Created by: SherylV. Paliza, CPA

LEARNING OBJECTIVES

1.Identify and explain the steps in the accounting process.

2. Identify the typical account titles used in recording transactions

3. Explain the Double Entry System and use it in recording business

transactions

4.Prepare adjusting entries and understand the rationale for their

preparation.

3.Prepare closing entries and understand the rationale for their

preparation.

5.Explain the advantages of preparing reversing entries and identify

adjusting entries that may be reversed.

3.

Created by: SherylV. Paliza, CPA

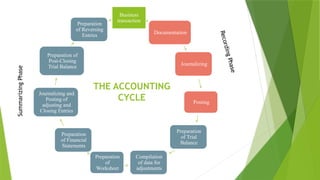

ACCOUNTING PROCESS

procedures or series of steps undertaken to come up with

the information reported in the financial statements.

also referred to as the Accounting Cycle.

Divided into two phases:

RECORDING PHASE

SUMMARIZING PHASE

4.

Created by: SherylV. Paliza, CPA

RECORDING PHASE

collecting information about economic transactions and the recording of

these transactions in the appropriate accounting records

Transaction - economic event that changes an asset, a liability, or

an equity account balance

Accounting records - include business documents, journals, and

ledgers.

5.

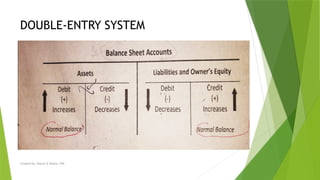

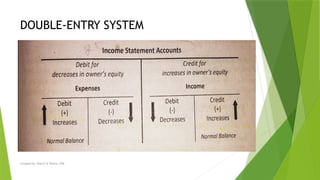

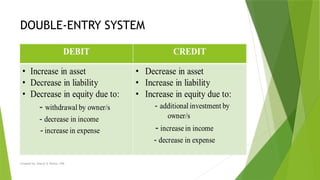

DOUBLE-ENTRY SYSTEM

meansthat the dual effects of a business transaction is recorded.

A debit side entry must have a corresponding credit side entry.

For every transaction, there must be one or more accounts debited and

one or more accounts credited.

Created by: Sheryl V. Paliza, CPA

NORMAL BALANCE OF AN ACCOUNT

-refers to the side of the account (debit or credit) where increases are

recorded.

Created by: SherylV. Paliza, CPA

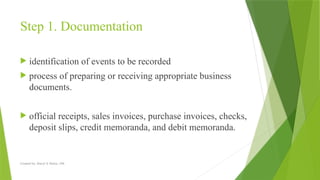

Step 1. Documentation

identification of events to be recorded

process of preparing or receiving appropriate business

documents.

official receipts, sales invoices, purchase invoices, checks,

deposit slips, credit memoranda, and debit memoranda.

11.

Created by: SherylV. Paliza, CPA

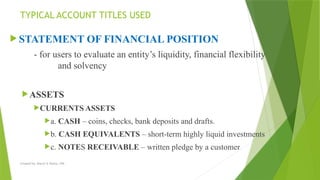

TYPICAL ACCOUNT TITLES USED

STATEMENT OF FINANCIAL POSITION

- for users to evaluate an entity’s liquidity, financial flexibility

and solvency

ASSETS

CURRENTS ASSETS

a. CASH – coins, checks, bank deposits and drafts.

b. CASH EQUIVALENTS – short-term highly liquid investments

c. NOTES RECEIVABLE – written pledge by a customer

12.

Created by: SherylV. Paliza, CPA

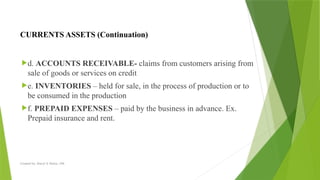

d. ACCOUNTS RECEIVABLE- claims from customers arising from

sale of goods or services on credit

e. INVENTORIES – held for sale, in the process of production or to

be consumed in the production

f. PREPAID EXPENSES – paid by the business in advance. Ex.

Prepaid insurance and rent.

CURRENTS ASSETS (Continuation)

13.

