Downloaded 291 times

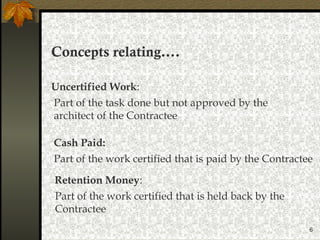

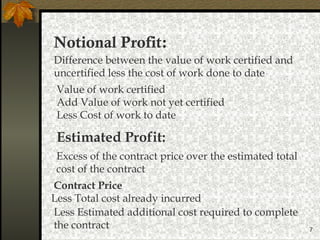

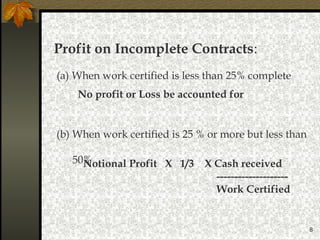

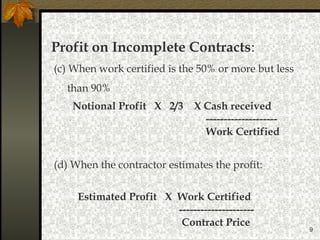

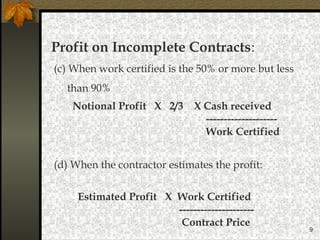

Contract costing is a method where each construction contract is treated as a separate cost unit and profit or loss is determined for each contract individually. Key features include contracts being large projects that take over a year to complete, expenses and profits being separately tracked for each contract, and payments being made based on stages of completion certified by an architect. Concepts include the contractor undertaking the work, the contractee on whose behalf the work is done, the contract price, and calculations for certified work, uncertified work, retention money, notional profit and estimated profit as a contract progresses toward completion.