Downloaded 119 times

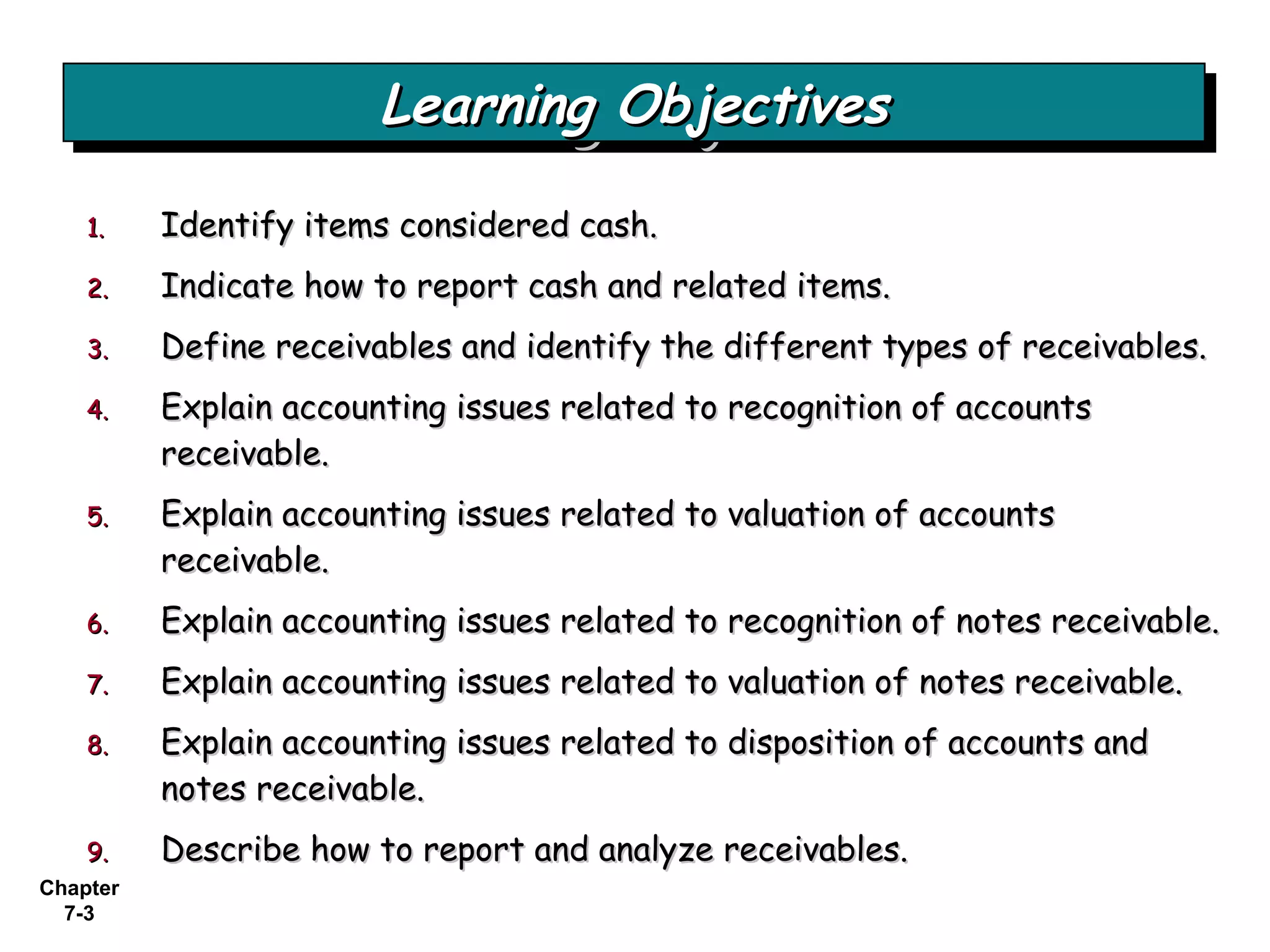

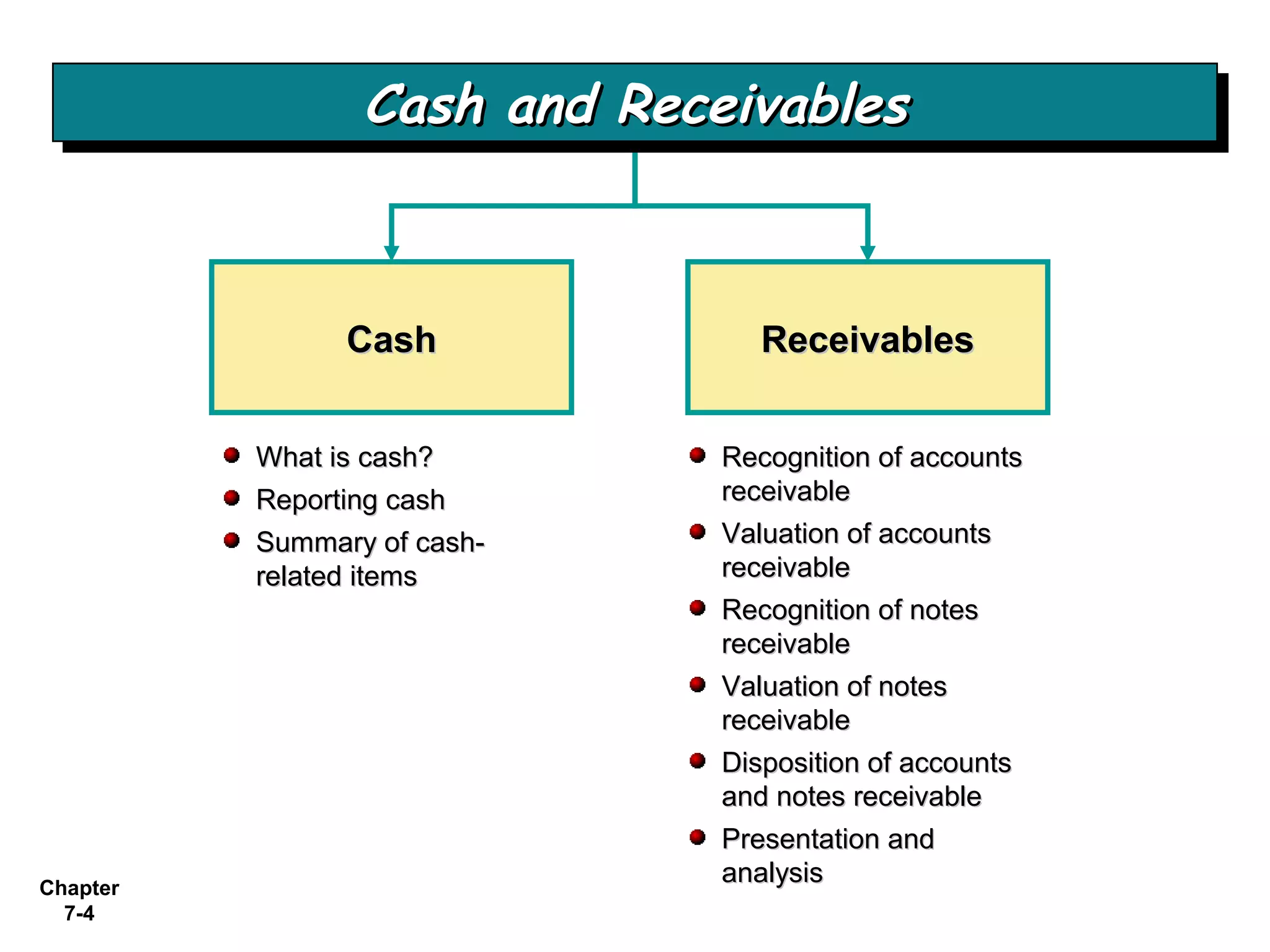

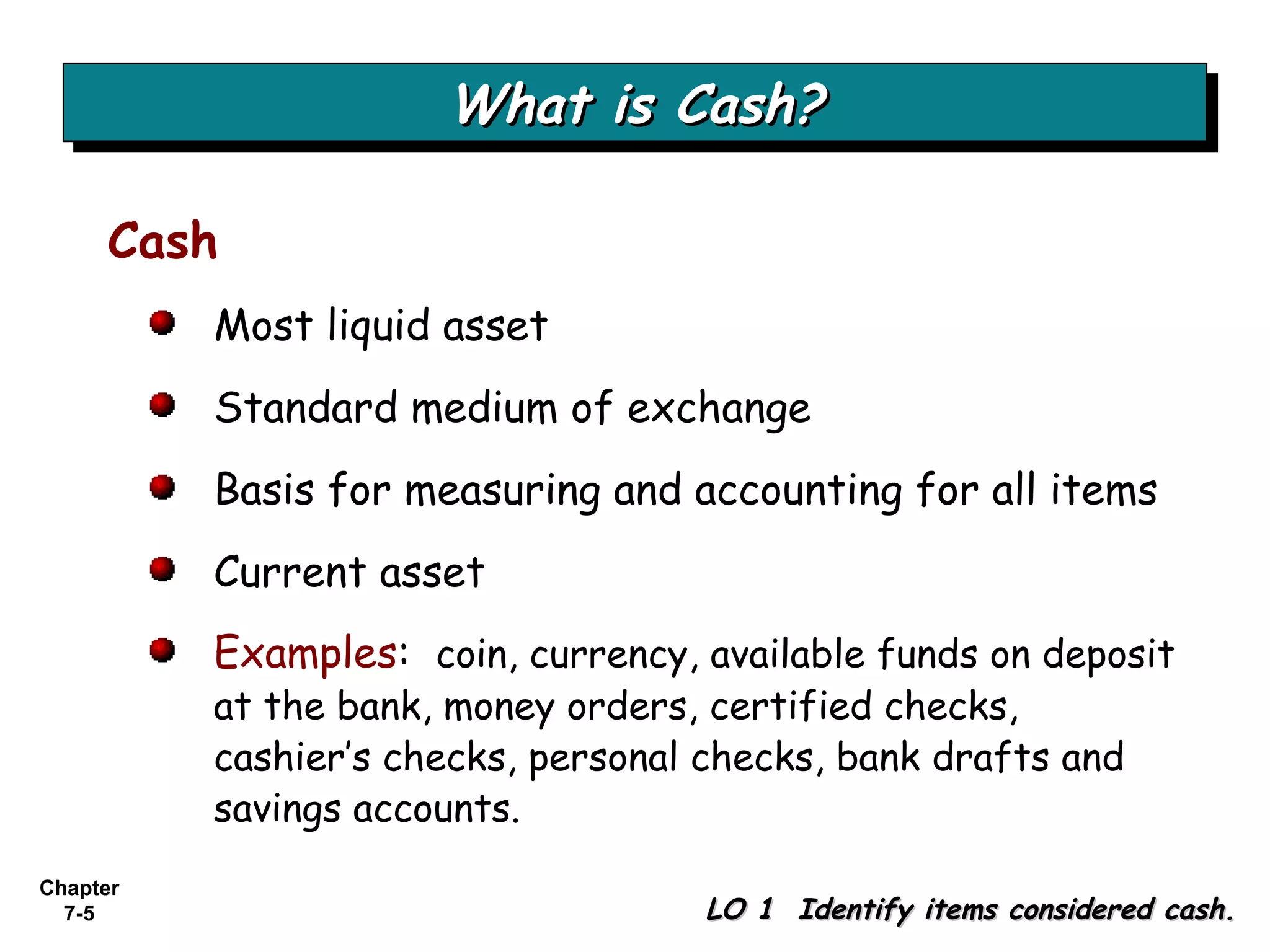

