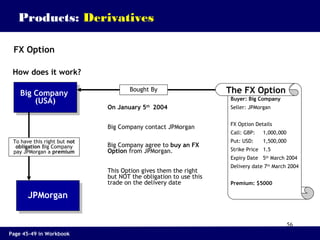

Downloaded 80 times

![21

Capital Markets Overview

Markets – A place where exchange of goods and services happen

Capital Market

•Place where capital (fund) requirements of the issuers are

met; i.e. Issuers (Corporate, Government, etc) raise funds

•Trades in these markets are for debt, equity securities or

other instruments

•Organized, as they are governed by regulatory bodies

[Securities & Exchange Board of India, RBI]](https://image.slidesharecdn.com/bankingquest-151230213123/85/Banking-Training-In-Nepal-21-320.jpg)

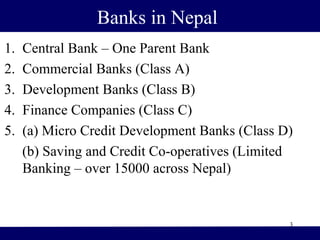

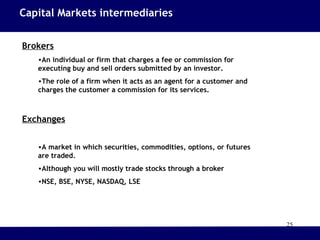

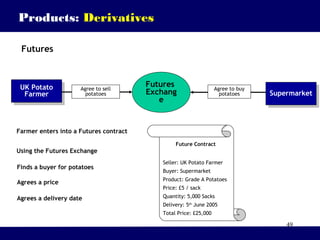

![57

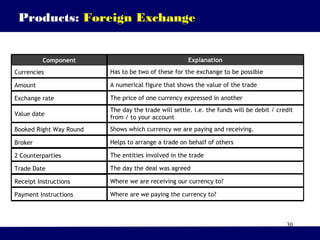

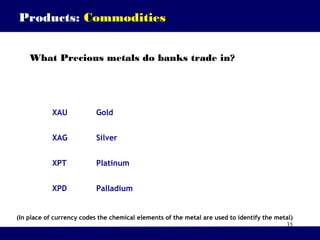

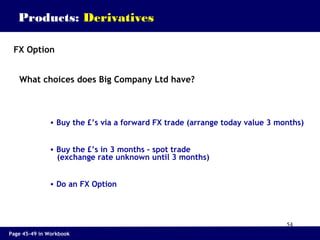

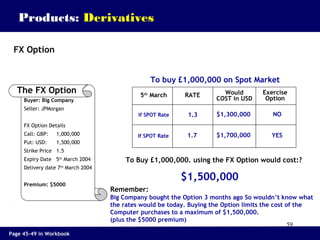

FX Option

Products: Derivatives

Buyer: Big Company

Seller: JPMorgan

FX Option Details

Call: GBP: 1,000,000

Put: USD: 1,500,000

Strike Price 1.5

Expiry Date 5th

March 2004

Delivery date 7th

March 2004

Premium: $5000

Big company now have the right to use [exercise] this trade for settlement on March 7th

The FX Option

What are the key dates?

Expiry Date:

Date that Big Company have to decide whether to exercise the Option

Delivery Date:

Date that transfer of funds would occur if Big Company Ltd

exercise this Option

Other FX Option Components

Call:

Currency that the buyer of the Option would receive

Put:

Currency that the buyer of the Option would sell

Strike:

Exchange Rate that would be used if Option is exercised

Page 45-49 in Workbook](https://image.slidesharecdn.com/bankingquest-151230213123/85/Banking-Training-In-Nepal-57-320.jpg)