Created by: SherylV. Paliza, CPA

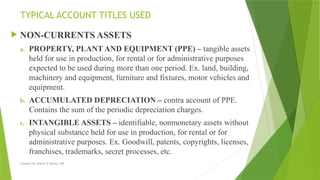

NON-CURRENTS ASSETS

a. PROPERTY, PLANT AND EQUIPMENT (PPE) – tangible assets

held for use in production, for rental or for administrative purposes

expected to be used during more than one period. Ex. land, building,

machinery and equipment, furniture and fixtures, motor vehicles and

equipment.

b. ACCUMULATED DEPRECIATION – contra account of PPE.

Contains the sum of the periodic depreciation charges.

c. INTANGIBLE ASSETS – identifiable, nonmonetary assets without

physical substance held for use in production, for rental or for

administrative purposes. Ex. Goodwill, patents, copyrights, licenses,

franchises, trademarks, secret processes, etc.

TYPICAL ACCOUNT TITLES USED

14.

Created by: SherylV. Paliza, CPA

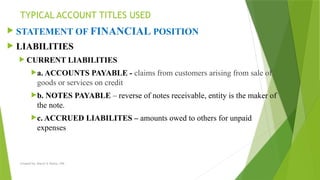

STATEMENT OF FINANCIAL POSITION

LIABILITIES

CURRENT LIABILITIES

a. ACCOUNTS PAYABLE - claims from customers arising from sale of

goods or services on credit

b. NOTES PAYABLE – reverse of notes receivable, entity is the maker of

the note.

c. ACCRUED LIABILITES – amounts owed to others for unpaid

expenses

TYPICAL ACCOUNT TITLES USED

15.

Created by: SherylV. Paliza, CPA

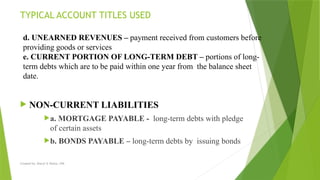

NON-CURRENT LIABILITIES

a. MORTGAGE PAYABLE - long-term debts with pledge

of certain assets

b. BONDS PAYABLE – long-term debts by issuing bonds

TYPICAL ACCOUNT TITLES USED

d. UNEARNED REVENUES – payment received from customers before

providing goods or services

e. CURRENT PORTION OF LONG-TERM DEBT – portions of long-

term debts which are to be paid within one year from the balance sheet

date.

16.

Created by: SherylV. Paliza, CPA

STATEMENT OF FINANCIAL POSITION

OWNER’S EQUITY

a. CAPITAL – original and additional investments of the owner/s

of the entity

b.WITHDRAWALS – when the owner/s withdraw cash or other

assets from the entity

c. INCOME SUMMARY – temporary account used at the end of

the accounting period to close income and expenses. This account

shows the profit or loss for the period

TYPICAL ACCOUNT TITLES USED

17.

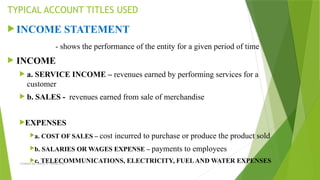

Created by: SherylV. Paliza, CPA

INCOME STATEMENT

- shows the performance of the entity for a given period of time

INCOME

a. SERVICE INCOME – revenues earned by performing services for a

customer

b. SALES - revenues earned from sale of merchandise

EXPENSES

a. COST OF SALES – cost incurred to purchase or produce the product sold

b. SALARIES OR WAGES EXPENSE – payments to employees

c. TELECOMMUNICATIONS, ELECTRICITY, FUELAND WATER EXPENSES

TYPICAL ACCOUNT TITLES USED

18.

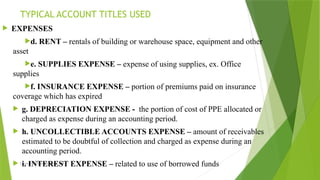

Created by: SherylV. Paliza, CPA

EXPENSES

d. RENT – rentals of building or warehouse space, equipment and other

asset

e. SUPPLIES EXPENSE – expense of using supplies, ex. Office

supplies

f. INSURANCE EXPENSE – portion of premiums paid on insurance

coverage which has expired

g. DEPRECIATION EXPENSE - the portion of cost of PPE allocated or

charged as expense during an accounting period.

h. UNCOLLECTIBLE ACCOUNTS EXPENSE – amount of receivables

estimated to be doubtful of collection and charged as expense during an

accounting period.

i. INTEREST EXPENSE – related to use of borrowed funds

TYPICAL ACCOUNT TITLES USED

19.

