Downloaded 127 times

Subsidiary ledgers are subsets of the general ledger that provide detailed records for specific accounts. There are typically three main control accounts: sales ledger for accounts receivable, purchases ledger for accounts payable, and inventory subsidiary ledger. The subsidiary ledgers track individual customer and supplier balances as well as inventory stock details. The totals from the subsidiary ledgers must equal the balances in the related general ledger control accounts. Subsidiary ledgers help locate errors, check accuracy, and provide ready totals for financial reporting.

Definition and overview of subsidiary ledgers, subledgers, and control accounts in accounting.

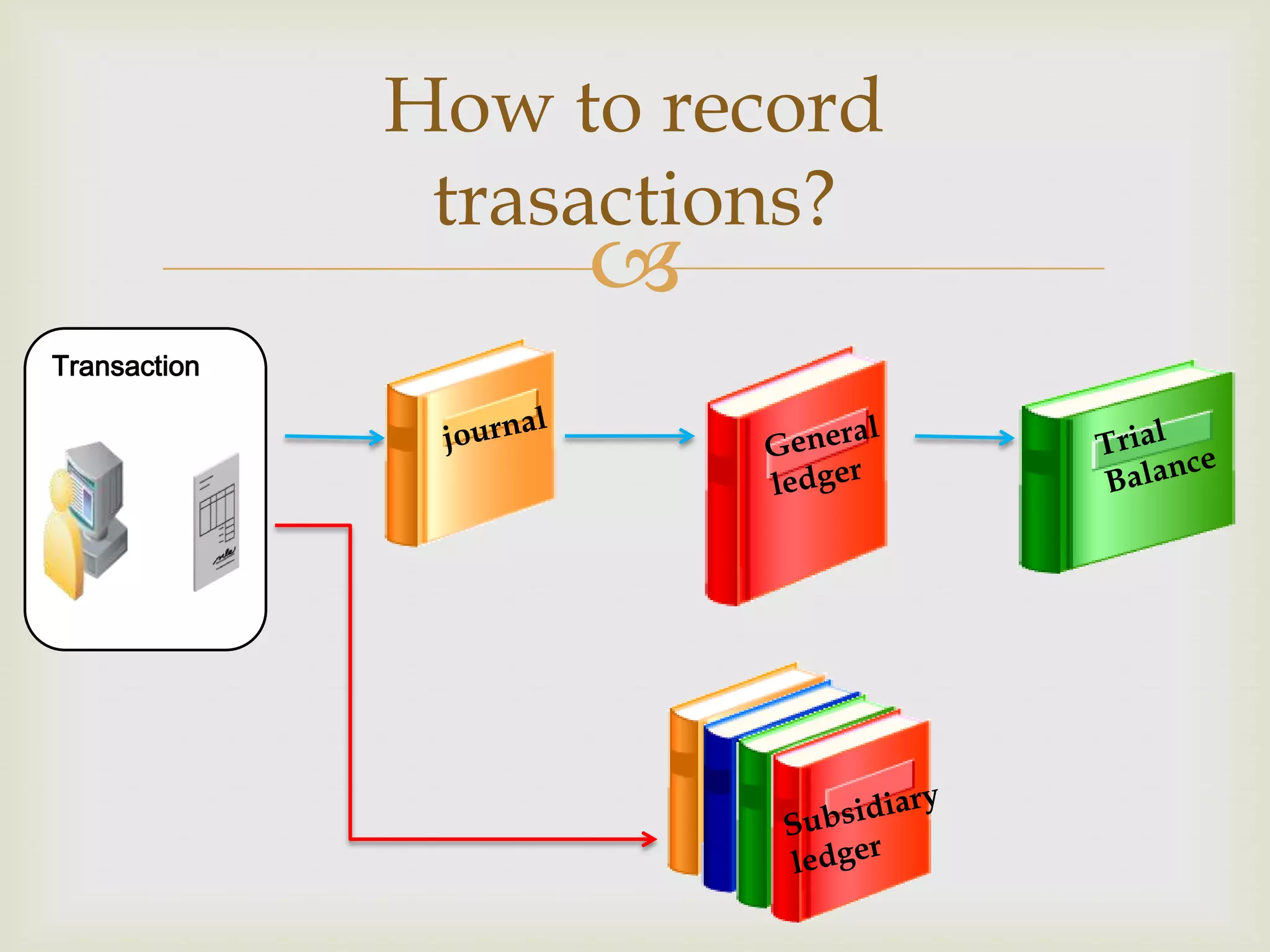

Introduction to the recording of transactions in accounting through subsidiary ledgers.

