Download to read offline

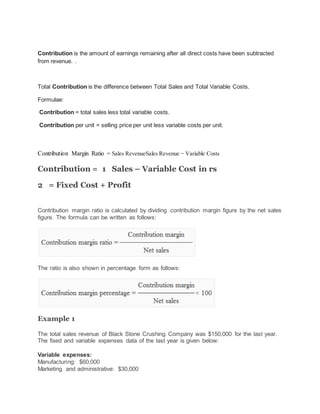

Contribution is revenue minus variable costs. It represents the amount available to cover fixed costs and generate profit. The contribution margin ratio is contribution divided by sales revenue and expresses what percentage of sales is available for fixed costs and profit. It is calculated by taking the difference between total sales and total variable costs, then dividing by total sales. Higher contribution margin ratios indicate more sales revenue available for covering fixed costs and generating profit.