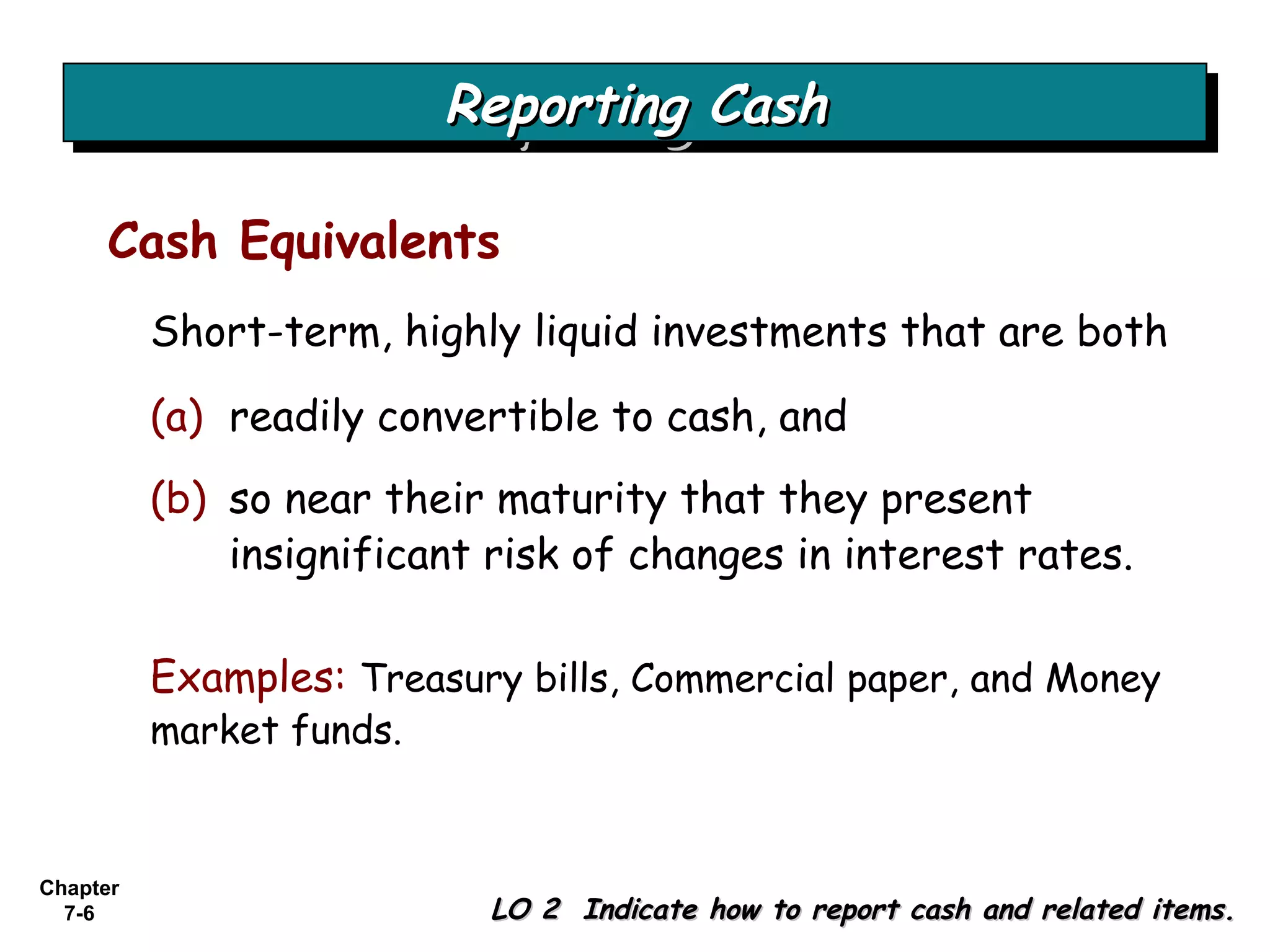

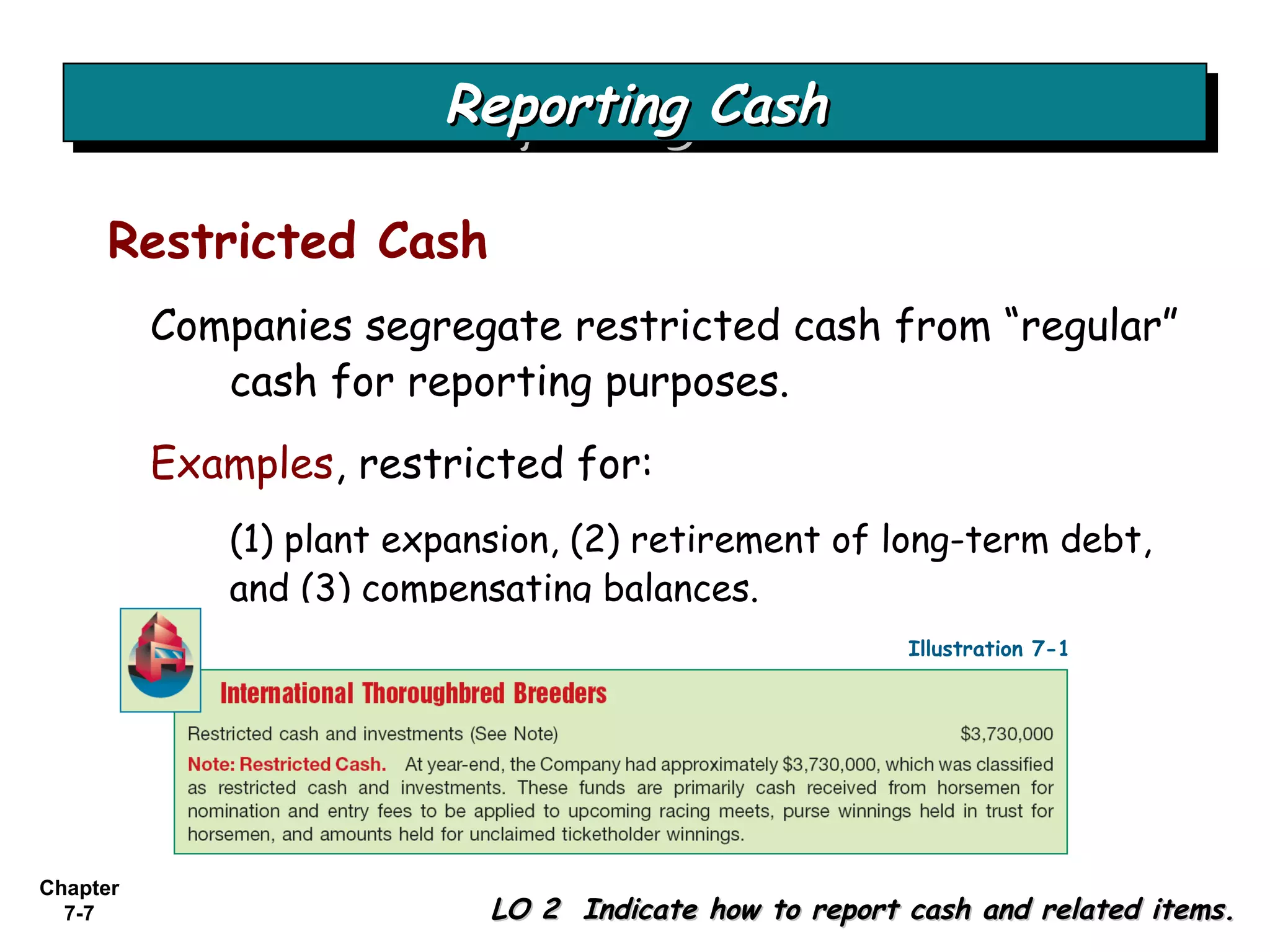

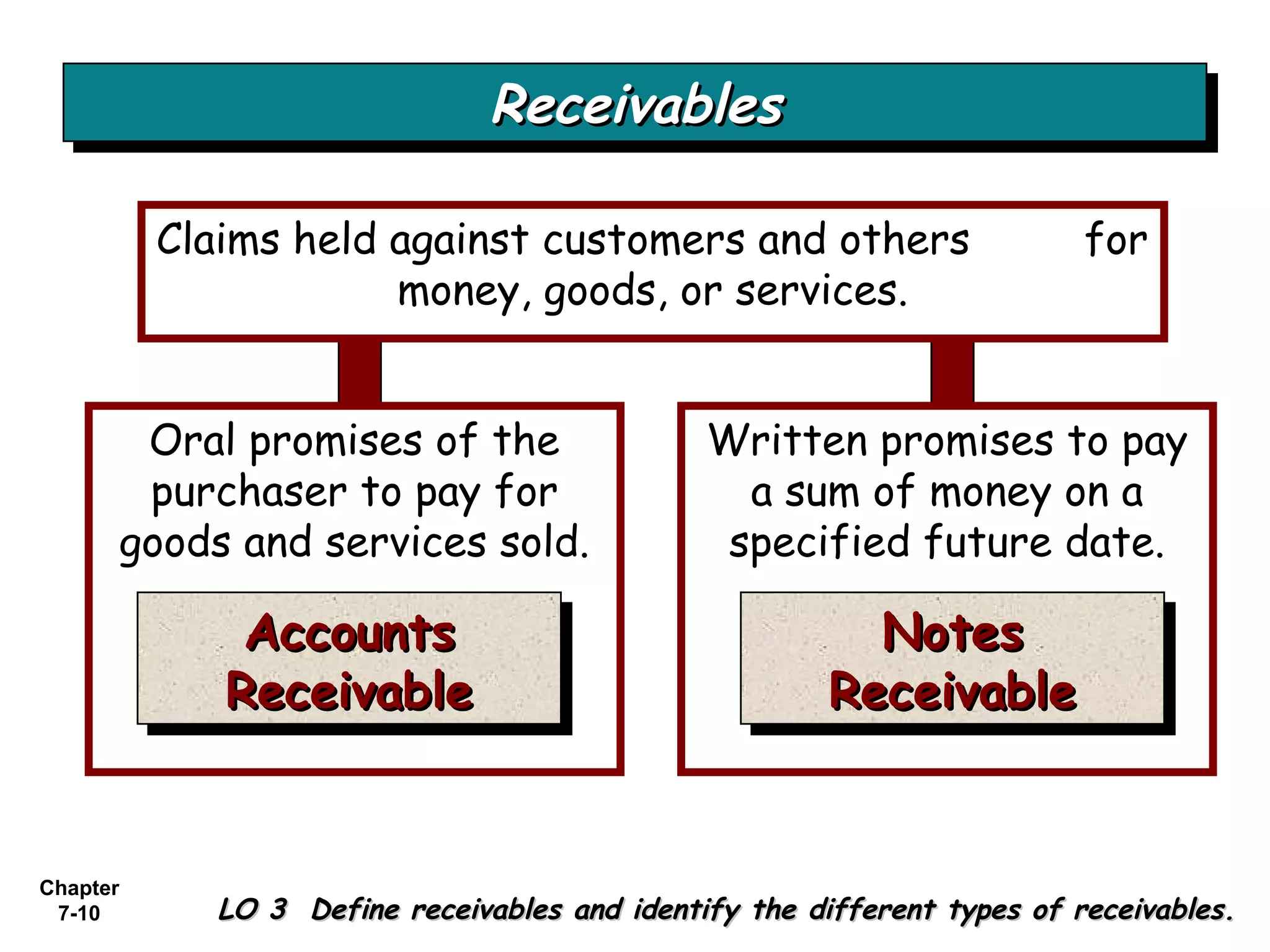

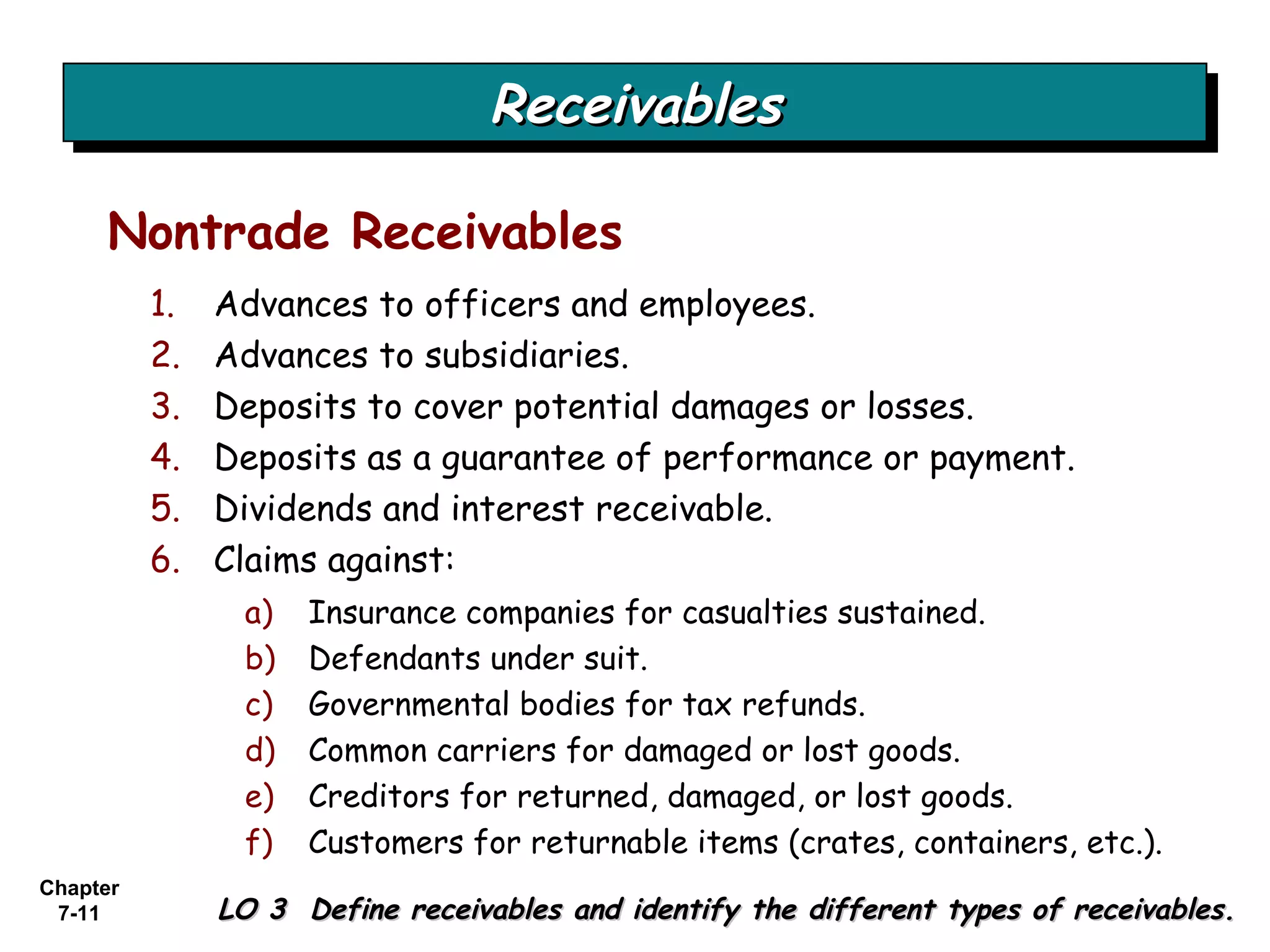

