Downloaded 67 times

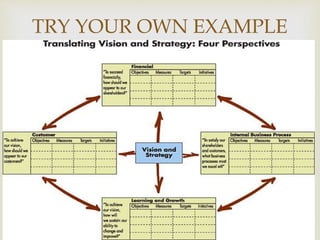

The document discusses the balanced scorecard concept proposed by Robert Kaplan and David Norton in 1992 as an alternative to only measuring managerial control through financial metrics. The balanced scorecard model suggests organizations view their performance through four perspectives: financial, customer, internal business processes, and learning and growth. By developing metrics in each of these areas and analyzing performance, managers can gain a more well-rounded understanding of organizational success beyond just financial measures.