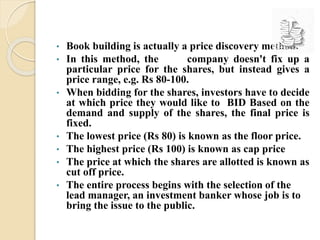

Book building is a process used by underwriters during an initial public offering (IPO) to determine the price of shares to be offered. An underwriter, usually an investment bank, invites institutional investors to submit confidential bids that indicate the number of shares they want to buy and the price they are willing to pay. This allows the underwriter to gauge demand for the shares across different price points to determine an appropriate offer price. Key aspects of book building include setting a price range, collecting bids, and determining the final cut-off price for share allocation based on investor demand. The process aims to set a market-based price and give companies feedback on investor interest and valuation.