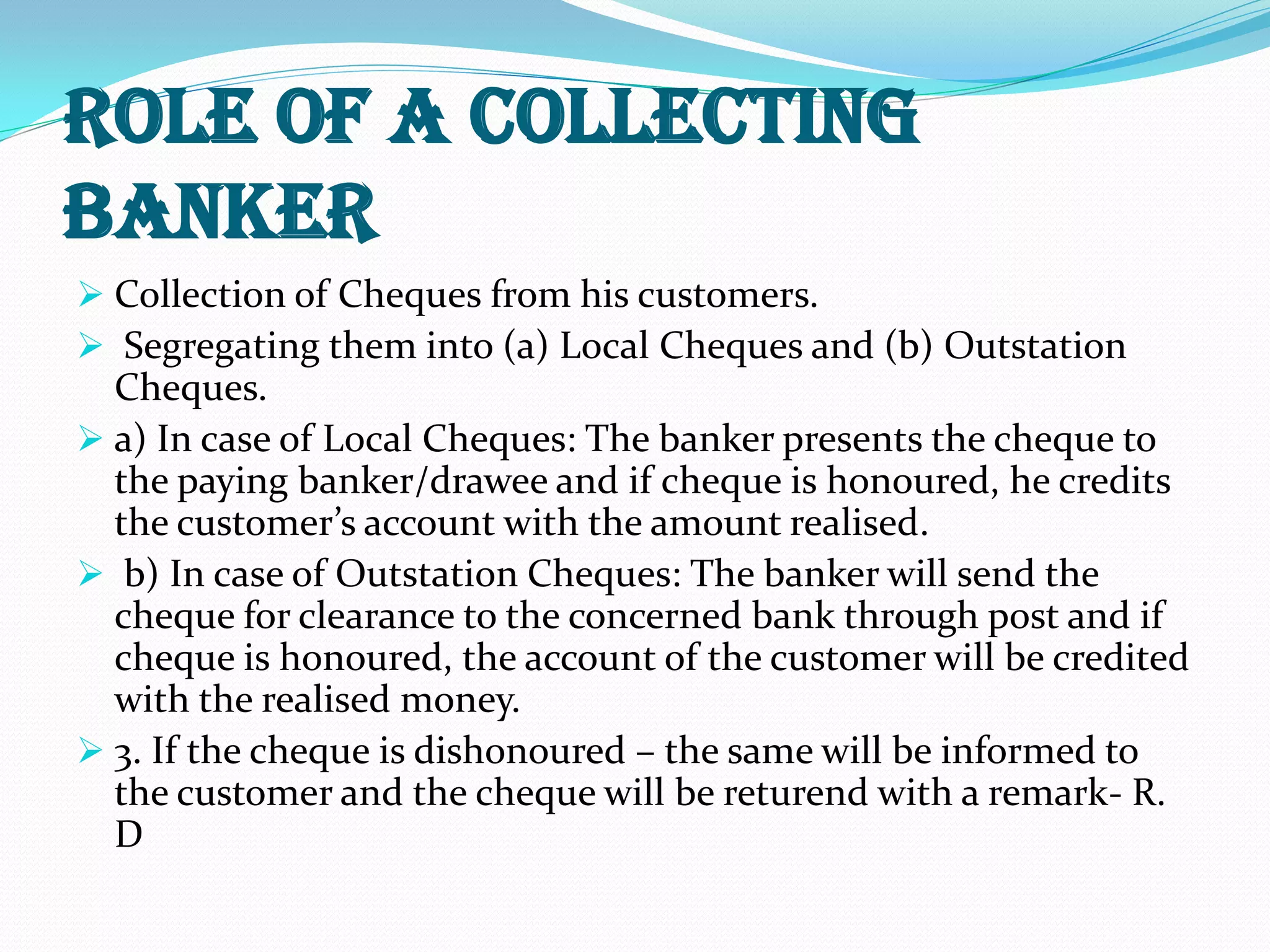

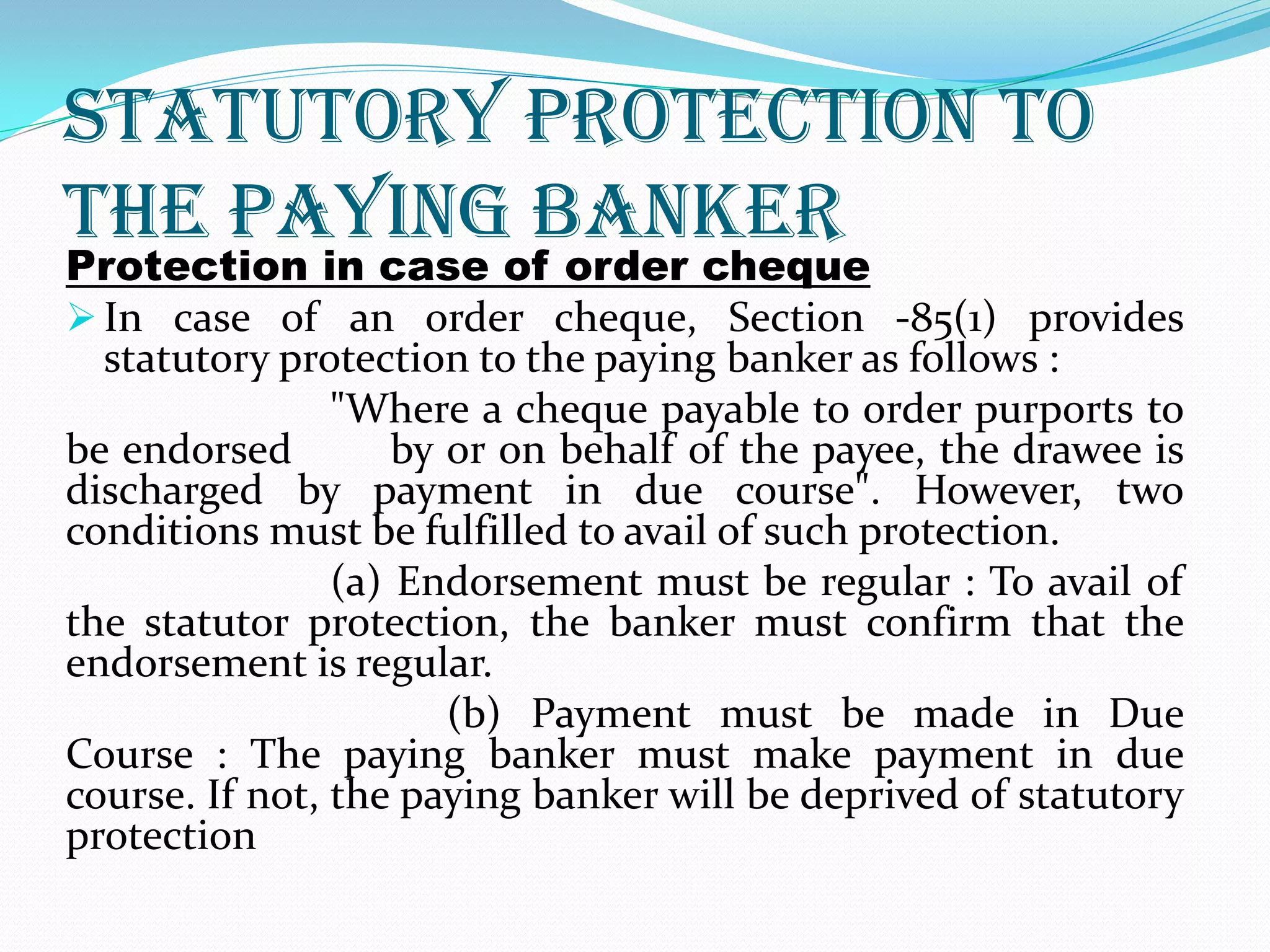

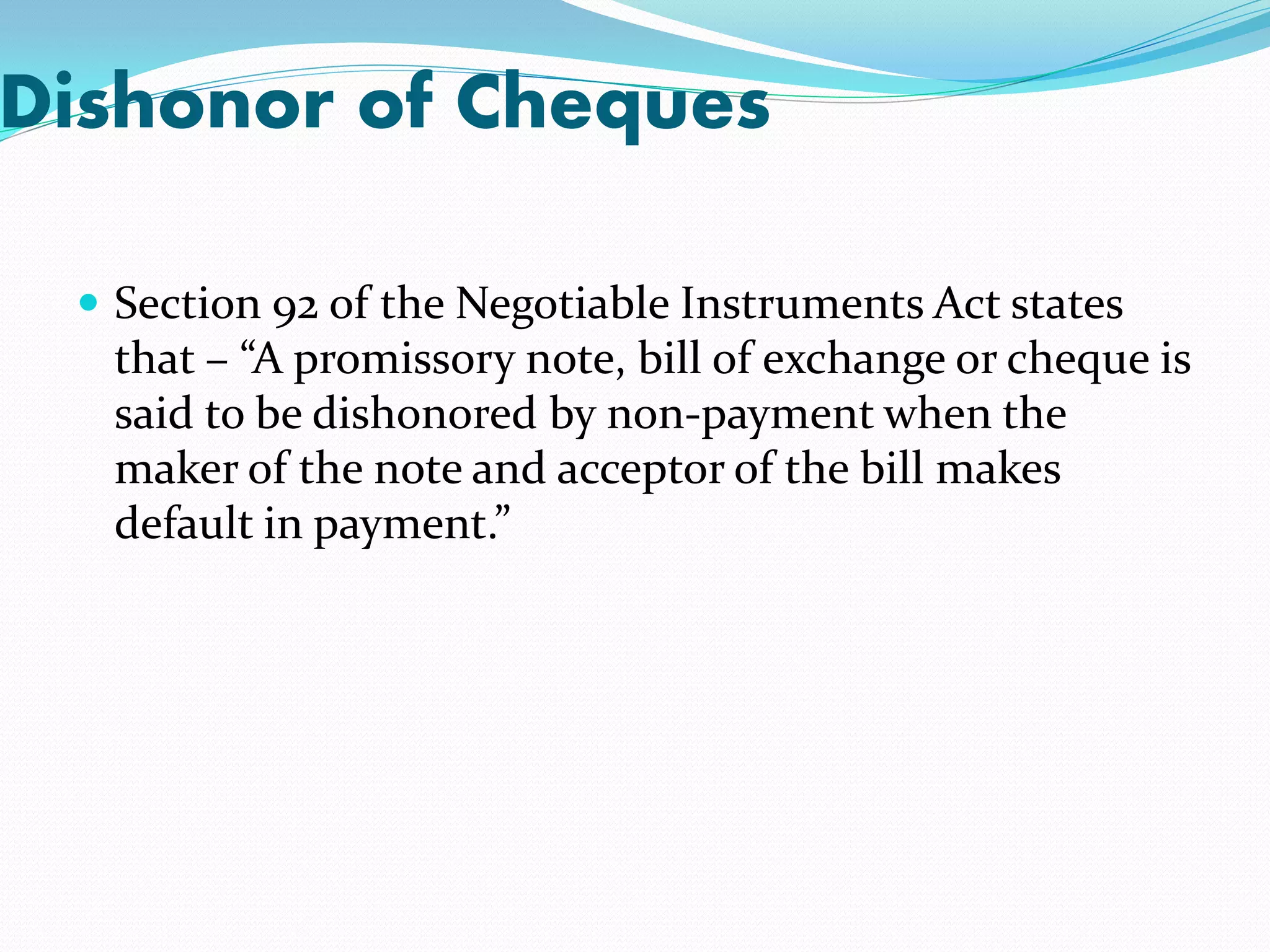

Finance and banking play a key role in modern business and economic development. The document discusses various aspects of the banker-customer relationship including general relationships as debtor-creditor and special relationships as agent-principal or trustee-beneficiary. It also covers the roles and duties of collecting bankers who undertake cheque collection and paying bankers who honor cheques drawn on their banks.