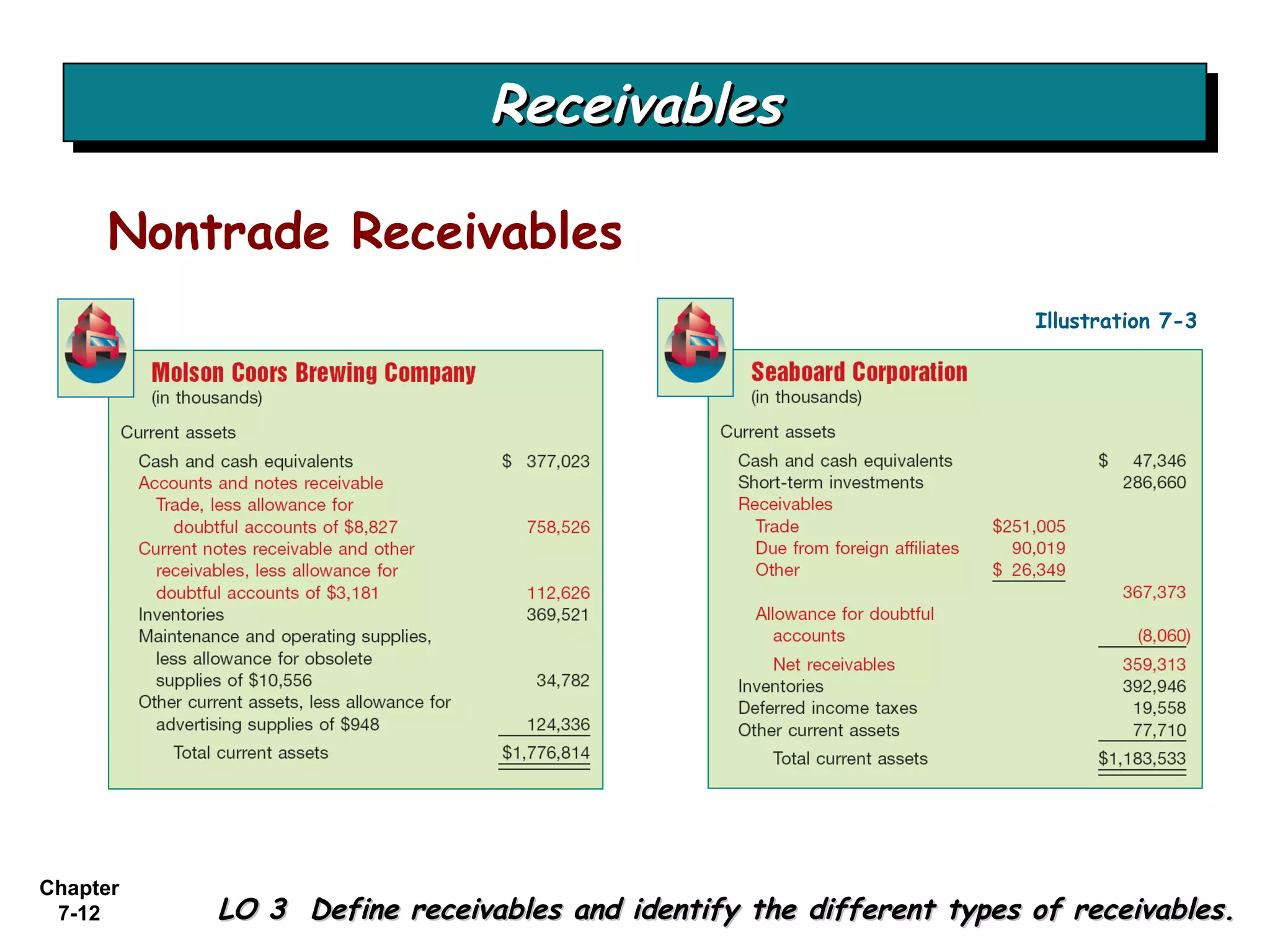

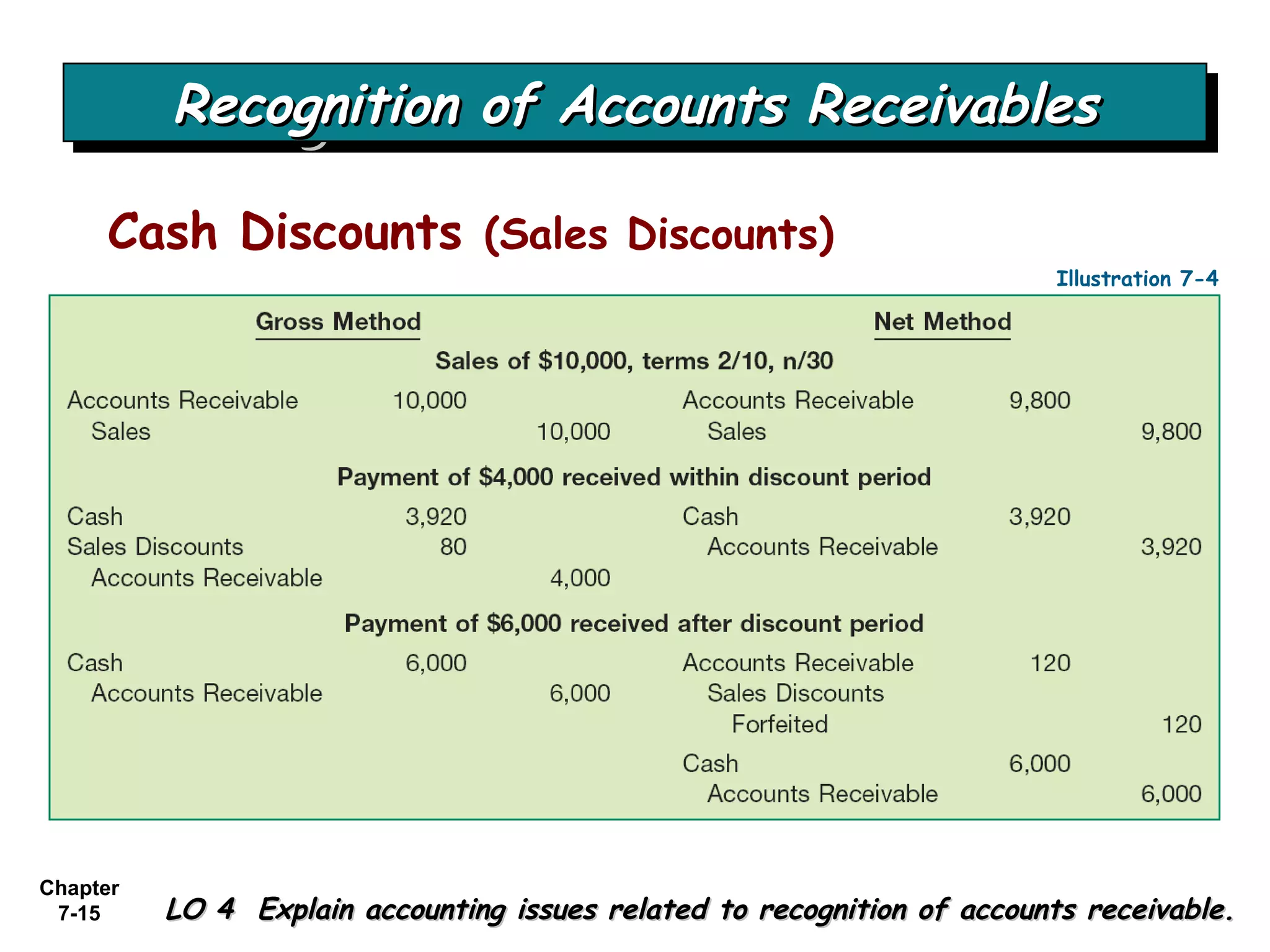

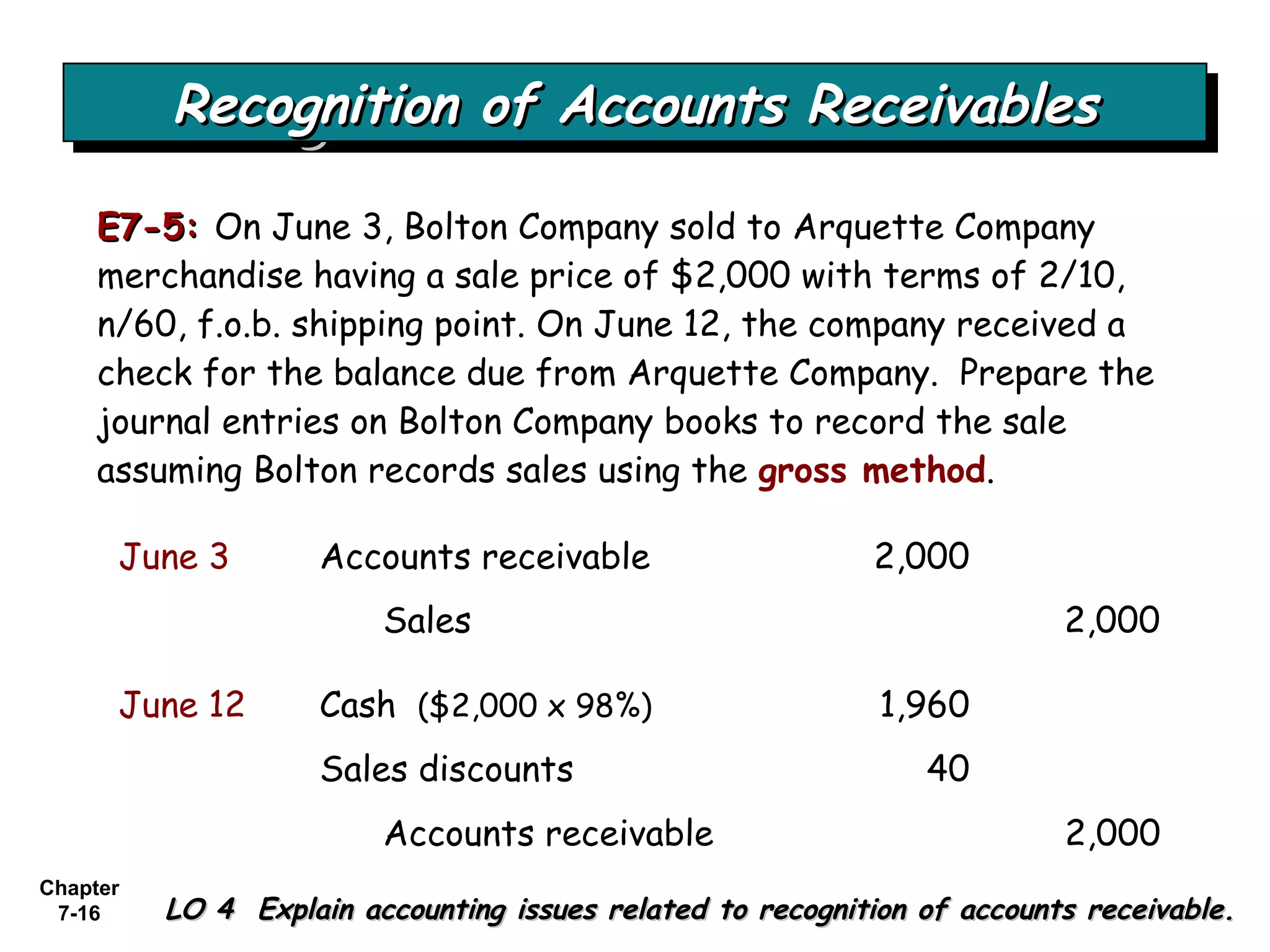

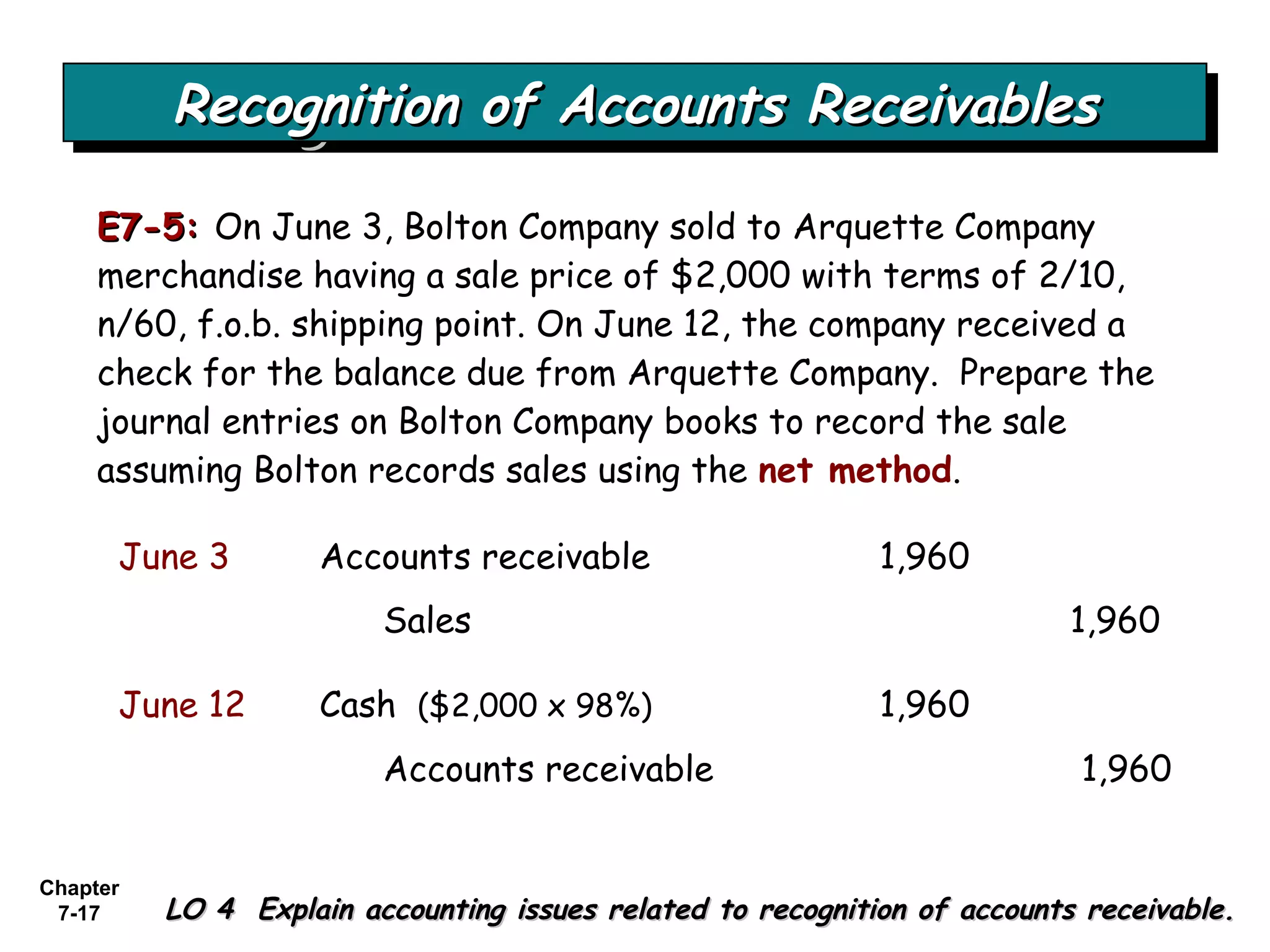