Created by: SherylV. Paliza, CPA

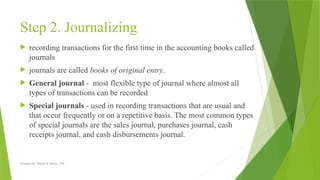

Step 2. Journalizing

recording transactions for the first time in the accounting books called

journals

journals are called books of original entry.

General journal - most flexible type of journal where almost all

types of transactions can be recorded

Special journals - used in recording transactions that are usual and

that occur frequently or on a repetitive basis. The most common types

of special journals are the sales journal, purchases journal, cash

receipts journal, and cash disbursements journal.

20.

Created by: SherylV. Paliza, CPA

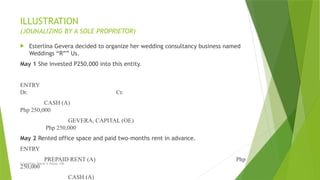

ILLUSTRATION

(JOUNALIZING BY A SOLE PROPRIETOR)

Esterlina Gevera decided to organize her wedding consultancy business named

Weddings “R”” Us.

May 1 She invested P250,000 into this entity.

ENTRY

Dr. Cr.

CASH (A)

Php 250,000

GEVERA, CAPITAL (OE)

Php 250,000

May 2 Rented office space and paid two-months rent in advance.

ENTRY

PREPAID RENT (A) Php

250,000

CASH (A)

21.

Created by: SherylV. Paliza, CPA

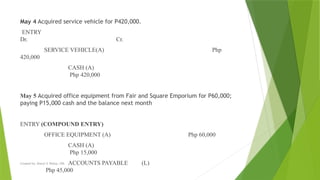

May 4 Acquired service vehicle for P420,000.

ENTRY

Dr. Cr.

SERVICE VEHICLE(A) Php

420,000

CASH (A)

Php 420,000

May 5 Acquired office equipment from Fair and Square Emporium for P60,000;

paying P15,000 cash and the balance next month

ENTRY (COMPOUND ENTRY)

OFFICE EQUIPMENT (A) Php 60,000

CASH (A)

Php 15,000

ACCOUNTS PAYABLE (L)

Php 45,000

22.

Created by: SherylV. Paliza, CPA

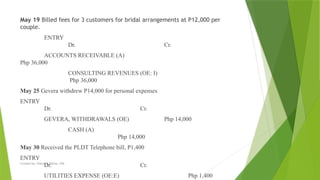

May 19 Billed fees for 3 customers for bridal arrangements at P12,000 per

couple.

ENTRY

Dr. Cr.

ACCOUNTS RECEIVABLE (A)

Php 36,000

CONSULTING REVENUES (OE: I)

Php 36,000

May 25 Gevera withdrew P14,000 for personal expenses

ENTRY

Dr. Cr.

GEVERA, WITHDRAWALS (OE) Php 14,000

CASH (A)

Php 14,000

May 30 Received the PLDT Telephone bill, P1,400

ENTRY

Dr. Cr.

UTILITIES EXPENSE (OE:E) Php 1,400

23.

Created by: SherylV. Paliza, CPA

Step 3. Posting

process of transferring the recorded transactions in the journal to the accounts in the

ledger

to classify the effects of transactions on specific asset, liability, equity, income and

expense accounts.

A ledger is a group of related accounts and is called the book of final entry.

1. General ledger - principal ledger which contains all the accounts that

are reported in the financial statements

Contra accounts- established to record deductions from related

accounts with positive balances such as Accumulated Depreciation (deducted from

Property, Plant and Equipment)

Adjunct accounts are accounts set up to record additions to

related accounts such as Freight-In (added to Purchases)

2. Subsidiary ledgers - contain details of some general ledger account

balances.

24.

Created by: SherylV. Paliza, CPA

SUMMARIZING PHASE

Includes the steps necessary for the preparation summary reports.

25.

