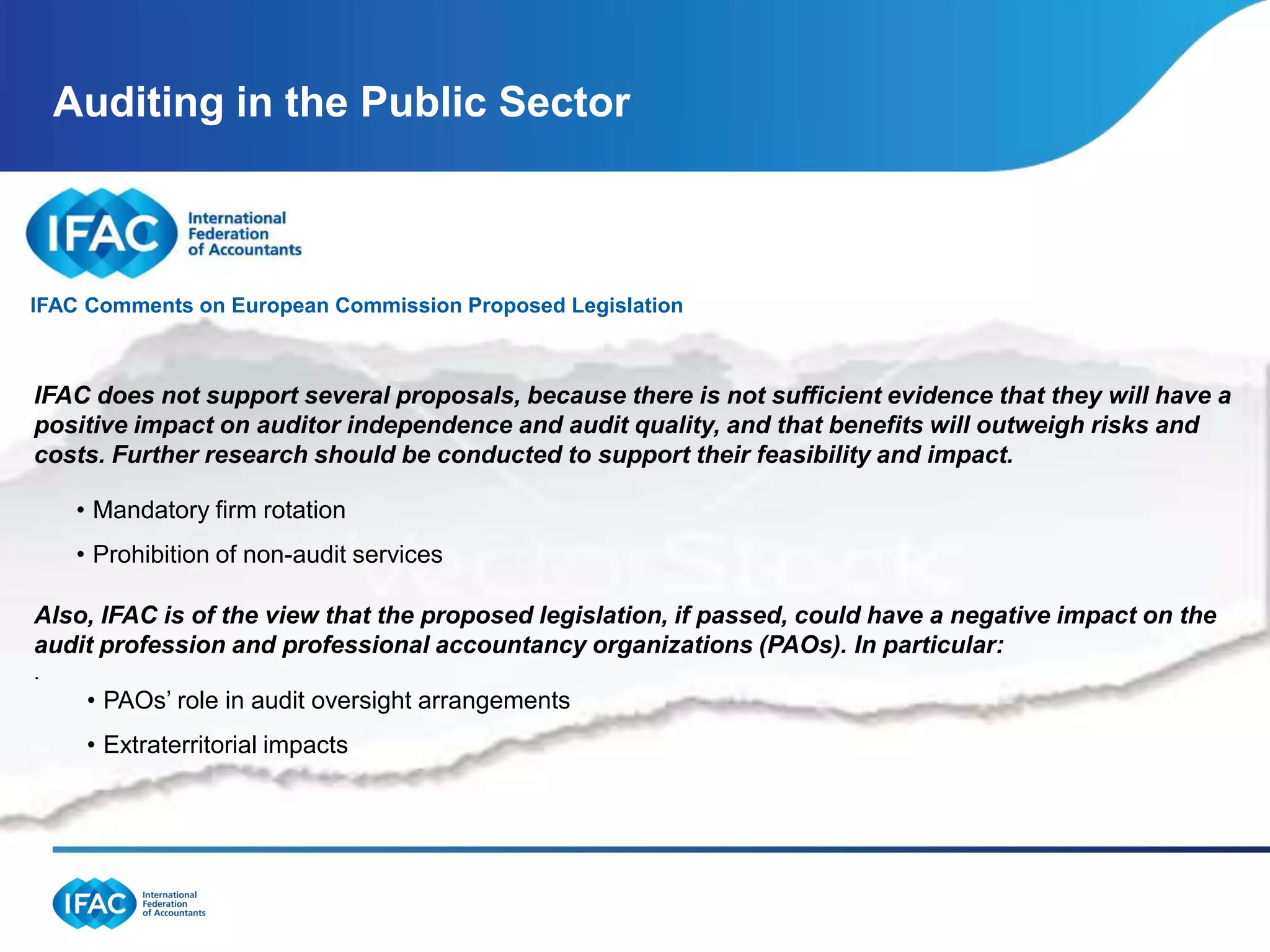

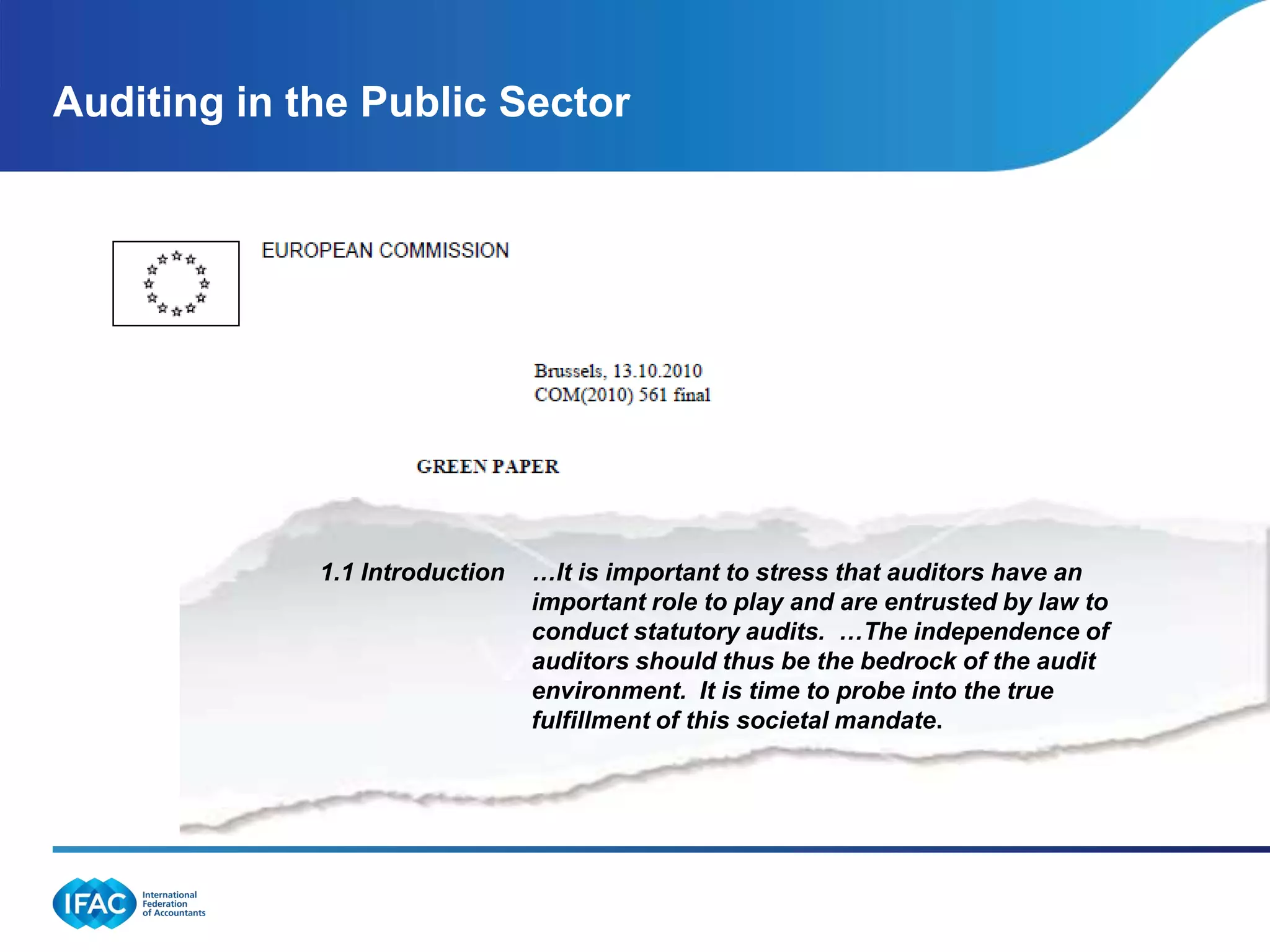

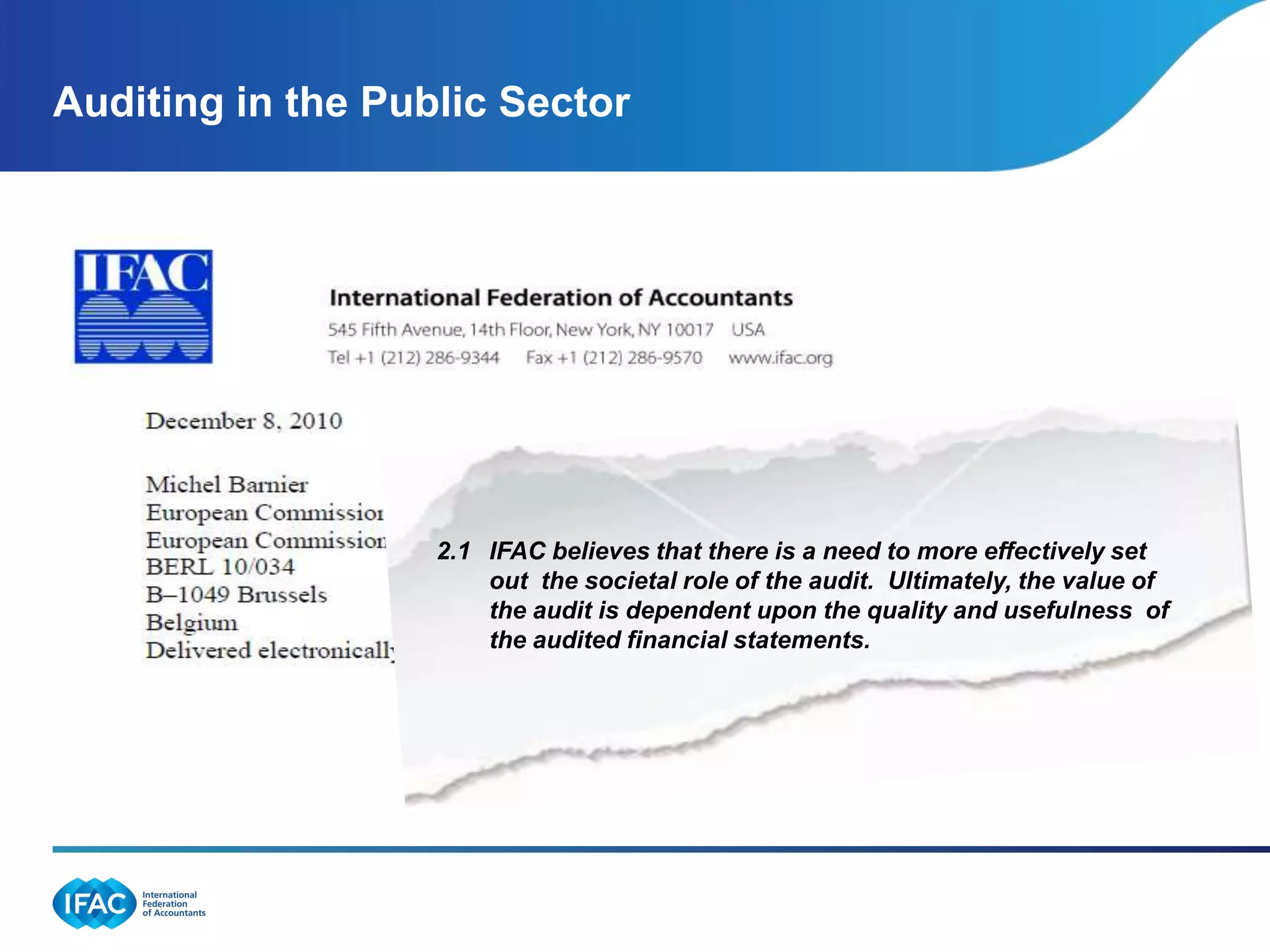

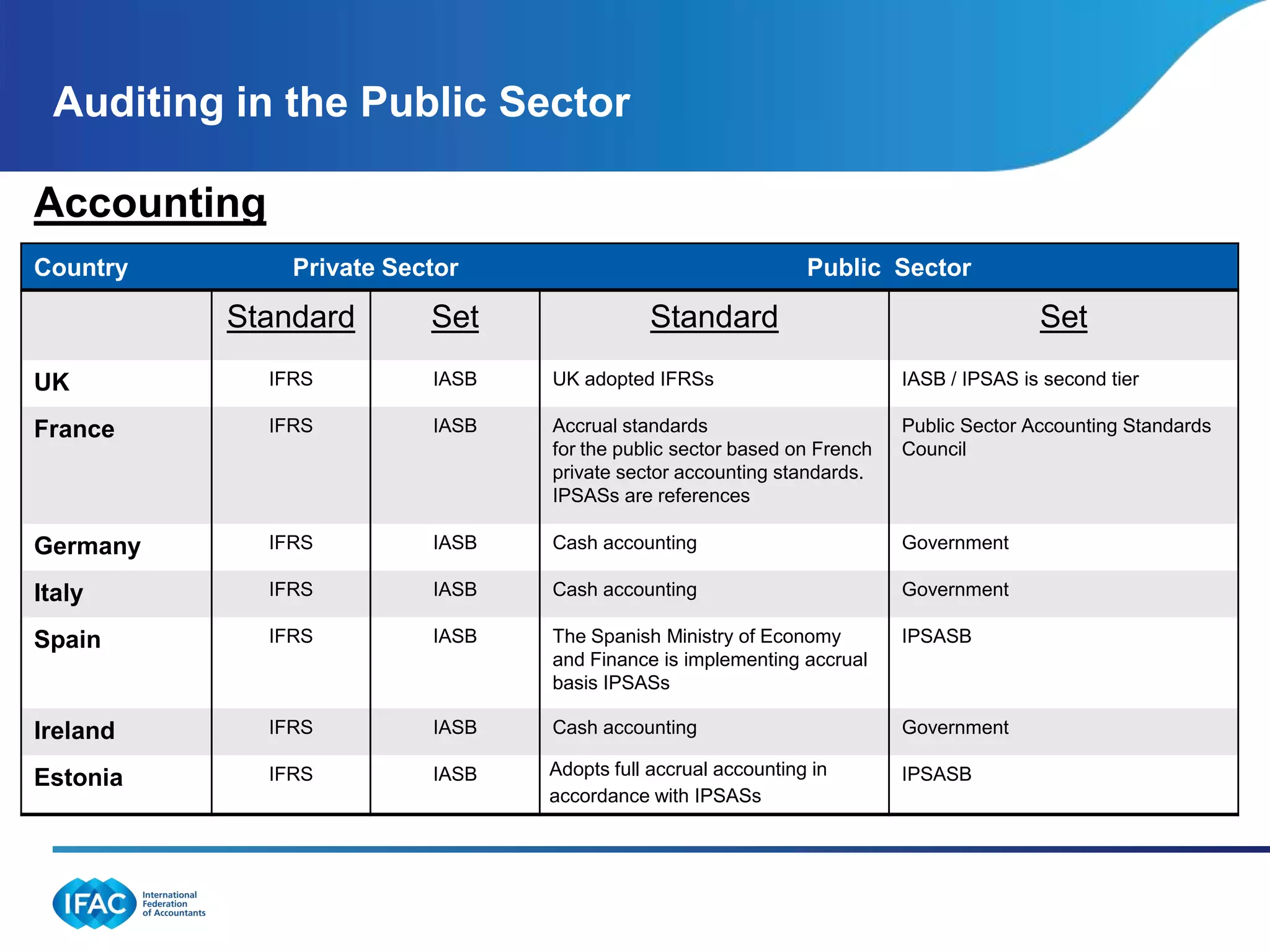