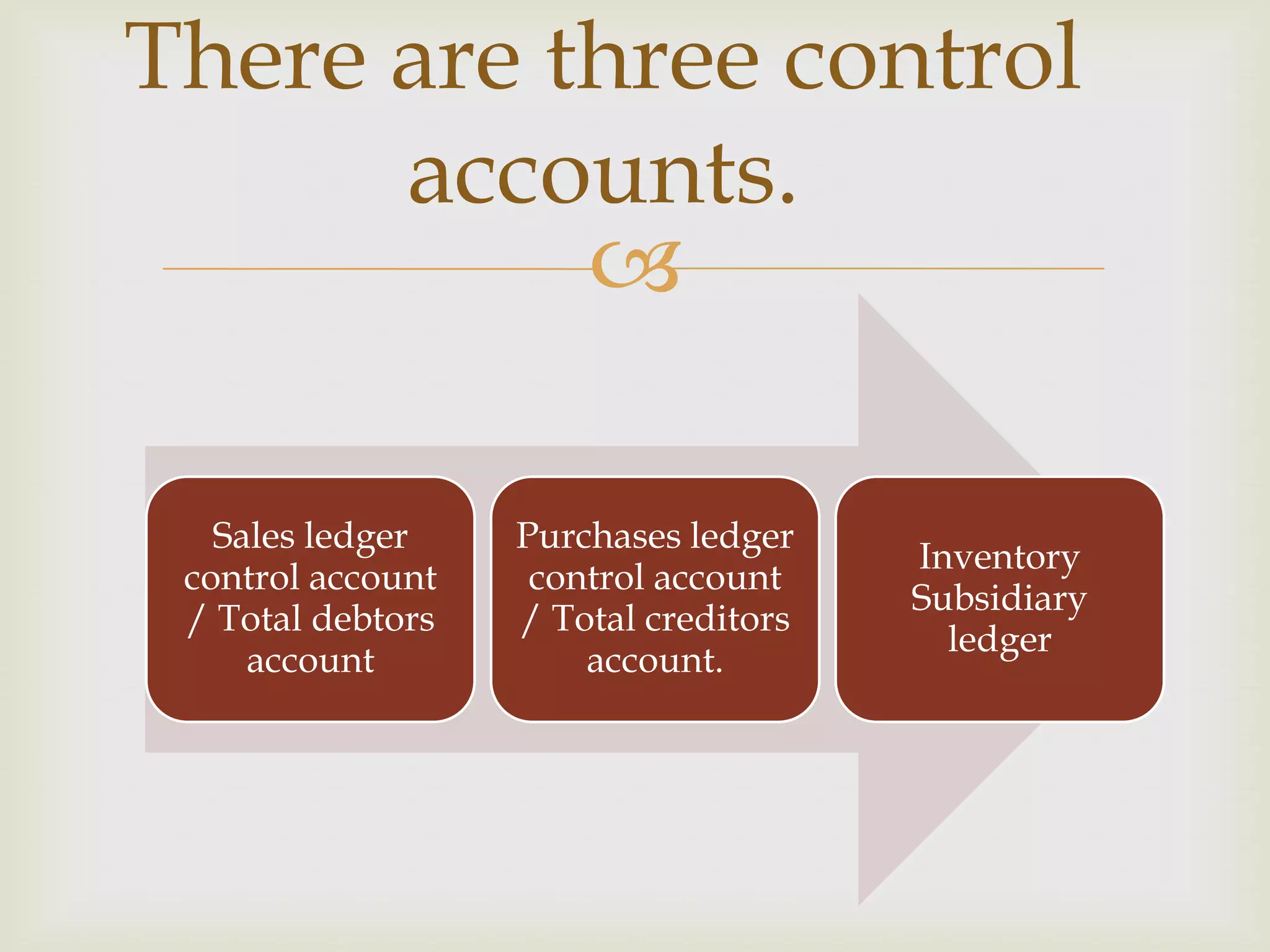

Identification of three major control accounts: Sales ledger, Purchases ledger, Inventory subsidiary ledger.