Created by: SherylV. Paliza, CPA

Step 4. Preparing a trial balance

Trial balance – summary of balances of the accounts in the

general ledger

- prepared to prove the equality of debits and credit but

it does not indicate the accuracy of work done

- preparation of a trial balance is normally done in the work

sheet

26.

Created by: SherylV. Paliza, CPA

Step 5. Compiling adjusting data

process of gathering and putting together various data necessary to

update the balances of certain accounts in the books of the company.

Adjustments are necessary so that income and expenses will be

reported in the period they are earned and incurred respectively;

hence, profit will not be misstated.

27.

Created by: SherylV. Paliza, CPA

Common types of adjusting data

A. Accrued expense

B. Accrued income

C. Prepaid expense

D. Unearned /income

E. Depreciation of property, plant and equipment and

other cost allocation

F. Uncollectible accounts

G. Inventory

Step 5. Compiling adjusting data (conti.)

28.

Created by: SherylV. Paliza, CPA

A. ACCRUED EXPENSE

Expense incurred but not yet paid as of the balance sheet date

Matched against income or earnings for the current period

Examples are interest accrued on notes payable and accrued salaries

of employees.

Adjustment for accrued expense is recorded as follows:

Expense XXX

Payable XXX

29.

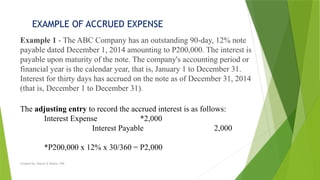

Example 1 -The ABC Company has an outstanding 90-day, 12% note

payable dated December 1, 2014 amounting to P200,000. The interest is

payable upon maturity of the note. The company's accounting period or

financial year is the calendar year, that is, January 1 to December 31.

Interest for thirty days has accrued on the note as of December 31, 2014

(that is, December 1 to December 31).

Created by: Sheryl V. Paliza, CPA

EXAMPLE OF ACCRUED EXPENSE

The adjusting entry to record the accrued interest is as follows:

Interest Expense *2,000

Interest Payable 2,000

*P200,000 x 12% x 30/360 = P2,000

30.

Created by: SherylV. Paliza, CPA

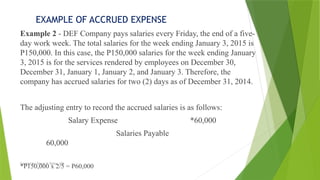

Example 2 - DEF Company pays salaries every Friday, the end of a five-

day work week. The total salaries for the week ending January 3, 2015 is

P150,000. In this case, the P150,000 salaries for the week ending January

3, 2015 is for the services rendered by employees on December 30,

December 31, January 1, January 2, and January 3. Therefore, the

company has accrued salaries for two (2) days as of December 31, 2014.

The adjusting entry to record the accrued salaries is as follows:

Salary Expense *60,000

Salaries Payable

60,000

*P150,000 x 2/5 = P60,000

EXAMPLE OF ACCRUED EXPENSE

31.

Created by: SherylV. Paliza, CPA

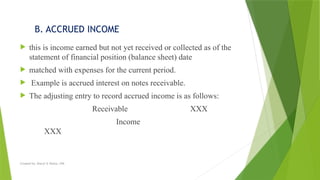

B. ACCRUED INCOME

this is income earned but not yet received or collected as of the

statement of financial position (balance sheet) date

matched with expenses for the current period.

Example is accrued interest on notes receivable.

The adjusting entry to record accrued income is as follows:

Receivable XXX

Income

XXX

32.

Created by: SherylV. Paliza, CPA

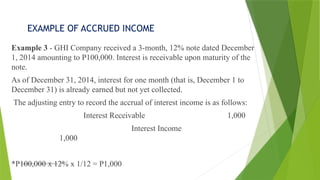

Example 3 - GHI Company received a 3-month, 12% note dated December

1, 2014 amounting to P100,000. Interest is receivable upon maturity of the

note.

As of December 31, 2014, interest for one month (that is, December 1 to

December 31) is already earned but not yet collected.

The adjusting entry to record the accrual of interest income is as follows:

Interest Receivable 1,000

Interest Income

1,000

*P100,000 x 12% x 1/12 = P1,000

EXAMPLE OF ACCRUED INCOME

33.

