Download to read offline

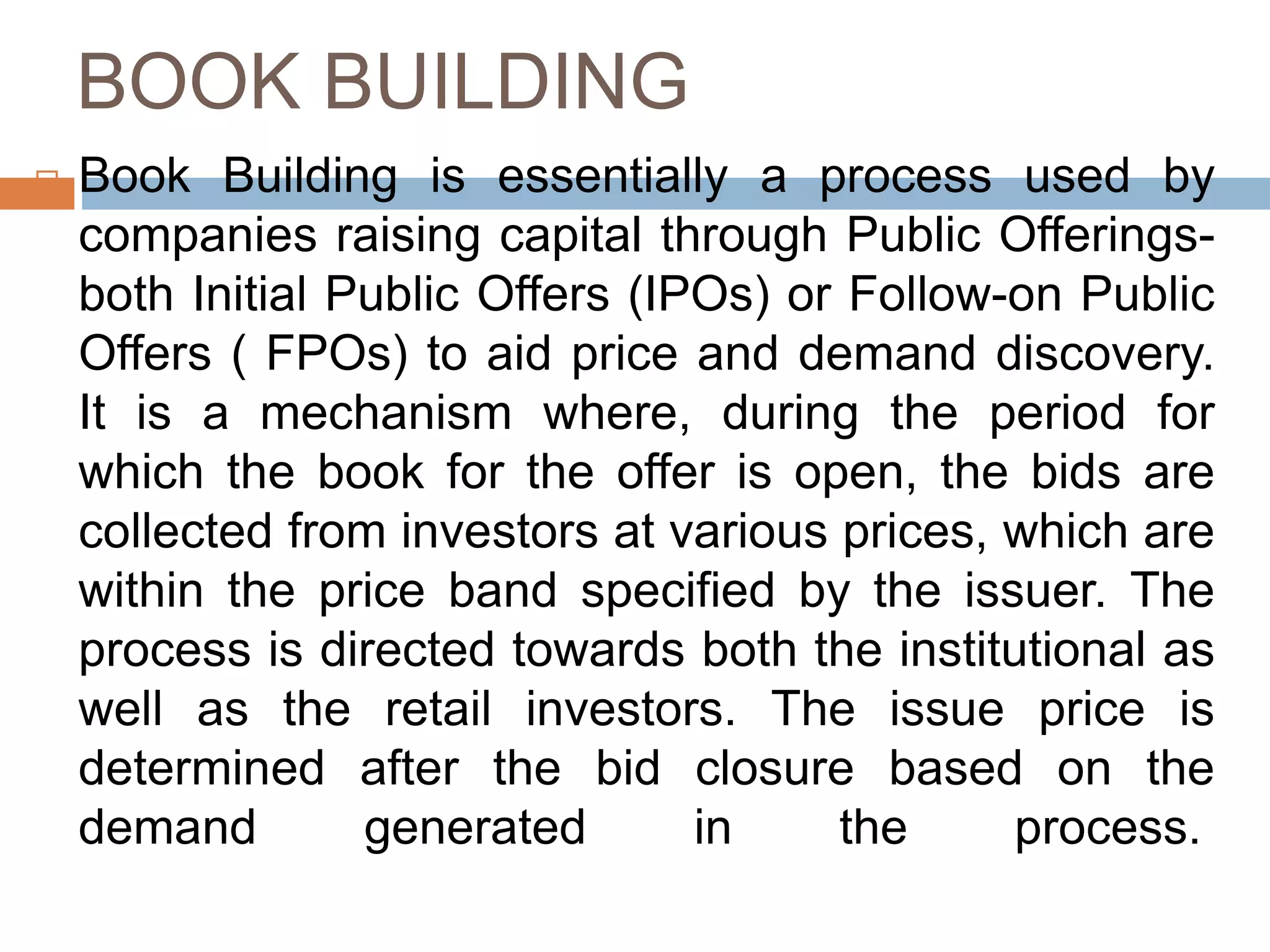

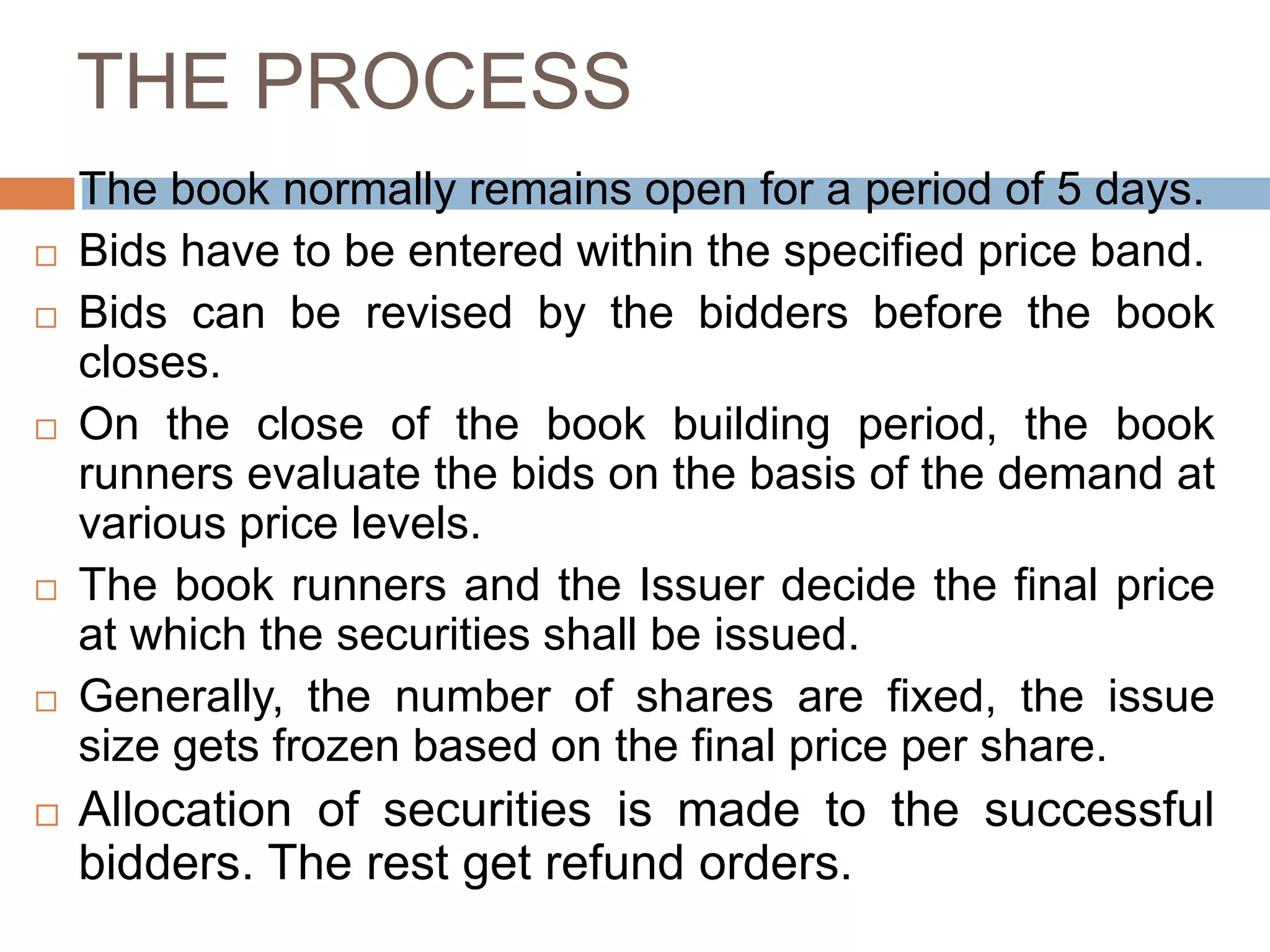

This document discusses book building and fixed price issues for raising capital in the primary market. It describes the two main types of public issues - fixed price issues where the price is known in advance, and book building issues where the price is determined after bidding within a price band. The key aspects of the book building process are outlined, including how bids are collected electronically within a price band over a period of typically 5 days, after which the final issue price is set based on demand. Guidelines for book building from SEBI are also mentioned.