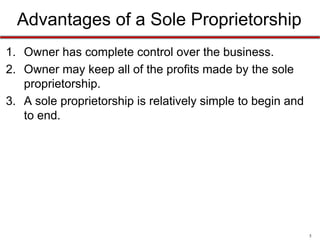

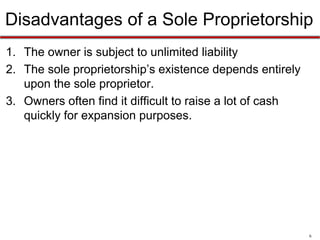

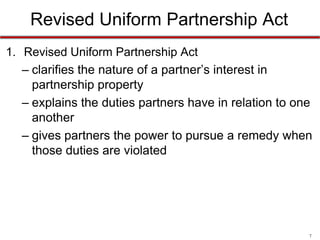

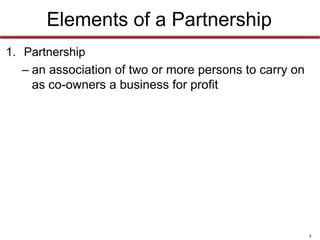

This document discusses different types of business organizations including sole proprietorships and partnerships. It defines sole proprietorships and outlines their advantages and disadvantages. It describes the Revised Uniform Partnership Act and elements of a partnership. It explains the differences between entity and aggregate theories of partnership. It discusses partnership formation, property rights, management duties, dissociation vs dissolution, and types of partnerships like limited liability partnerships and limited partnerships.