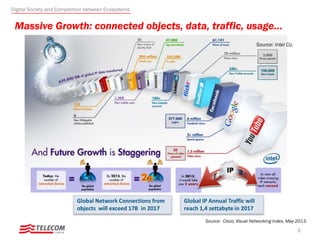

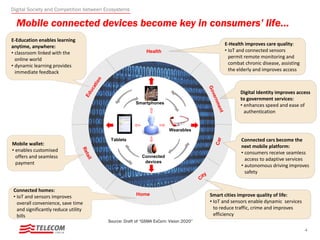

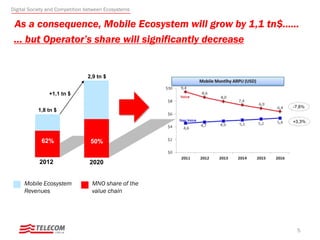

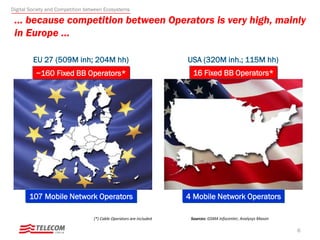

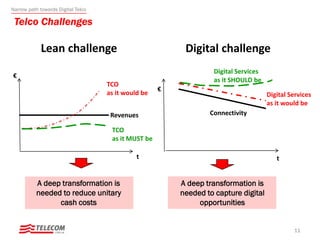

Telecom Italia presented its strategic vision for addressing future business drivers and IT implications. Massive growth in connected devices, data, traffic and usage will lead to a 1.1 trillion dollar increase in the mobile ecosystem by 2020, but operators' share will significantly decrease due to high competition and the dominance of internet companies. Telcos face challenges to reduce costs through lean operations and capture new digital opportunities. Telecom Italia's strategy is to transform networks and IT, leverage big data and cloud computing, and partner with internet companies to transition to a digital telco model.