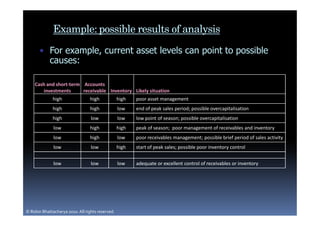

Financial analysis provides stakeholders with an external view of a company's financial health and outlook based on its financial reports and statements. Key financial issues are highlighted and potential risks and benefits identified. Ratio and trend analysis against industry standards can reveal strengths or weaknesses that may impact profitability or require management attention. The results of financial analysis may indicate areas for further operational or strategic analysis and improve a company's financial efficiency.