Downloaded 366 times

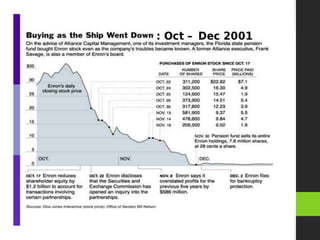

The Enron scandal, which led to the bankruptcy of the Enron Corporation in October 2001 and the dissolution of Arthur Andersen, was marked by significant accounting fraud, self-dealings, and misleading financial statements that overstated revenues and concealed liabilities. This scandal triggered extensive investigations and resulted in the passage of the Sarbanes-Oxley Act to enhance corporate governance and accountability in public companies. In the aftermath, shareholders lost billions, and former employees were awarded settlements to recover some losses.

![Enron Case Study 971103 [Compatibility Mode]](https://cdn.slidesharecdn.com/ss_thumbnails/enroncasestudy-971103compatibilitymode-090531062455-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)