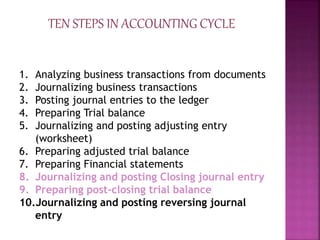

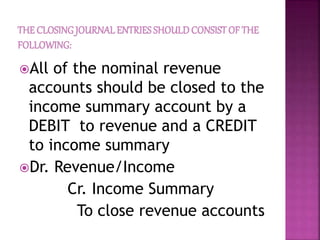

The document discusses journalizing closing entries, which involves transferring the balances of temporary accounts to the owner's capital account. Specifically, it outlines five steps:

1) Closing revenue accounts to the income summary account by debiting revenue and crediting income summary.

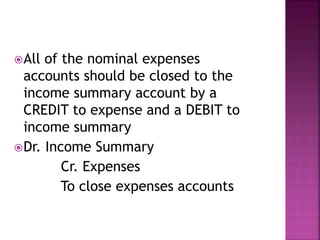

2) Closing expenses accounts by crediting expenses and debiting income summary.

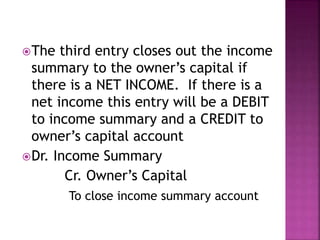

3) Closing the income summary account by debiting it and crediting owner's capital if there is a net income.

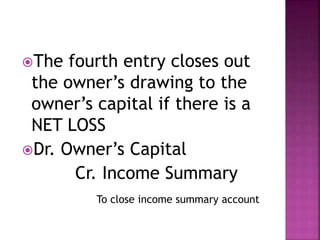

4) Closing the income summary account by debiting owner's capital and crediting income summary if there is a net loss.

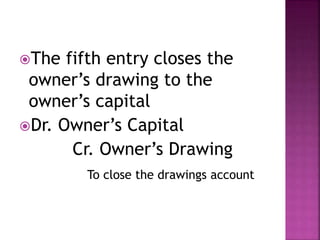

5) Closing the owner's drawing account by debiting owner's capital and crediting owner's drawing