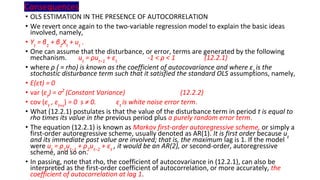

This document discusses autocorrelation and its consequences. Autocorrelation occurs when error terms in a time series regression model are correlated over time. This violates the classical linear regression assumption that error terms are independent. If autocorrelation is present, it can bias standard error estimates and invalidate statistical tests. The document outlines various causes of autocorrelation like inertia in time series data, omitted variables, incorrect functional form, lags, and data manipulation. It also discusses the consequences of autocorrelation like biased standard errors and underestimated variance estimates. Methods to detect autocorrelation graphically and through statistical tests like runs tests are presented.

![THE NATURE OF THE PROBLEM

• Autocorrelation may be defined as “correlation between members of series

of observations ordered in time [as in time series data] or space [as in

cross-sectional data].’’ the CLRM assumes that:

• E(ui

uj

) = 0 i ≠ j (3.2.5)

• Put simply, the classical model assumes that the disturbance term relating

to any observation is not influenced by the disturbance term relating to any

other observation.

• For example, if we are dealing with quarterly time series data involving the

regression of output on labor and capital inputs and if, say, there is a labor

strike affecting output in one quarter, there is no reason to believe that this

disruption will be carried over to the next quarter. That is, if output is lower

this quarter, there is no reason to expect it to be lower next quarter.

• Similarly, if we are dealing with cross-sectional data involving the

regression of family consumption expenditure on family income, the effect

of an increase of one family’s income on its consumption expenditure is not

expected to affect the consumption expenditure of another family.](https://image.slidesharecdn.com/autocorrelation-230814135130-658e338a/85/auto-correlation-pdf-3-320.jpg)

![Now let. N = total number of observations = N1 + N2

N1 = number of + symbols (i.e., + residuals)

N2 = number of − symbols (i.e., − residuals)

R = number of runs=(3)

Note: N = N1 + N2.

The null hypothesis is randomness or no auto correlation; if R (= 3) is outside the range, we rejec

the null hypothesis that ut

is random. if R (= 3) is within the range value, we can not reject the nu

hypothesis

so that ut

is not-random or ut

follow some pattern.

Prob [E(R) − 1.96σR ≤ R ≤ E(R) + 1.96σR] = 0.95 (12.6.3)](https://image.slidesharecdn.com/autocorrelation-230814135130-658e338a/85/auto-correlation-pdf-23-320.jpg)

![Using the formulas given in (12.6.2), we obtain

The 95% confidence interval for R in our example is thus: As our R (=3) is out side the

range, We can not reject the null hypothesis. So, we can suggest that there is

auto-correlation.

[10.975 ± 1.96(3.1134)] = (4.8728, 17.0722)](https://image.slidesharecdn.com/autocorrelation-230814135130-658e338a/85/auto-correlation-pdf-24-320.jpg)