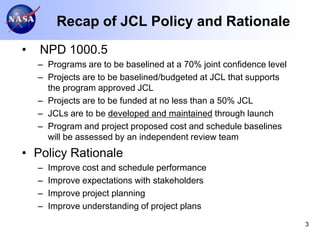

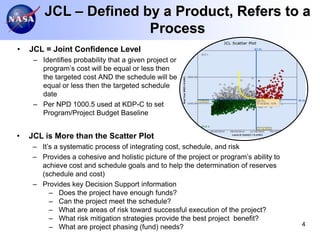

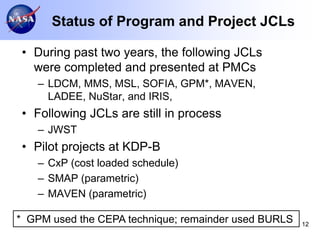

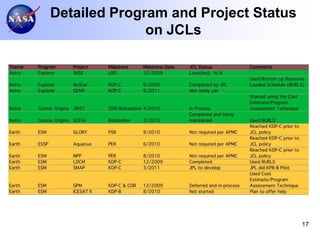

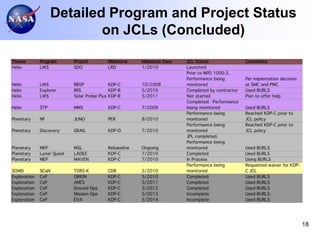

The document discusses confidence level estimating and budgeting policies. It provides a recap of the joint confidence level (JCL) policy, which requires programs to be baselined at a 70% JCL and projects to be baselined/budgeted at a JCL that supports the program's approved level. It discusses the status of JCL calculations for various programs and projects, issues learned from implementing JCLs, and actions taken to address lessons learned to improve the process.