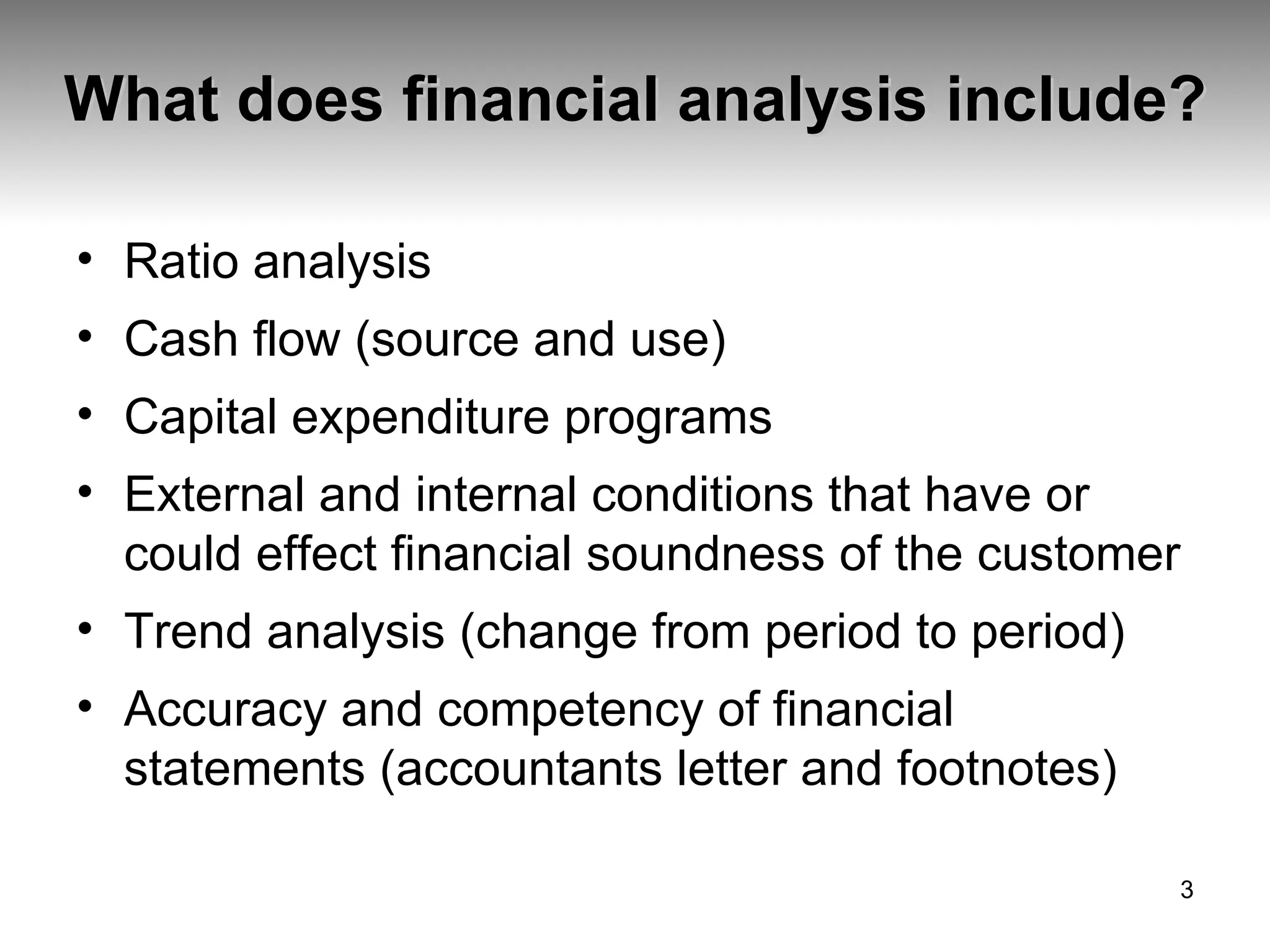

