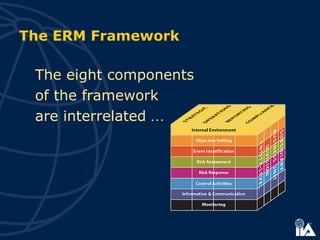

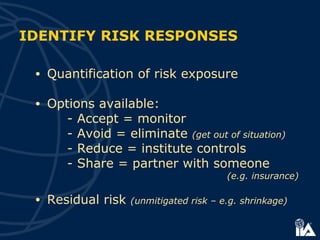

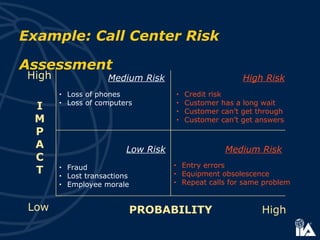

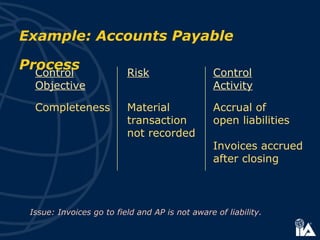

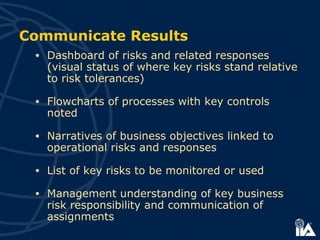

This document summarizes COSO's Enterprise Risk Management - Integrated Framework. It defines ERM as a process run by an organization's board and management to identify potential events, manage risk within the organization's risk appetite, and provide assurance around achieving objectives. The framework identifies 8 components of ERM - internal environment, objective setting, event identification, risk assessment, risk response, control activities, information & communication, and monitoring. It describes how organizations can implement ERM through risk assessments, determining risk appetite, identifying responses, and ongoing monitoring and oversight. Internal auditors can help by reviewing controls and risk processes and ensuring resources target key risk areas.