Download as PDF, PPTX

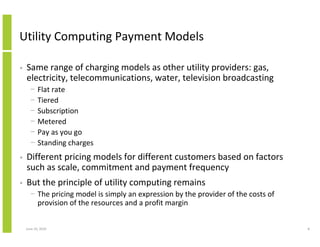

The document discusses utility computing and how organizations can transition to a utility model for information technology services. Under a utility model, users access computing resources on demand and pay based on usage, replacing traditional capital costs. While this model has similarities to older computer bureau services, it also includes storage, data transmission, and service management. For organizations to successfully adopt utility IT services, they must understand their current and future costs to implement an accurate cost recovery payment model.