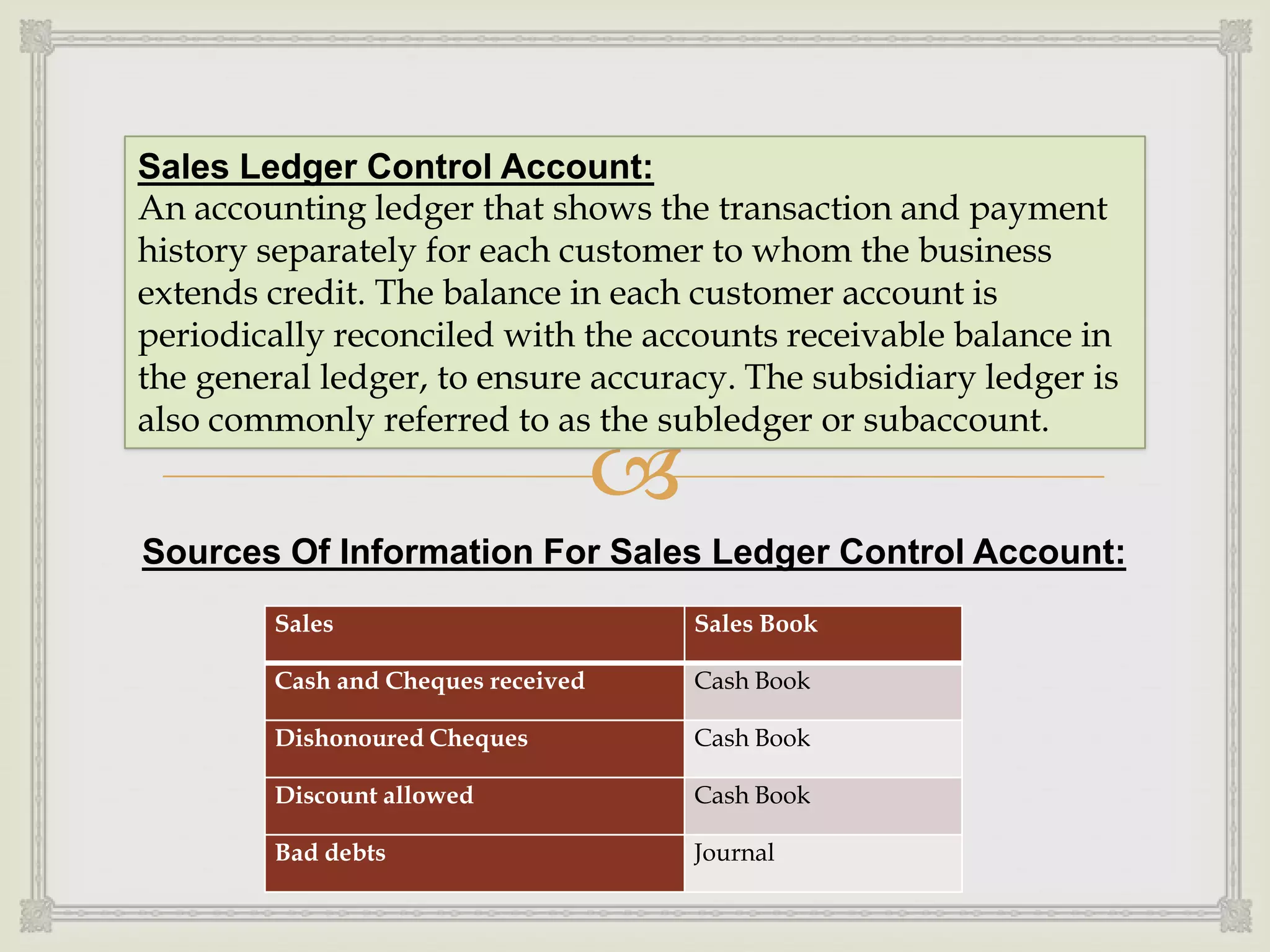

Details of the Sales Ledger Control Account and its reconciliation with accounts receivable.