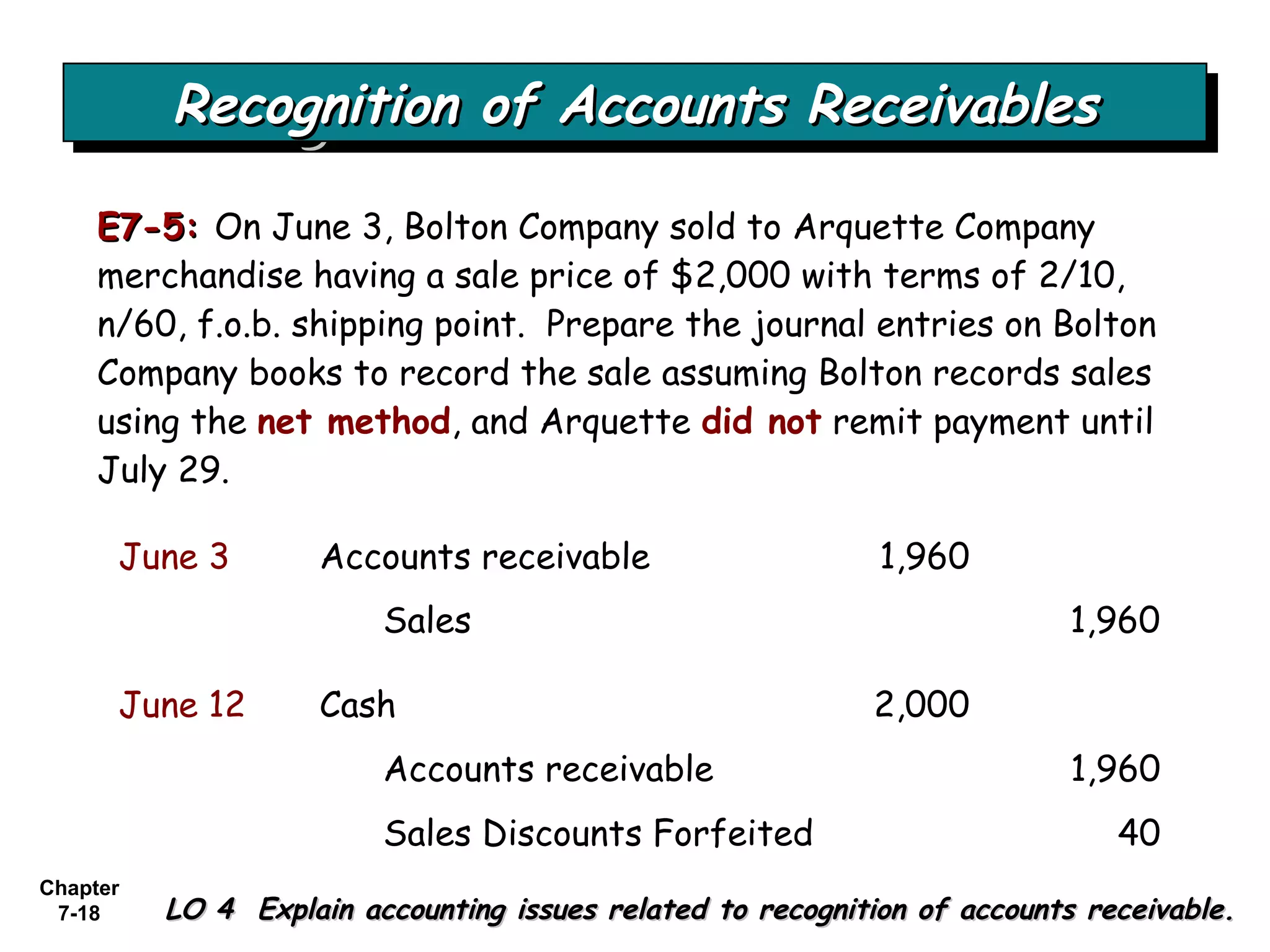

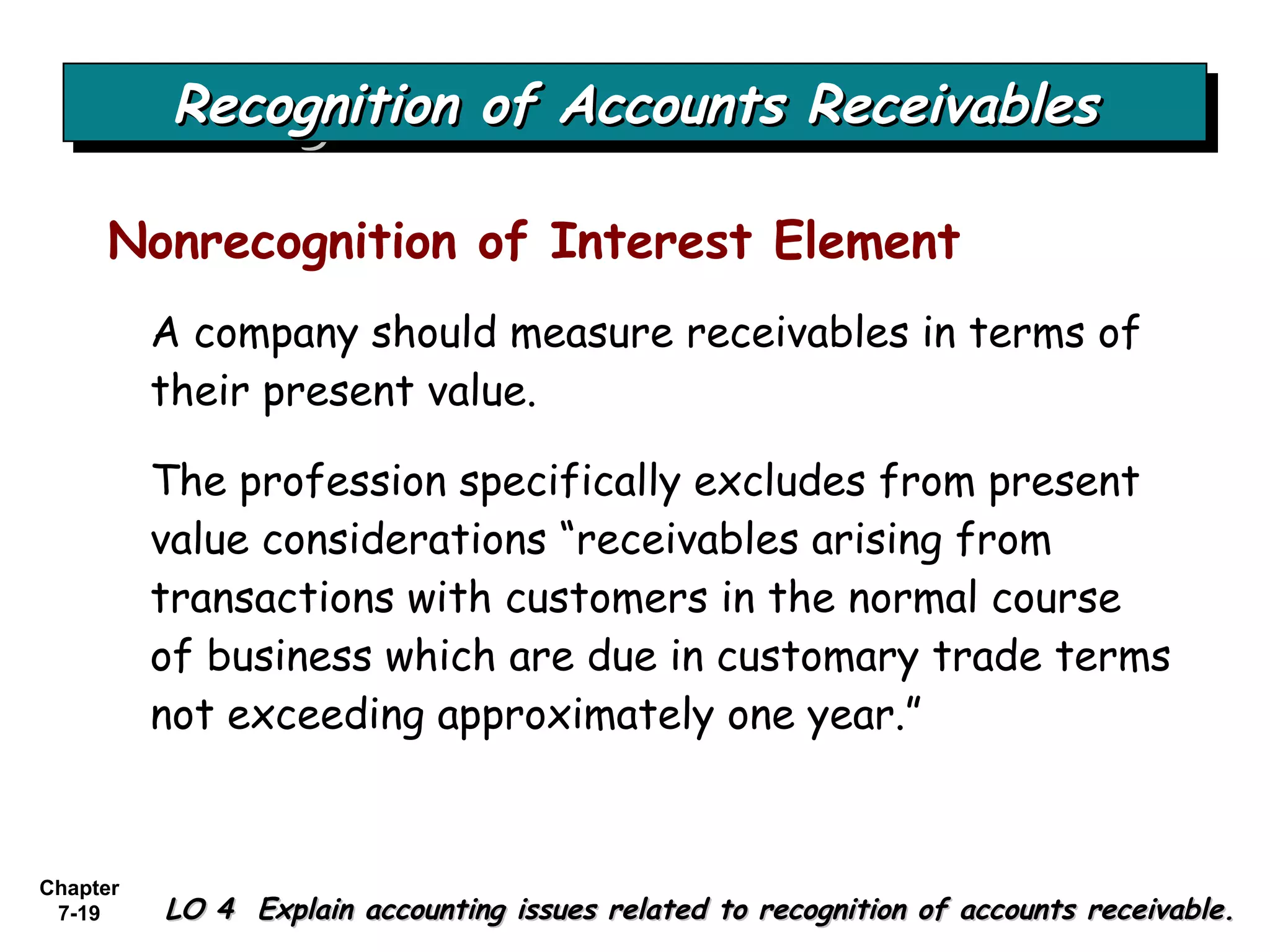

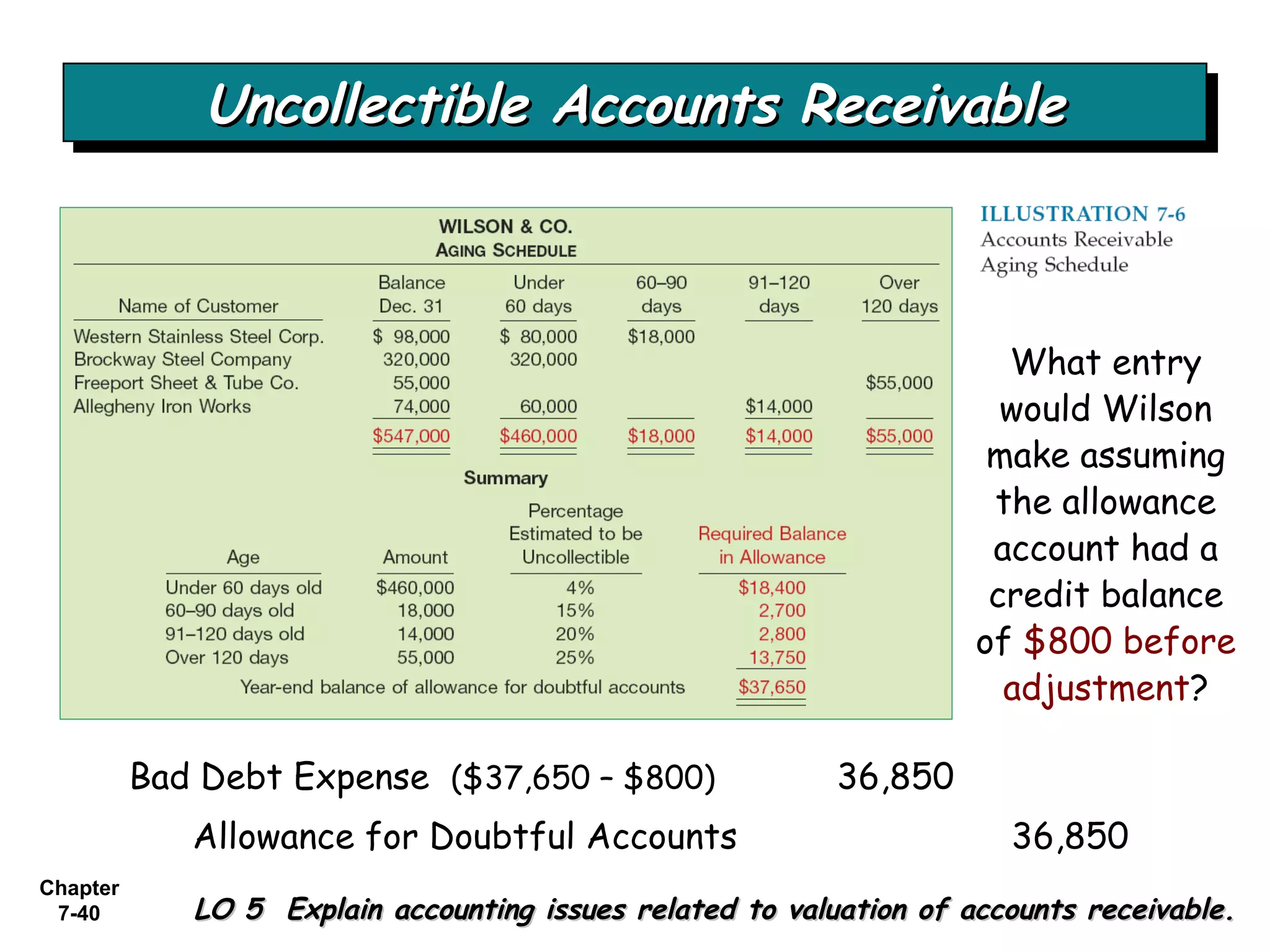

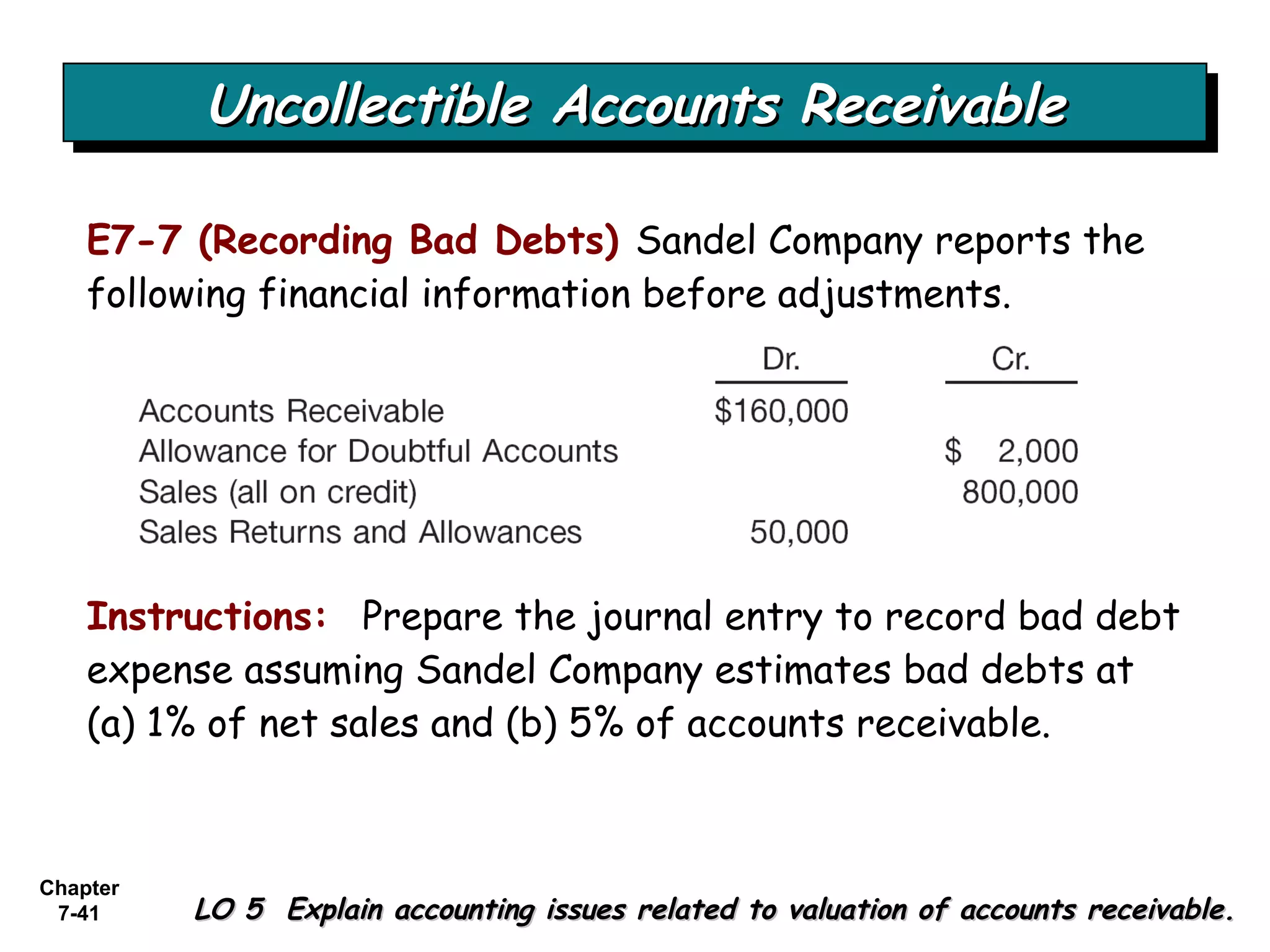

