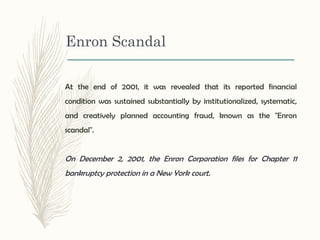

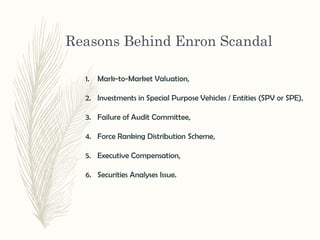

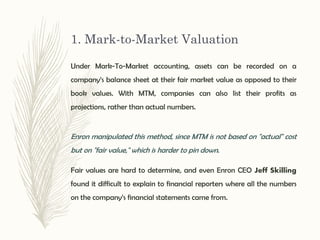

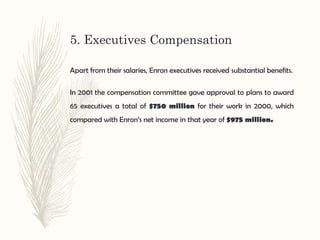

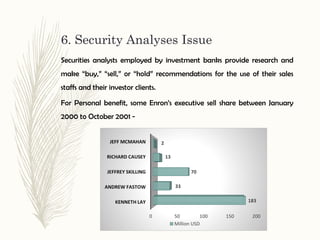

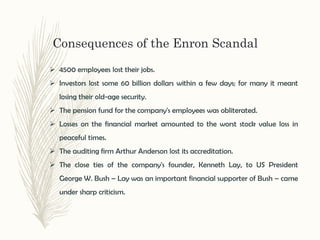

The document details the rise and fall of Enron Corporation, highlighting its initial success as an innovative energy company before its downfall due to widespread accounting fraud known as the Enron scandal. It outlines the key factors leading to the scandal, including mark-to-market accounting, ineffective auditing, and executive compensation practices. The consequences of the scandal were severe, resulting in significant job losses, investor financial damage, and the collapse of Arthur Andersen, the firm's auditing company.

![Enron Case Study 971103 [Compatibility Mode]](https://cdn.slidesharecdn.com/ss_thumbnails/enroncasestudy-971103compatibilitymode-090531062455-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)