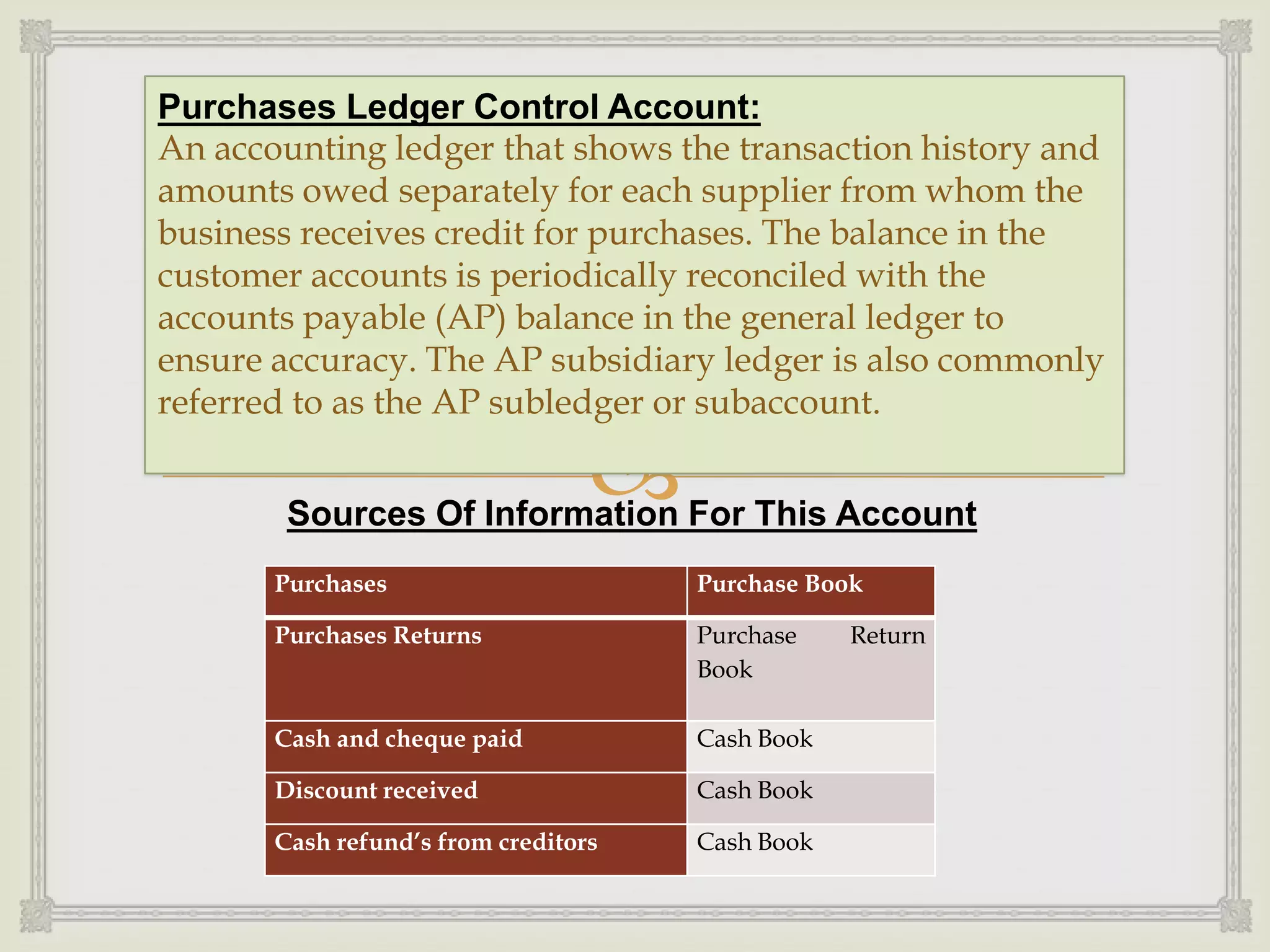

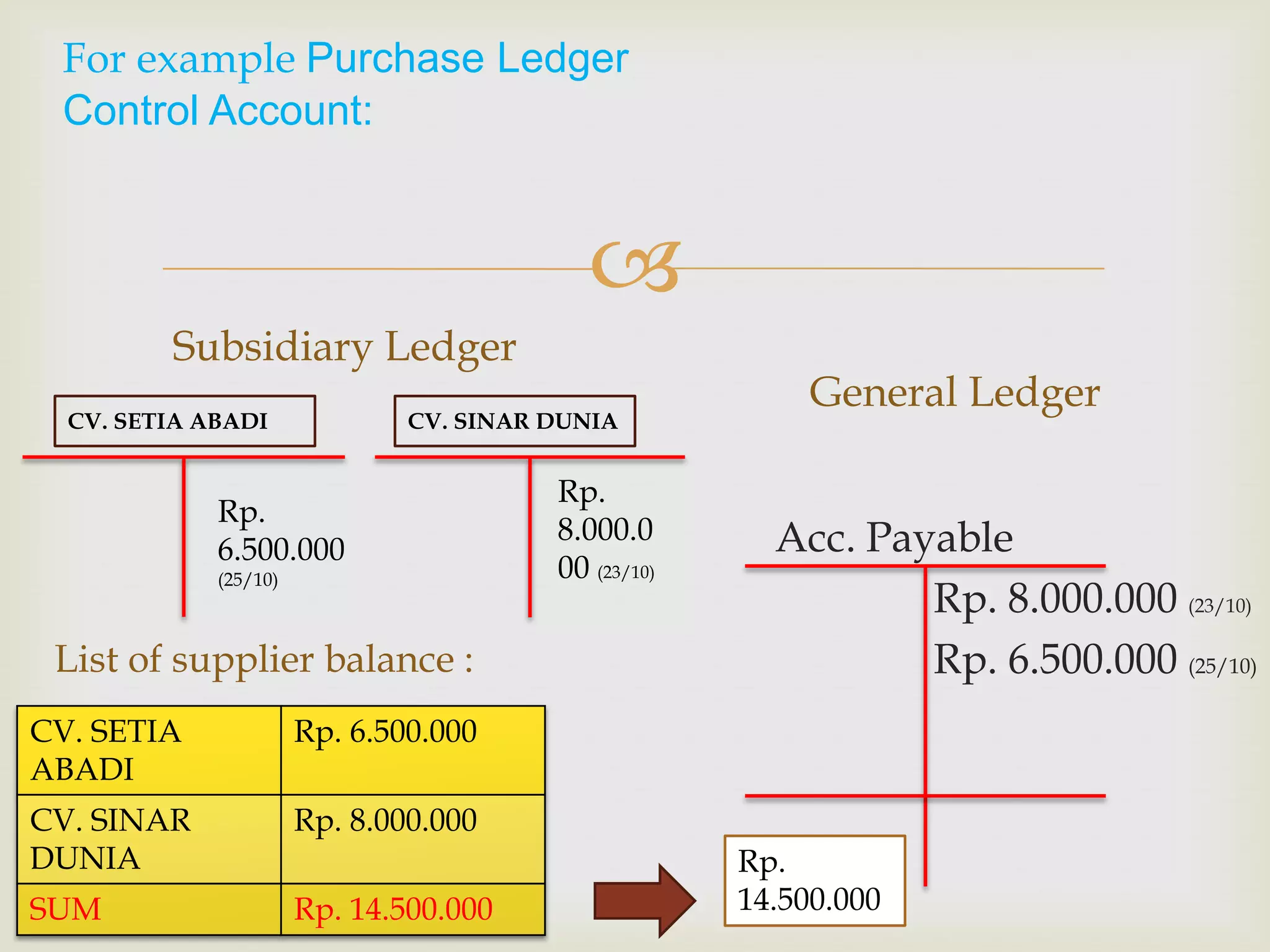

Overview of the Purchases Ledger Control Account and its reconciliation with accounts payable.

