Downloaded 26 times

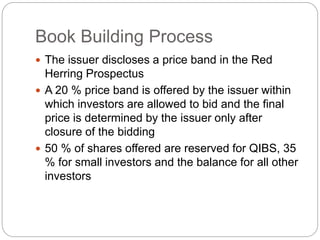

This document provides information about the book building process for issuing securities in India. It defines book building as a process for determining the fair price and quantity of securities to be issued by building demand. The book runner maintains a book of bids from investors and underwriters. SEBI guidelines require at least 25% allocation to retail investors, 25% to non-institutional investors, and 25% to qualified institutional buyers. The final issue price is set based on demand within the disclosed price band.