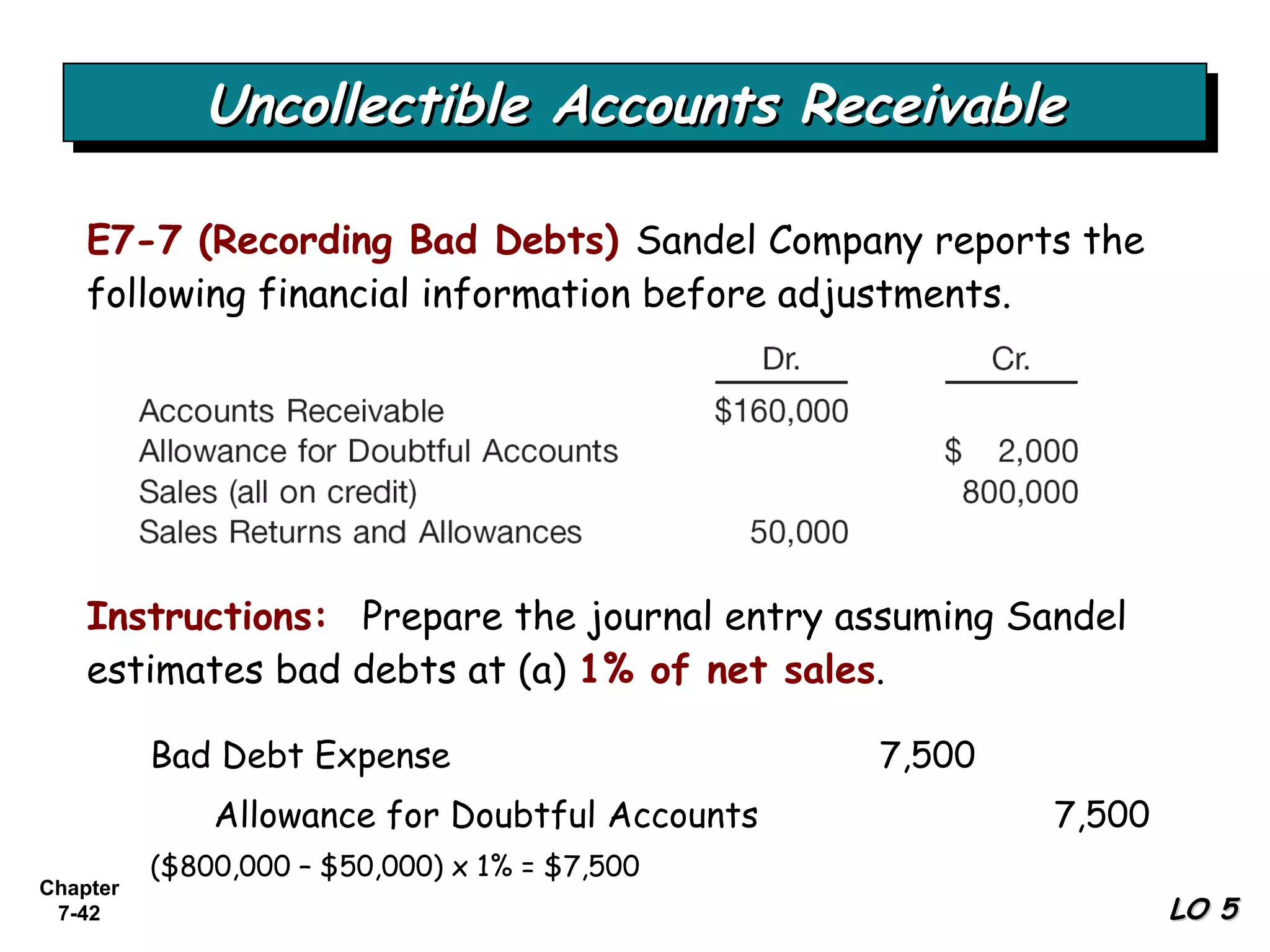

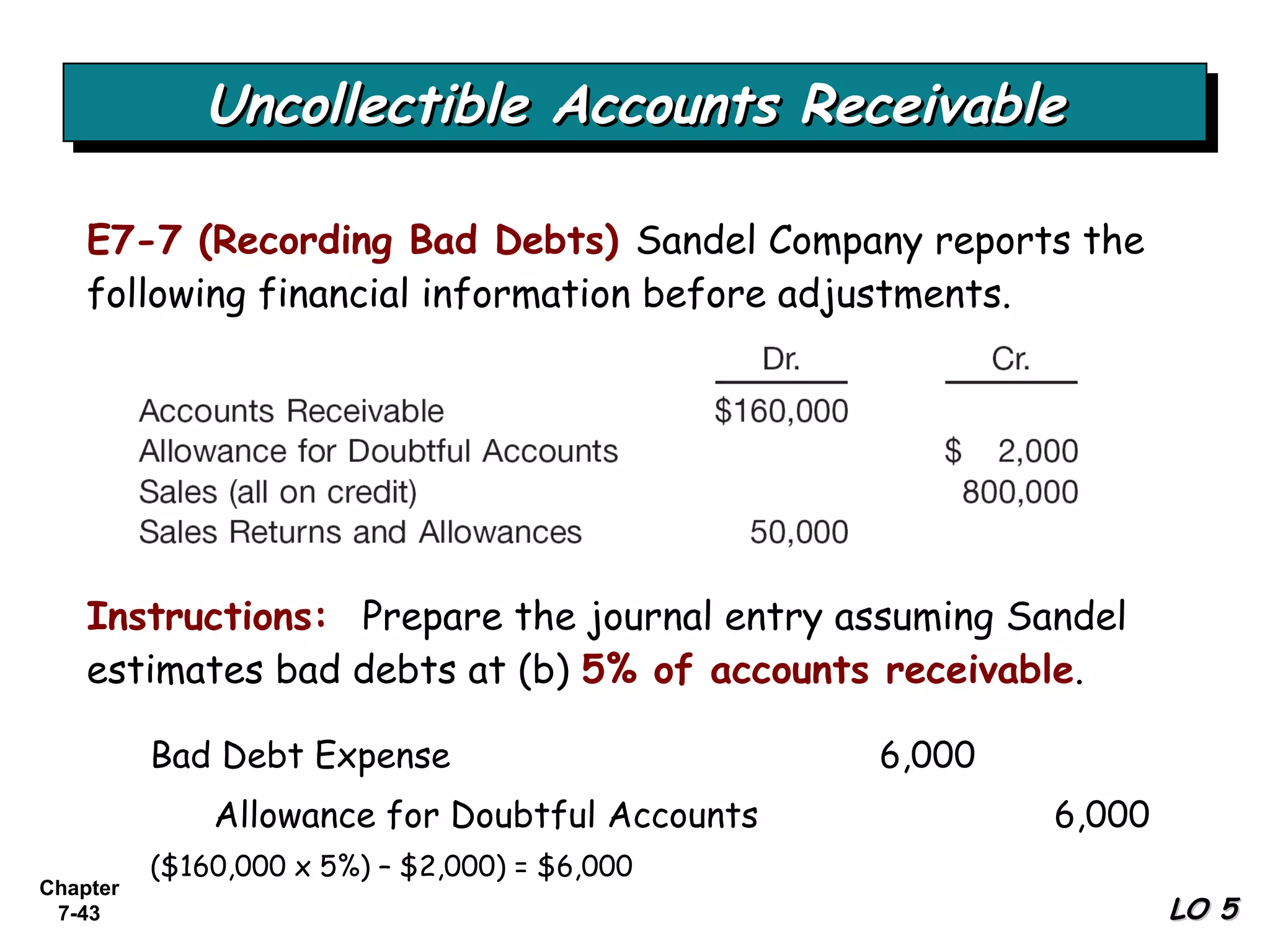

This chapter discusses accounting for cash and receivables. It defines cash as the most liquid asset and identifies items that are considered cash such as currency and bank deposits. Receivables are defined as claims against customers and others for money, goods, or services, and the main types are accounts receivable and notes receivable. The chapter explains the accounting issues around recognition, valuation, and disposition of accounts and notes receivable. It also describes how to report and analyze receivables in financial statements.