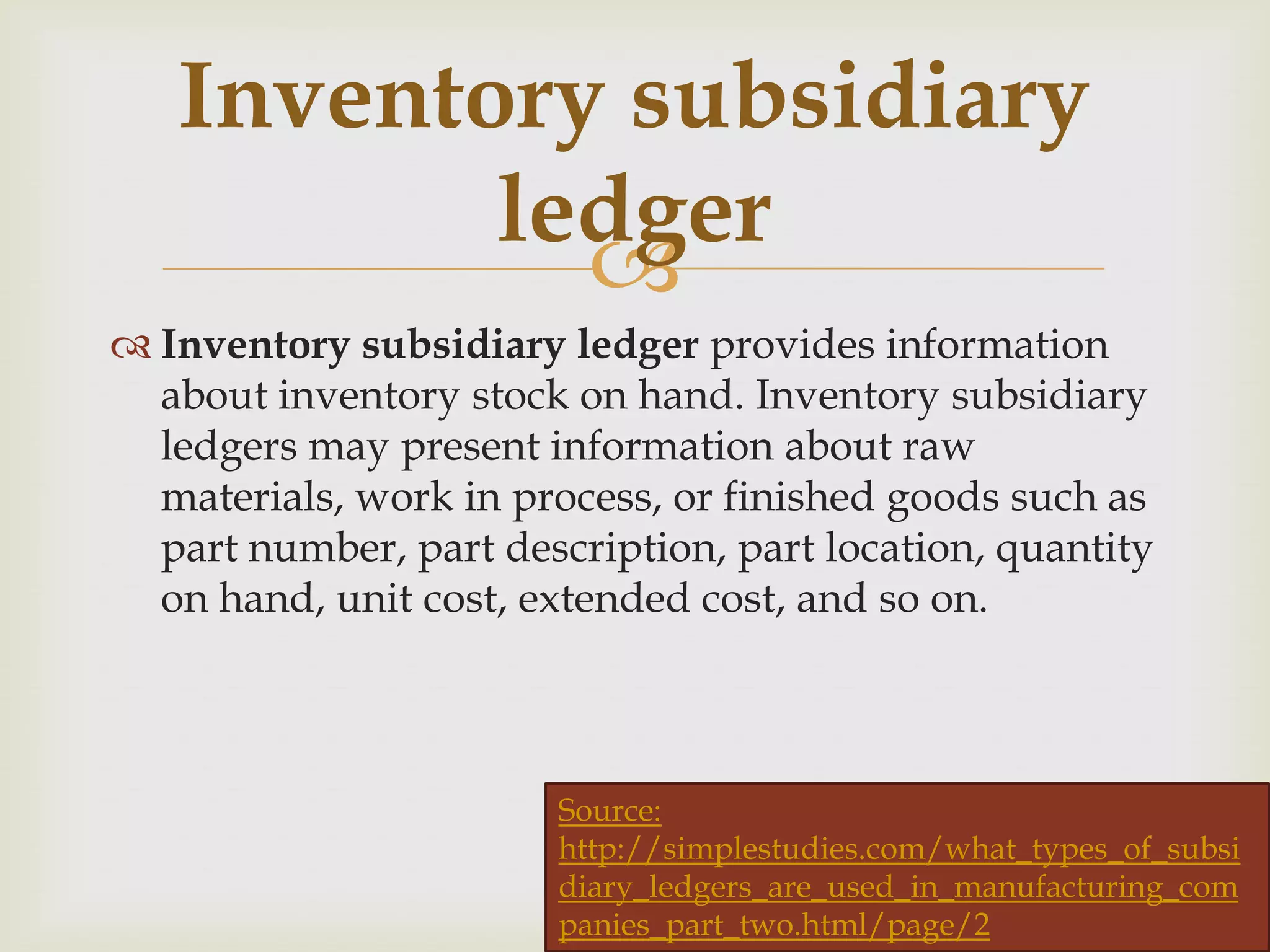

Information provided by the inventory subsidiary ledger regarding stock levels and costs.

