Downloaded 350 times

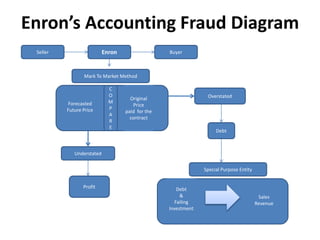

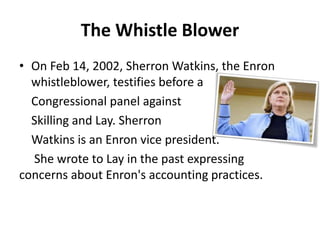

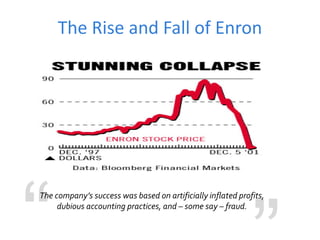

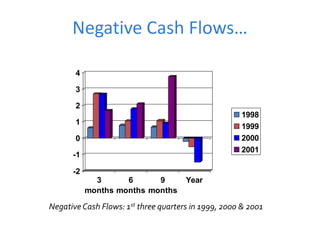

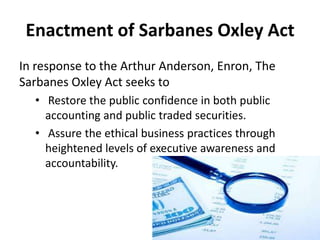

The presentation discusses the Enron scandal, focusing on the company's rise and subsequent fall due to dubious accounting practices, especially mark-to-market accounting and the use of special purpose entities. Sherron Watkins, an Enron vice president, acted as a whistleblower revealing these practices, which ultimately led to the implementation of the Sarbanes-Oxley Act to restore public confidence in corporate governance. The document emphasizes the need for stronger internal controls and corporate transparency to prevent similar scandals in the future.

![Enron Case Study 971103 [Compatibility Mode]](https://cdn.slidesharecdn.com/ss_thumbnails/enroncasestudy-971103compatibilitymode-090531062455-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)