Created by: SherylV. Paliza, CPA

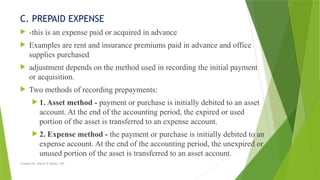

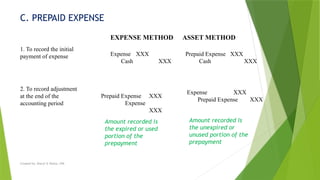

C. PREPAID EXPENSE

-this is an expense paid or acquired in advance

Examples are rent and insurance premiums paid in advance and office

supplies purchased

adjustment depends on the method used in recording the initial payment

or acquisition.

Two methods of recording prepayments:

1. Asset method - payment or purchase is initially debited to an asset

account. At the end of the accounting period, the expired or used

portion of the asset is transferred to an expense account.

2. Expense method - the payment or purchase is initially debited to an

expense account. At the end of the accounting period, the unexpired or

unused portion of the asset is transferred to an asset account.

34.

Created by: SherylV. Paliza, CPA

C. PREPAID EXPENSE

Expense XXX

Cash XXX

EXPENSE METHOD ASSET METHOD

Prepaid Expense XXX

Cash XXX

1. To record the initial

payment of expense

2. To record adjustment

at the end of the

accounting period

Prepaid Expense XXX

Expense

XXX

Expense XXX

Prepaid Expense XXX

Amount recorded is

the expired or used

portion of the

prepayment

Amount recorded is

the unexpired or

unused portion of the

prepayment

35.

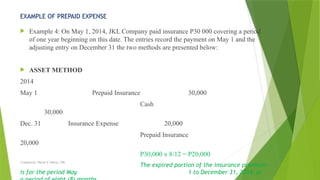

EXAMPLE OF PREPAIDEXPENSE

Example 4: On May 1, 2014, JKL Company paid insurance P30 000 covering a period

of one year beginning on this date. The entries record the payment on May 1 and the

adjusting entry on December 31 the two methods are presented below:

ASSET METHOD

2014

May 1 Prepaid Insurance 30,000

Cash

30,000

Dec. 31 Insurance Expense 20,000

Prepaid Insurance

20,000

P30,000 x 8/12 = P20,000

The expired portion of the insurance premium

is for the period May 1 to December 31, 2014, or

Created by: Sheryl V. Paliza, CPA

36.

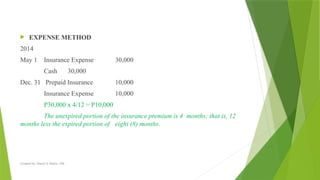

EXPENSE METHOD

2014

May1 Insurance Expense 30,000

Cash 30,000

Dec. 31 Prepaid Insurance 10,000

Insurance Expense 10,000

P30,000 x 4/12 = P10,000

The unexpired portion of the insurance premium is 4 months; that is, 12

months less the expired portion of eight (8) months.

Created by: Sheryl V. Paliza, CPA

37.

Created by: SherylV. Paliza, CPA

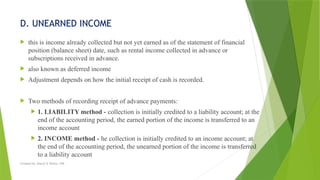

D. UNEARNED INCOME

this is income already collected but not yet earned as of the statement of financial

position (balance sheet) date, such as rental income collected in advance or

subscriptions received in advance.

also known as deferred income

Adjustment depends on how the initial receipt of cash is recorded.

Two methods of recording receipt of advance payments:

1. LIABILITY method - collection is initially credited to a liability account; at the

end of the accounting period, the earned portion of the income is transferred to an

income account

2. INCOME method - he collection is initially credited to an income account; at

the end of the accounting period, the unearned portion of the income is transferred

to a liability account

38.

