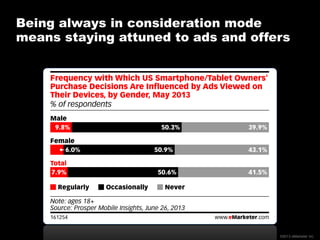

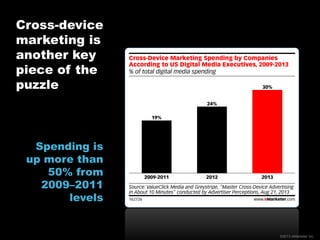

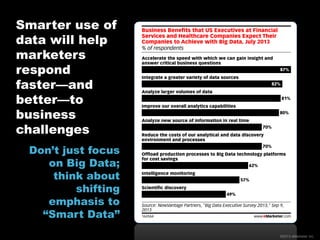

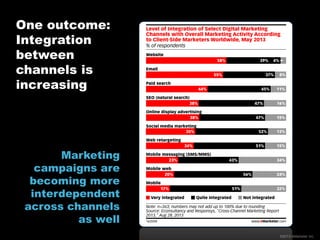

The document outlines four key digital marketing trends for 2014, emphasizing the centrality of mobile devices, the need for instant interactions, the transformation of shopping through 'always-on commerce', and the importance of social media in engaging consumers. It highlights the shift towards mobile-first strategies and the necessity for marketers to adapt quickly to consumer behaviors and preferences in a digitally connected world. The report also stressed the growing reliance on data and the integration of marketing channels to enhance consumer engagement.

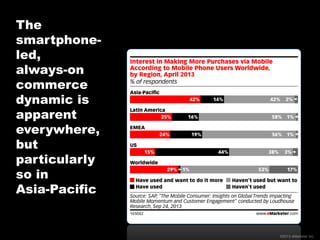

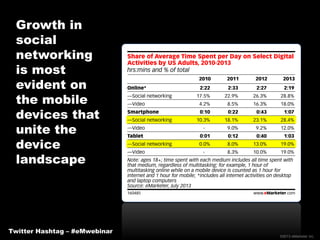

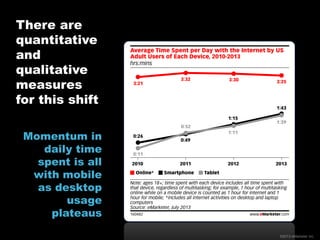

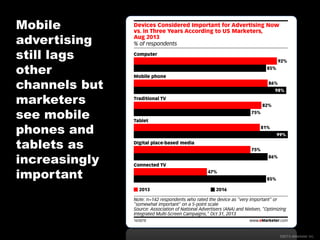

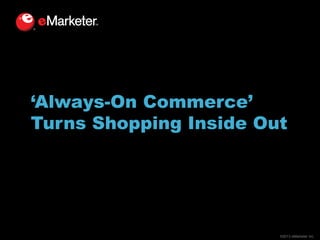

![Even if consumers aren’t consciously

shopping, they are shopping nonetheless

“Smartphone use is more or less

continuous. [It] doesn’t say anything

about whether the use has anything to

do with shopping, but it does mean that

[it has] a large part of the consumer’s

mind share during that shopping

mission. The shopping trip starts earlier

and ends later than it used to.”

—Nick Hodson, partner at Booz & Co.

©2013 eMarketer Inc.](https://image.slidesharecdn.com/emarketerwebinarkeydigitaltrends2014-131212133406-phpapp01/85/eMarketer-Webinar-Key-Digital-Trends-for-2014-22-320.jpg)