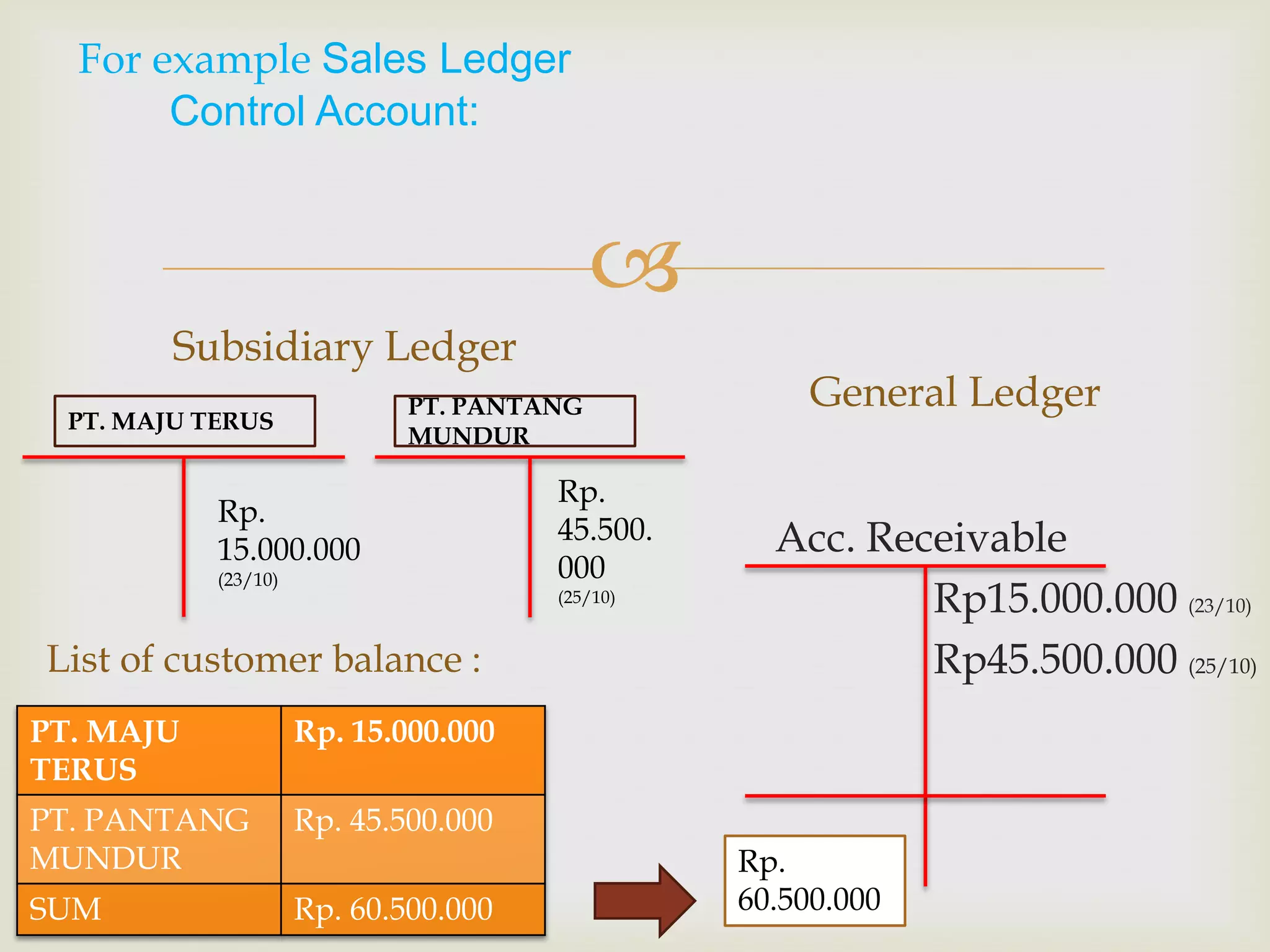

Example illustrating the Sales Ledger Control Account with customer balances and general ledger.

Example illustrating the Purchases Ledger Control Account with supplier balances and general ledger.

Example demonstrating inventory subsidiary ledger with balances of bolts and nuts.

Advantages of control accounts in error detection, accuracy checking, and fraud prevention.

Summary of the importance of subsidiary ledgers for tracking receivables, payables, and inventory.

Closing of the presentation.