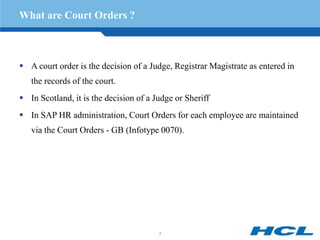

Court orders are legal decisions issued by a judge that direct an individual to take or refrain from taking a specified action. In SAP HR, court orders for each employee are maintained using infotype 0070 (Court Orders - GB). This infotype allows specification of details like standard payment amounts, protected earnings, payees, and payment periods. It also supports tracking of payment history and priorities for deduction of arrears. Student loan repayments are another type of mandatory deduction that can be configured using a subtype of infotype 0070.