Download as PDF, PPTX

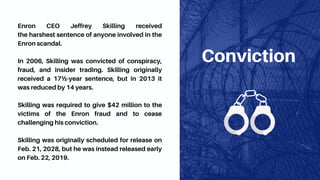

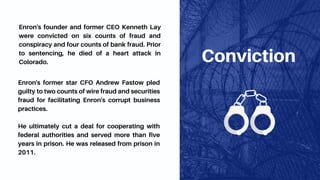

The Enron scandal involved the collapse of Enron Corporation, an American energy company, due to extensive accounting fraud and the use of special purpose entities to hide liabilities, leading to the largest bankruptcy in U.S. history in 2001. Key executives, including CEO Jeffrey Skilling and CFO Andrew Fastow, were convicted for their roles in the fraudulent activities, resulting in massive financial losses for shareholders and employees. The scandal prompted legislative reforms, including the Sarbanes-Oxley Act, aimed at increasing corporate accountability and improving financial reporting standards.

![Enron Case Study 971103 [Compatibility Mode]](https://cdn.slidesharecdn.com/ss_thumbnails/enroncasestudy-971103compatibilitymode-090531062455-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)