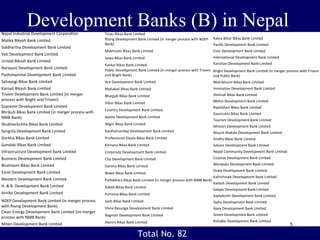

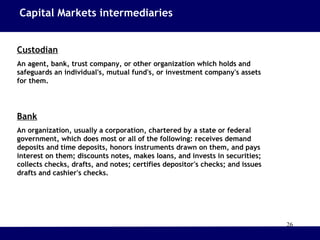

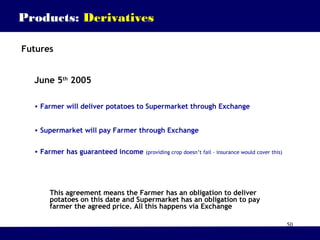

![58

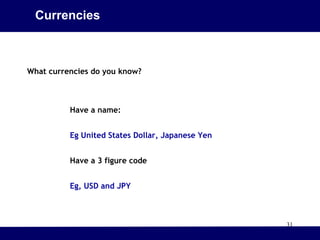

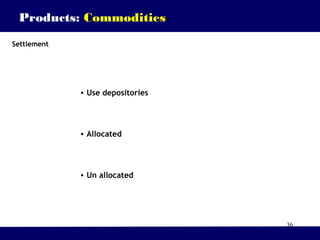

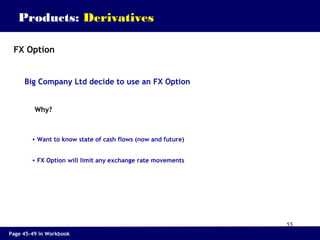

Products: Derivatives

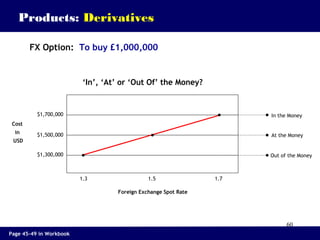

FX Option

Buyer: Big Company

Seller: JPMorgan

FX Option Details

Call: GBP: 1,000,000

Put: USD: 1,500,000

Strike Price 1.5

Expiry Date 5th

March 2004

Delivery date 7th

March 2004

Premium: $5000

The FX Option

How do Big company know whether to exercise the Option?

On 5th

March

• Look at current FX [Spot] rate

• If they used the spot rate (Not the Option Strike rate)

how much would it cost to buy the £1,000,000?

• Would it be cheaper to use the Spot rate and let the

Option expire or…

• Use the Option because the spot price in market would

cost more in USD.

Lets look at possible choices Big Company Could make

Page 45-49 in Workbook](https://image.slidesharecdn.com/bankingquest-151230213123/85/Banking-Training-In-Nepal-58-320.jpg)

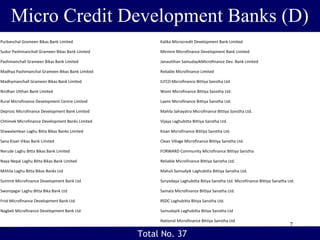

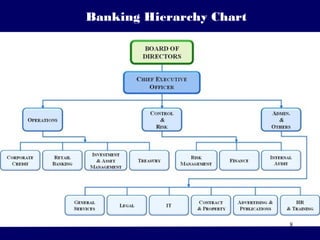

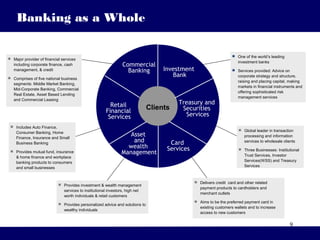

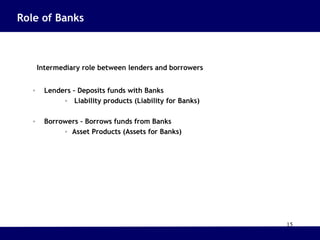

This document provides an overview of the banking system in Nepal. It begins by explaining the purpose of banks and then outlines the different types of banks in Nepal, including central banks, commercial banks, development banks, finance companies, and microcredit development banks. A total of 30 commercial banks, 82 development banks, 48 finance companies, and 37 microcredit development banks currently operate in Nepal. The document also includes organizational charts of the banking hierarchy and describes some of the key roles and services provided by banks, such as accepting deposits, lending money, remittances, safe deposit services, and capital market activities.