Created by: SherylV. Paliza, CPA

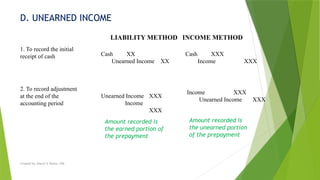

D. UNEARNED INCOME

Cash XX

Unearned Income XX

LIABILITY METHOD INCOME METHOD

Cash XXX

Income XXX

1. To record the initial

receipt of cash

2. To record adjustment

at the end of the

accounting period

Unearned Income XXX

Income

XXX

Income XXX

Unearned Income XXX

Amount recorded is

the earned portion of

the prepayment

Amount recorded is

the unearned portion

of the prepayment

39.

Created by: SherylV. Paliza, CPA

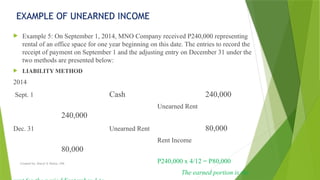

EXAMPLE OF UNEARNED INCOME

Example 5: On September 1, 2014, MNO Company received P240,000 representing

rental of an office space for one year beginning on this date. The entries to record the

receipt of payment on September 1 and the adjusting entry on December 31 under the

two methods are presented below:

LIABILITY METHOD

2014

Sept. 1 Cash 240,000

Unearned Rent

240,000

Dec. 31 Unearned Rent 80,000

Rent Income

80,000

P240,000 x 4/12 = P80,000

The earned portion is the

40.

Created by: SherylV. Paliza, CPA

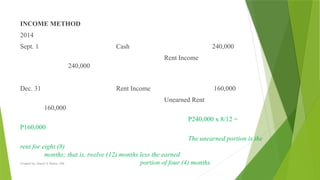

INCOME METHOD

2014

Sept. 1 Cash 240,000

Rent Income

240,000

Dec. 31 Rent Income 160,000

Unearned Rent

160,000

P240,000 x 8/12 =

P160,000

The unearned portion is the

rent for eight (8)

months; that is, twelve (12) months less the earned

portion of four (4) months.

41.

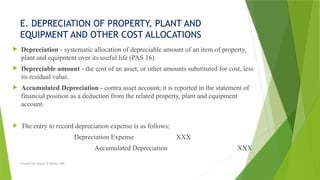

E. DEPRECIATION OFPROPERTY, PLANT AND

EQUIPMENT AND OTHER COST ALLOCATIONS

Depreciation - systematic allocation of depreciable amount of an item of property,

plant and equipment over its useful life (PAS 16)

Depreciable amount - the cost of an asset, or other amounts substituted for cost, less

its residual value.

Accumulated Depreciation - contra asset account; it is reported in the statement of

financial position as a deduction from the related property, plant and equipment

account.

The entry to record depreciation expense is as follows:

Depreciation Expense XXX

Accumulated Depreciation XXX

Created by: Sheryl V. Paliza, CPA

42.

Created by: SherylV. Paliza, CPA

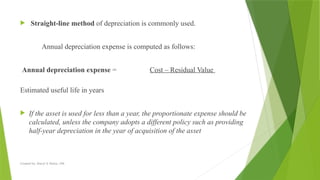

Straight-line method of depreciation is commonly used.

Annual depreciation expense is computed as follows:

Annual depreciation expense = Cost – Residual Value

Estimated useful life in years

If the asset is used for less than a year, the proportionate expense should be

calculated, unless the company adopts a different policy such as providing

half-year depreciation in the year of acquisition of the asset

43.

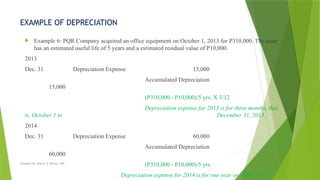

EXAMPLE OF DEPRECIATION

Example 6: PQR Company acquired an office equipment on October 1, 2013 for P310,000. The asset

has an estimated useful life of 5 years and a estimated residual value of P10,000.

2013

Dec. 31 Depreciation Expense 15,000

Accumulated Depreciation

15,000

(P310,000 - P10,000)/5 yrs. X 3/12

Depreciation expense for 2013 is for three months, that

is, October 1 to December 31, 2013.

2014

Dec. 31 Depreciation Expense 60,000

Accumulated Depreciation

60,000

(P310,000 - P10,000)/5 yrs.

Depreciation expense for 2014 is for one year or twelve (12)

Created by: Sheryl V. Paliza, CPA

44.

