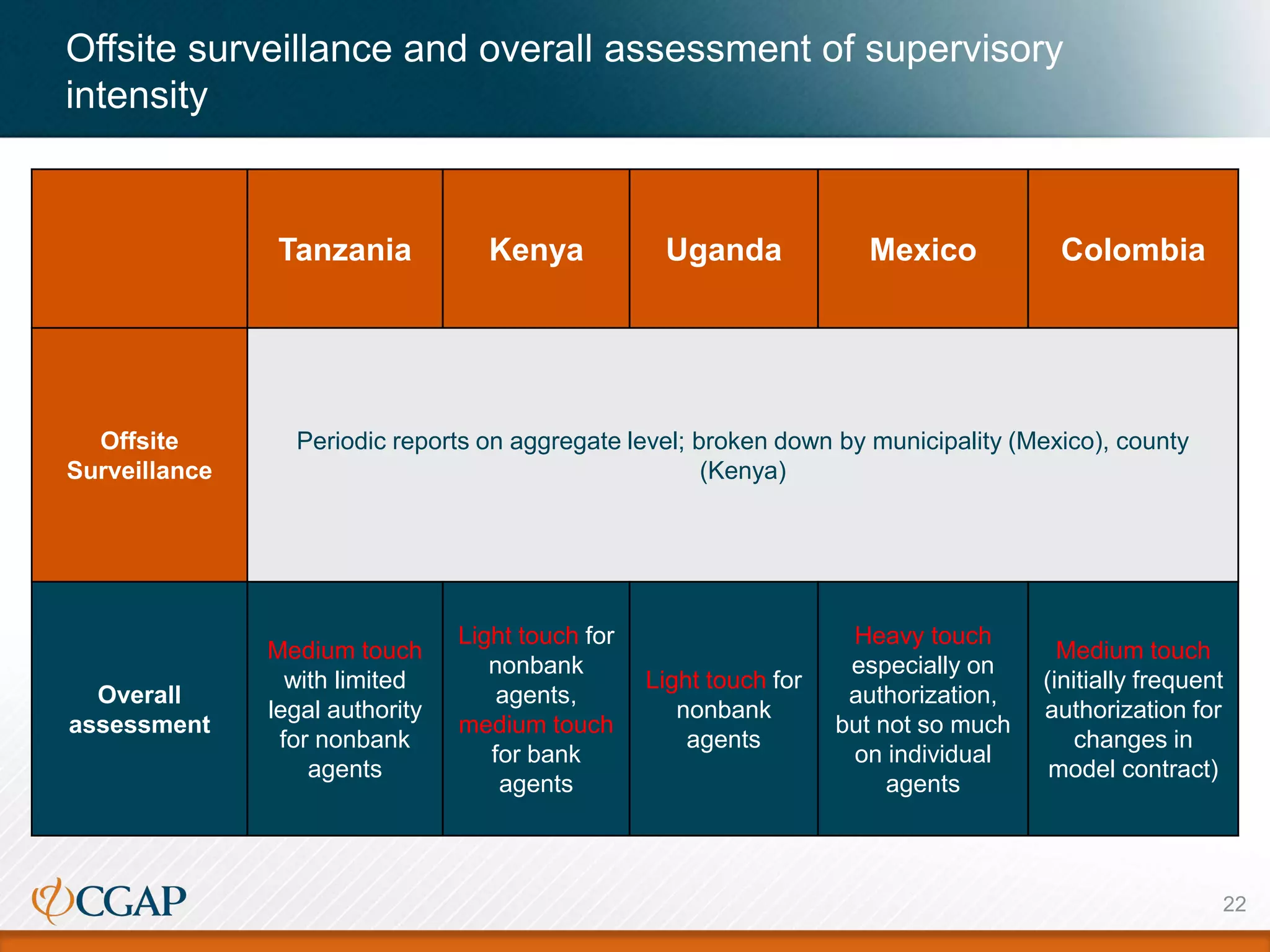

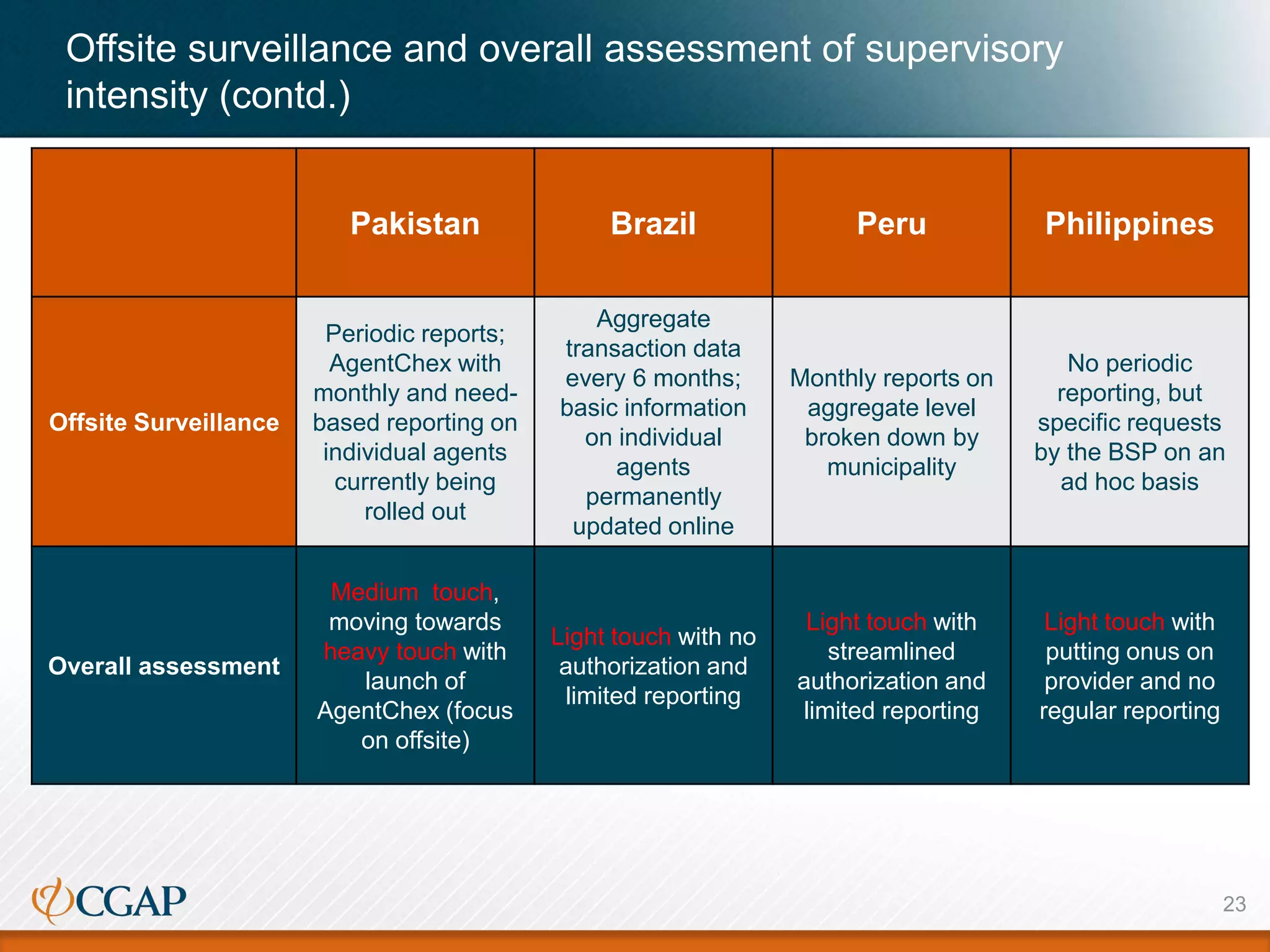

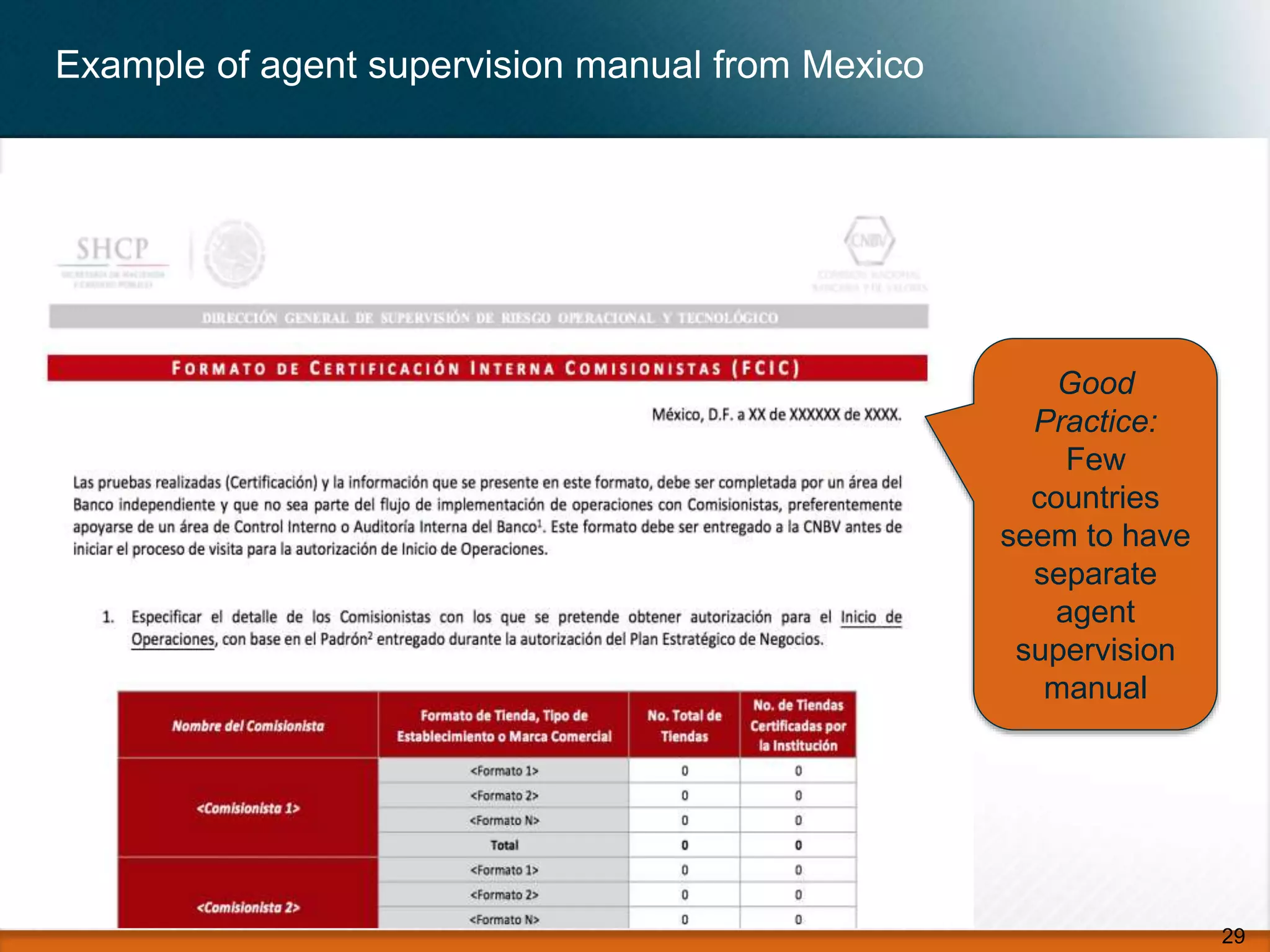

