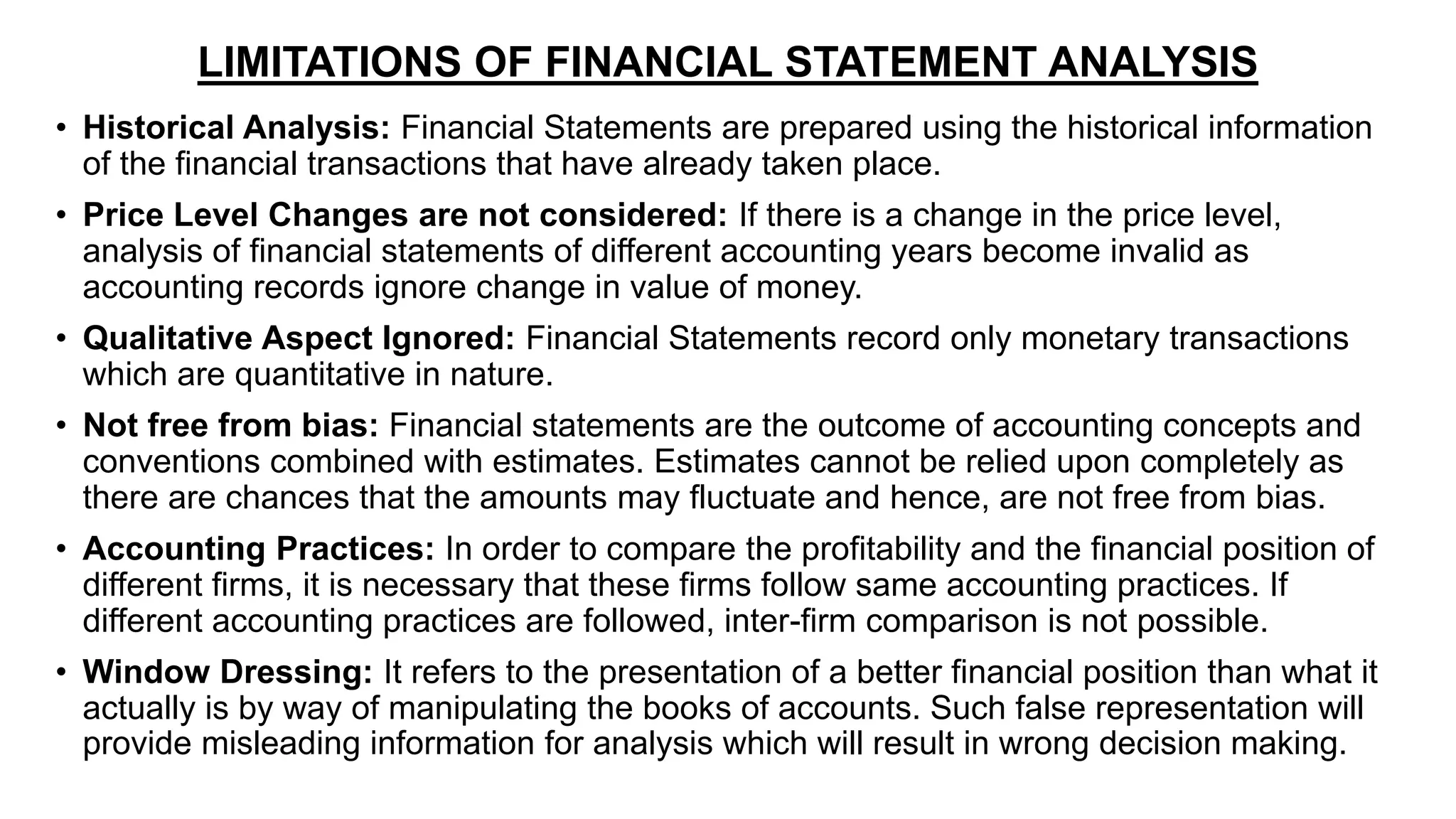

This document provides an overview of interpreting financial statements. It defines financial statement analysis and interpretation, and explains that analysis involves simplifying data through classification while interpretation explains the meaning and significance of the data. The document outlines objectives of analysis including assessing profitability, efficiency, and solvency, and discusses tools used like comparative statements, common size statements, ratio analysis, and trend analysis. It also covers limitations of analysis and importance of comparative statements.