Created by: SherylV. Paliza, CPA

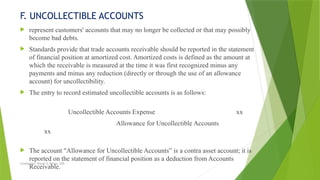

F. UNCOLLECTIBLE ACCOUNTS

represent customers' accounts that may no longer be collected or that may possibly

become bad debts.

Standards provide that trade accounts receivable should be reported in the statement

of financial position at amortized cost. Amortized costs is defined as the amount at

which the receivable is measured at the time it was first recognized minus any

payments and minus any reduction (directly or through the use of an allowance

account) for uncollectibility.

The entry to record estimated uncollectible accounts is as follows:

Uncollectible Accounts Expense xx

Allowance for Uncollectible Accounts

xx

The account "Allowance for Uncollectible Accounts” is a contra asset account; it is

reported on the statement of financial position as a deduction from Accounts

Receivable.

45.

Created by: SherylV. Paliza, CPA

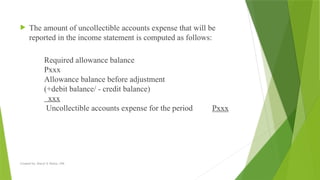

The amount of uncollectible accounts expense that will be

reported in the income statement is computed as follows:

Required allowance balance

Pxxx

Allowance balance before adjustment

(+debit balance/ - credit balance)

xxx

Uncollectible accounts expense for the period Pxxx

46.

Created by: SherylV. Paliza, CPA

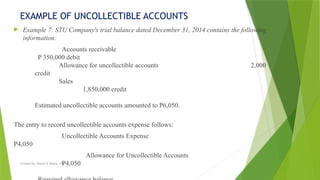

Example 7: STU Company's trial balance dated December 31, 2014 contains the following

information:

Accounts receivable

P 350,000 debit

Allowance for uncollectible accounts 2,000

credit

Sales

1,850,000 credit

Estimated uncollectible accounts amounted to P6,050.

The entry to record uncollectible accounts expense follows:

Uncollectible Accounts Expense

P4,050

Allowance for Uncollectible Accounts

P4,050

EXAMPLE OF UNCOLLECTIBLE ACCOUNTS

47.

Created by: SherylV. Paliza, CPA

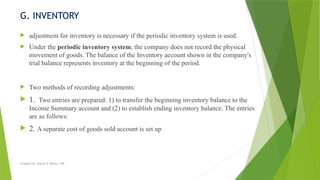

G. INVENTORY

adjustment for inventory is necessary if the periodic inventory system is used.

Under the periodic inventory system, the company does not record the physical

movement of goods. The balance of the Inventory account shown in the company's

trial balance represents inventory at the beginning of the period.

Two methods of recording adjustments:

1. Two entries are prepared: 1) to transfer the beginning inventory balance to the

Income Summary account and (2) to establish ending inventory balance. The entries

are as follows:

2. A separate cost of goods sold account is set up

48.

Created by: SherylV. Paliza, CPA

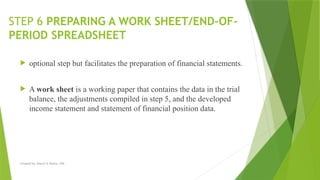

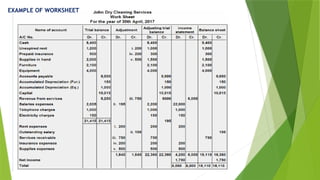

STEP 6 PREPARING A WORK SHEET/END-OF-

PERIOD SPREADSHEET

optional step but facilitates the preparation of financial statements.

A work sheet is a working paper that contains the data in the trial

balance, the adjustments compiled in step 5, and the developed

income statement and statement of financial position data.

Created by: SherylV. Paliza, CPA

STEP 7 PREPARING THE FINANCIAL

STATEMENTS

described as the end product of the accounting process.

The data reported in the statements are taken from the completed work

sheet. However, if a work sheet is not prepared, the adjusting data must be

journalized and posted because the data reported in the statements are taken

from the updated balances of the accounts in the general ledger.

51.