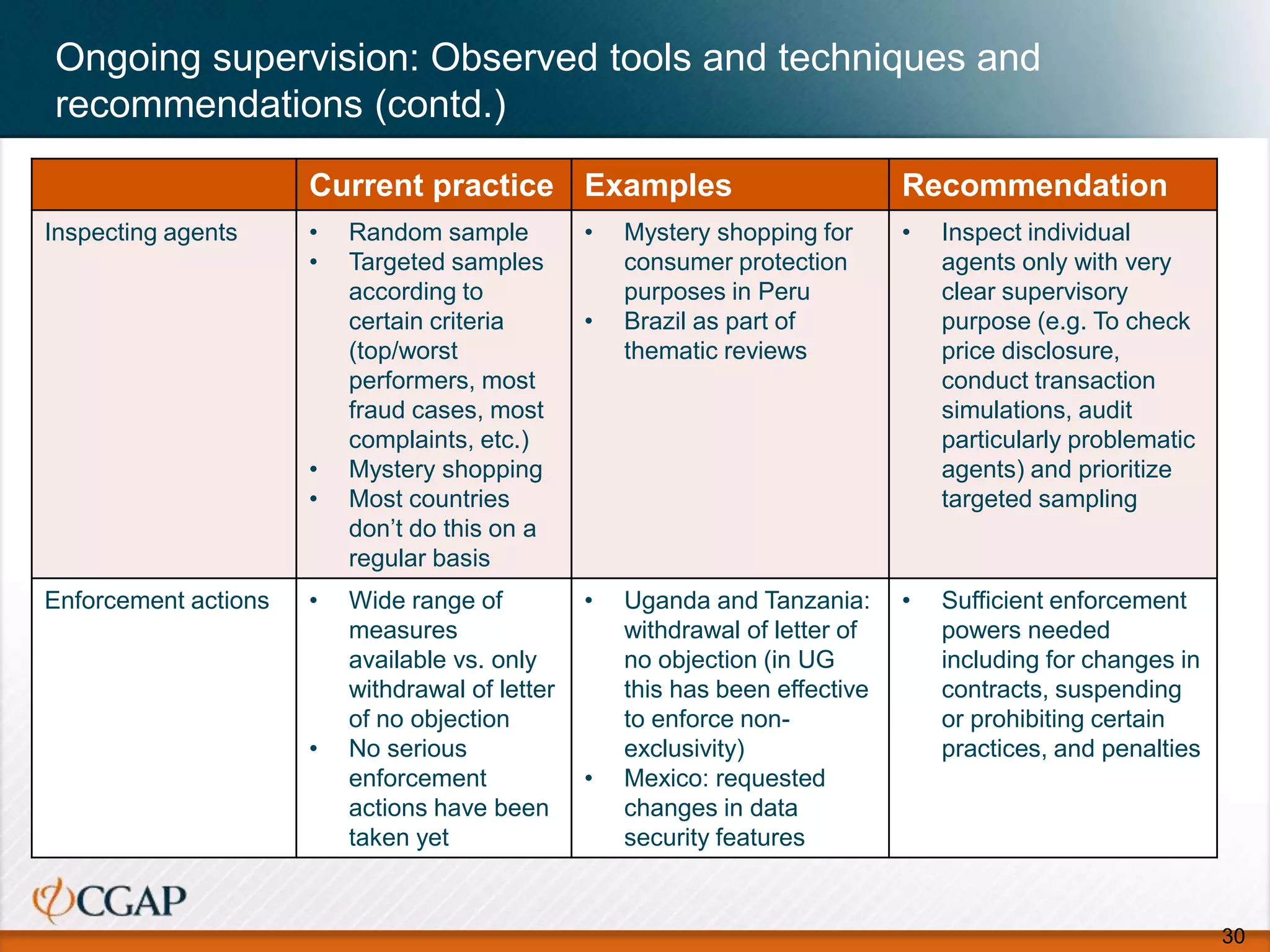

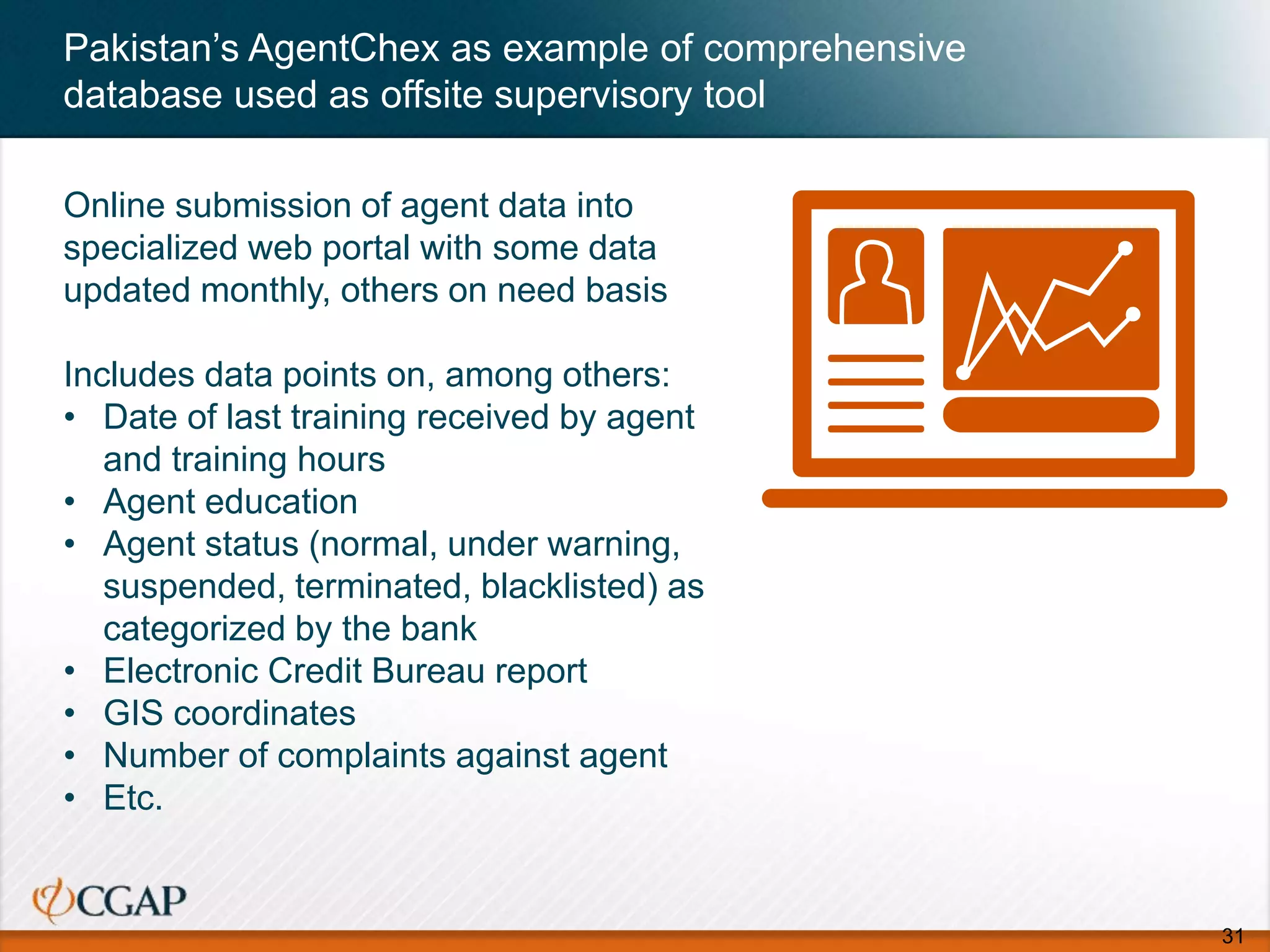

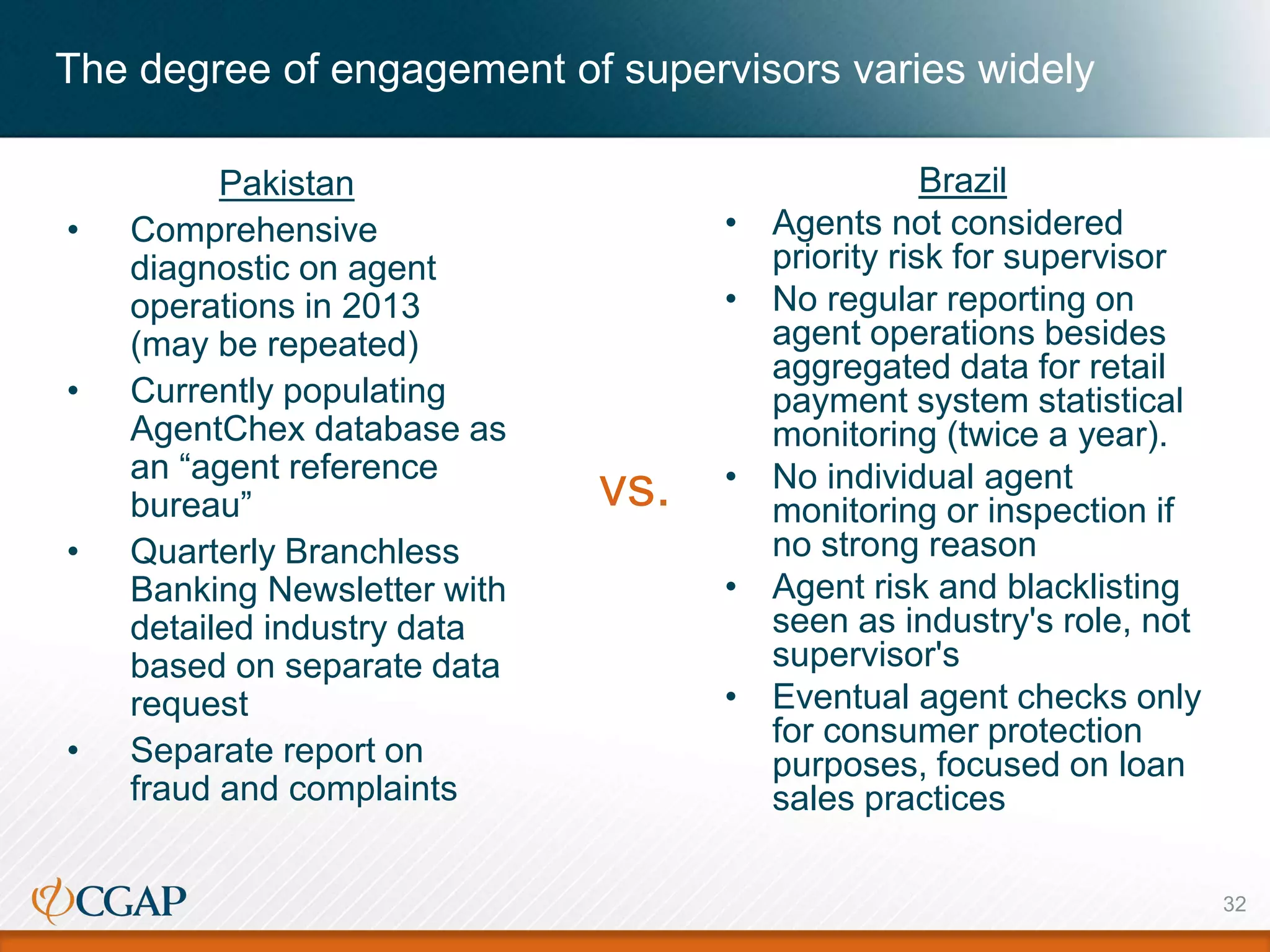

The document discusses supervisory practices for banks and nonbanks operating through agents, based on research methodology and observations from various countries. It highlights the regulatory landscape, risks associated with agent supervision, and current practices in various jurisdictions while suggesting improvements in supervisory tools and techniques. Key challenges include developing effective risk-based supervision and enhancing the qualifications of supervisory staff to address consumer and operational risks effectively.