Downloaded 25 times

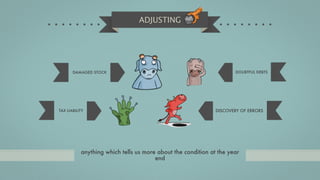

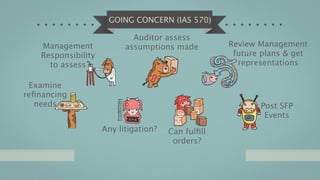

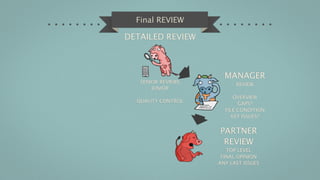

The document discusses the procedures for completing an audit, including initial engagements, comparative information, other information, post statement of financial position events, going concern considerations, and final procedures. It covers assessing opening balances and prior year adjustments in initial engagements, compliance with financial reporting frameworks and treatment of prior period adjustments in comparatives. It also addresses identifying inconsistencies in other information, adjusting and non-adjusting post-statement of financial position events, evaluating management's going concern assessment, and risk indicators.

![Approach note on internal audit [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/approachnoteoninternalauditcompatibilitymode-130407035746-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)