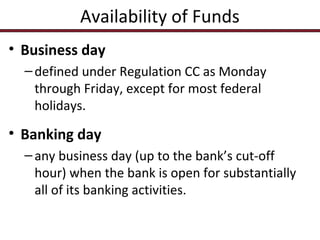

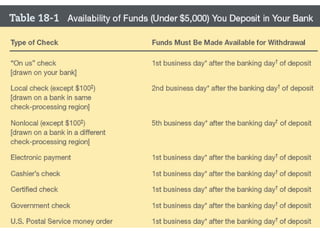

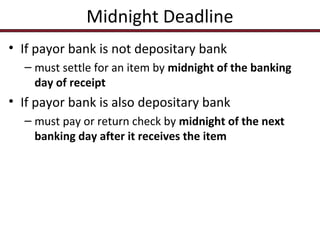

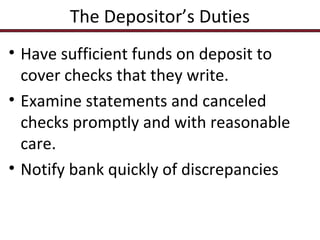

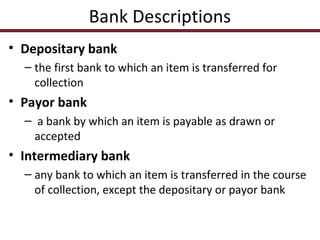

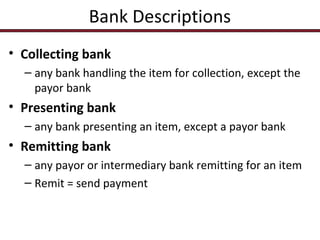

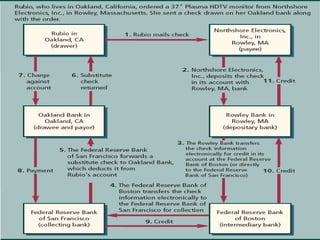

This document outlines key concepts regarding bank-depositor relationships and the check collection process. It discusses the duties of both banks and depositors, including a bank's duty to honor checks and protect funds. The document also describes the check collection process, defining terms like depositary bank, payor bank, and intermediary bank. It explains laws governing checks, like the Check 21 Act, which allows for electronic check processing and substitute checks. The Electronic Funds Transfer Act and consumer protections for electronic banking are also summarized.