Created by: SherylV. Paliza, CPA

PAS 1 provides that a complete set of financial statements shall

consist of the following:

1. Statement of financial position (balance sheet)

2. Statement of comprehensive income (income statement)

3. Statement of cash flows

4. Statement of changes in owners' equity

5. Notes to FS

52.

Created by: SherylV. Paliza, CPA

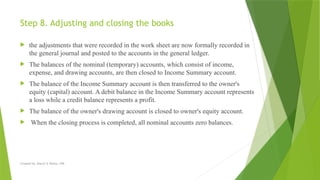

Step 8. Adjusting and closing the books

the adjustments that were recorded in the work sheet are now formally recorded in

the general journal and posted to the accounts in the general ledger.

The balances of the nominal (temporary) accounts, which consist of income,

expense, and drawing accounts, are then closed to Income Summary account.

The balance of the Income Summary account is then transferred to the owner's

equity (capital) account. A debit balance in the Income Summary account represents

a loss while a credit balance represents a profit.

The balance of the owner's drawing account is closed to owner's equity account.

When the closing process is completed, all nominal accounts zero balances.

53.

Created by: SherylV. Paliza, CPA

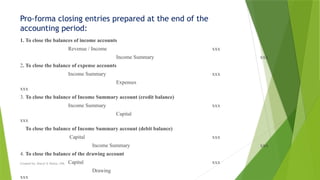

Pro-forma closing entries prepared at the end of the

accounting period:

1. To close the balances of income accounts

Revenue / Income xxx

Income Summary xxx

2. To close the balance of expense accounts

Income Summary xxx

Expenses

xxx

3. To close the balance of Income Summary account (credit balance)

Income Summary xxx

Capital

xxx

To close the balance of Income Summary account (debit balance)

Capital xxx

Income Summary xxx

4. To close the balance of the drawing account

Capital xxx

Drawing

xxx

54.

Created by: SherylV. Paliza, CPA

STEP 9 PREPARING A POST-CLOSING

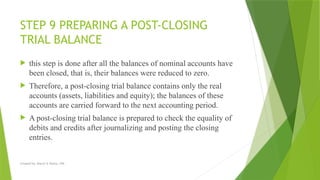

TRIAL BALANCE

this step is done after all the balances of nominal accounts have

been closed, that is, their balances were reduced to zero.

Therefore, a post-closing trial balance contains only the real

accounts (assets, liabilities and equity); the balances of these

accounts are carried forward to the next accounting period.

A post-closing trial balance is prepared to check the equality of

debits and credits after journalizing and posting the closing

entries.

55.

Created by: SherylV. Paliza, CPA

STEP 10 REVERSING THE ACCOUNTS

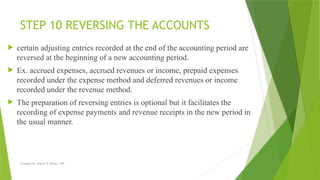

certain adjusting entries recorded at the end of the accounting period are

reversed at the beginning of a new accounting period.

Ex. accrued expenses, accrued revenues or income, prepaid expenses

recorded under the expense method and deferred revenues or income

recorded under the revenue method.

The preparation of reversing entries is optional but it facilitates the

recording of expense payments and revenue receipts in the new period in

the usual manner.

56.

Created by: SherylV. Paliza, CPA

The adjustments that will be reversed if reversing entries are prepared and the

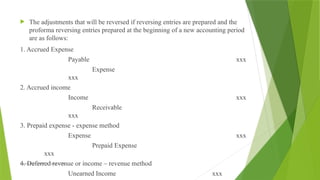

proforma reversing entries prepared at the beginning of a new accounting period

are as follows:

1. Accrued Expense

Payable xxx

Expense

xxx

2. Accrued income

Income xxx

Receivable

xxx

3. Prepaid expense - expense method

Expense xxx

Prepaid Expense

xxx

4. Deferred revenue or income – revenue method

Unearned Income xxx

Editor's Notes

#5 Introduced by Fra Luca Pacioli – father of accounting

![Tally.ERP 9 6.6.3 Crack 2025 Free Download Full Version [Latest]](https://cdn.slidesharecdn.com/ss_thumbnails/8881-250505005125-85bafed8-250715121305-bde34527-thumbnail.jpg?width=640&height=640&fit=bounds)