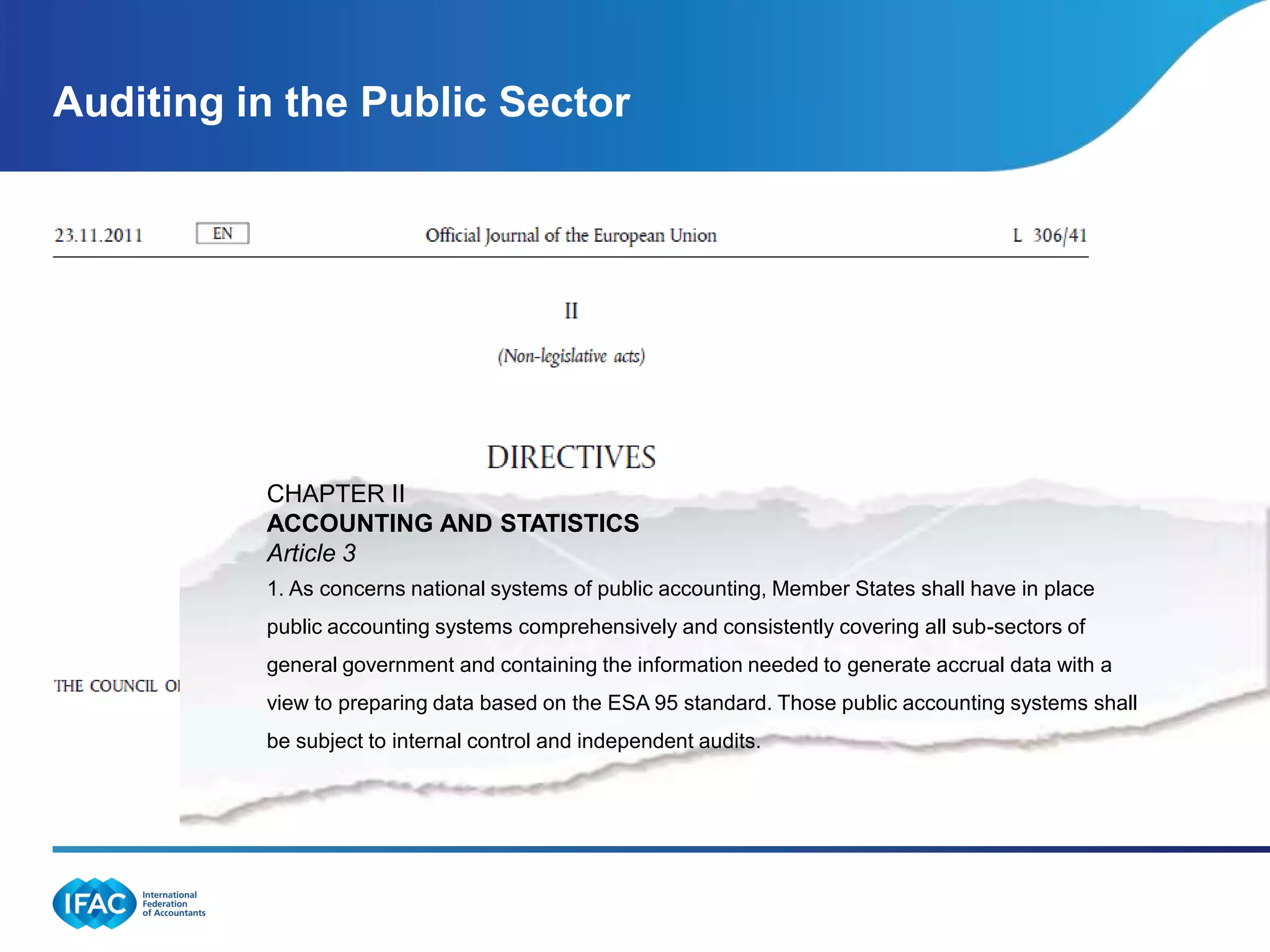

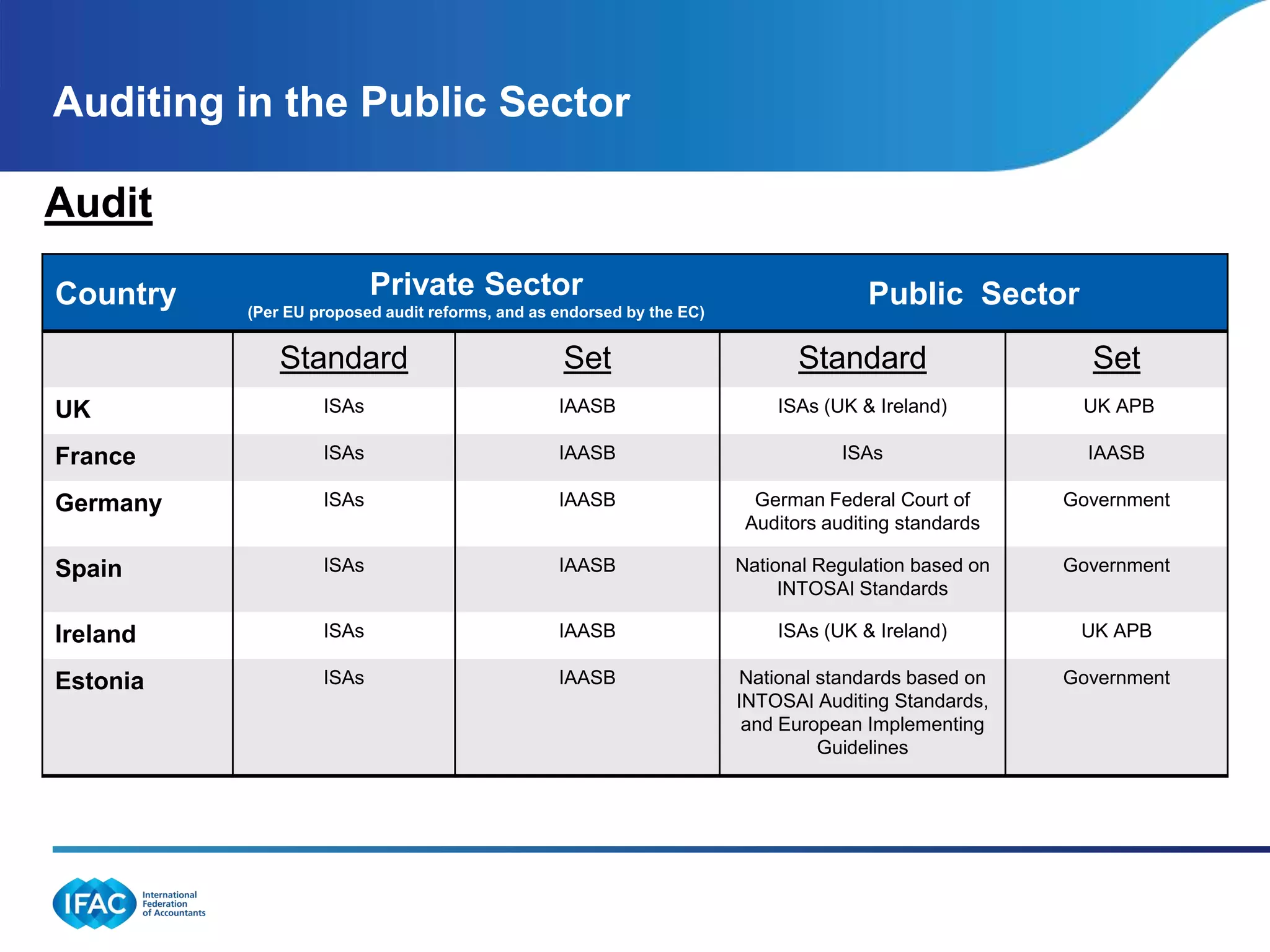

The International Federation of Accountants (IFAC) submitted comments on the European Commission's proposed legislation regarding auditing in the public sector, emphasizing support for initiatives aimed at improving audit quality and safeguarding auditor independence. IFAC expressed concerns that some proposed measures could negatively impact the audit profession, particularly issues related to auditor independence and the role of professional accountancy organizations. The organization advocates for enhanced dialogue between auditors and regulators, greater transparency in auditor selection, and mandates for the adoption of international standards for public sector accounting.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)