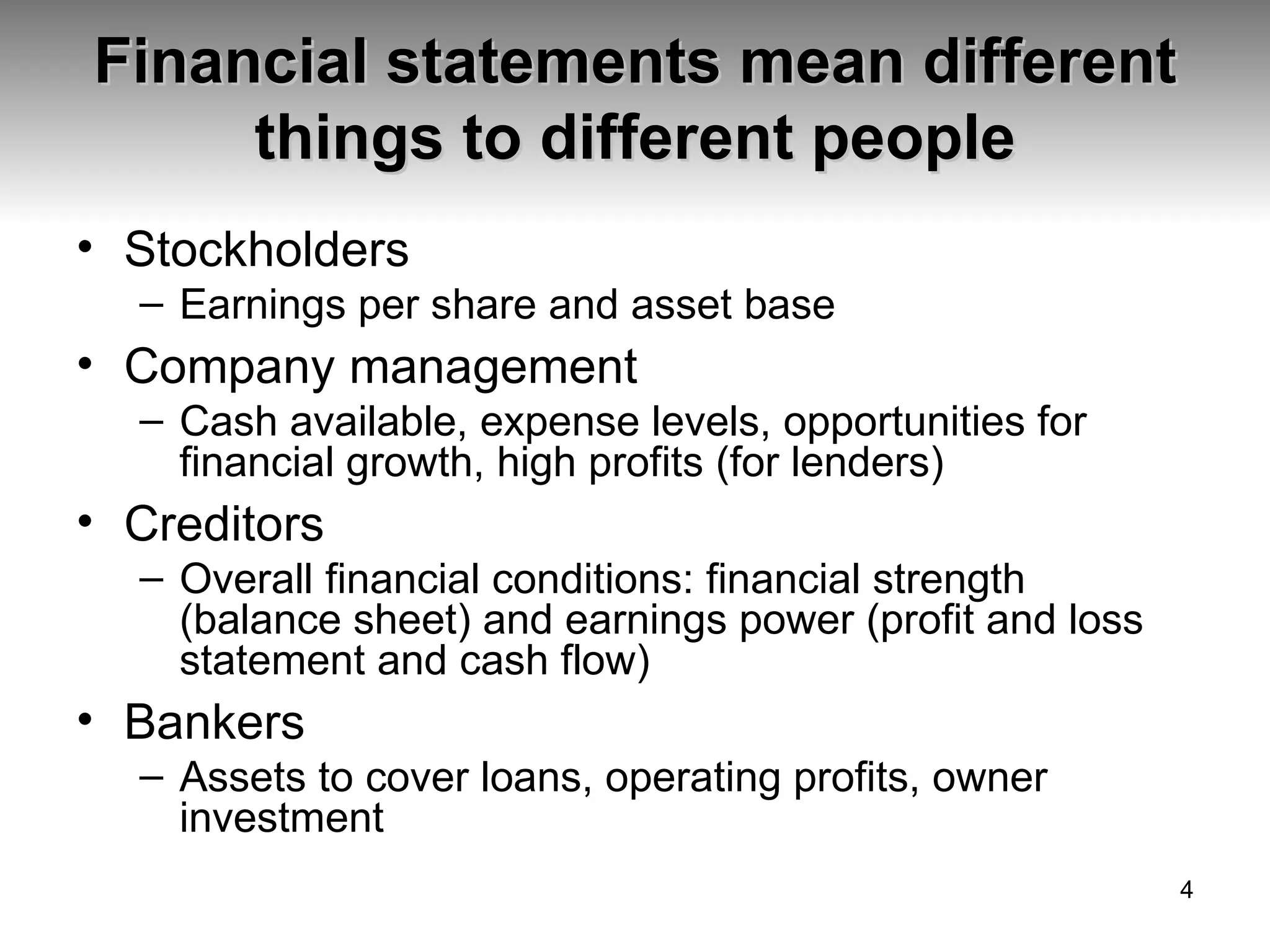

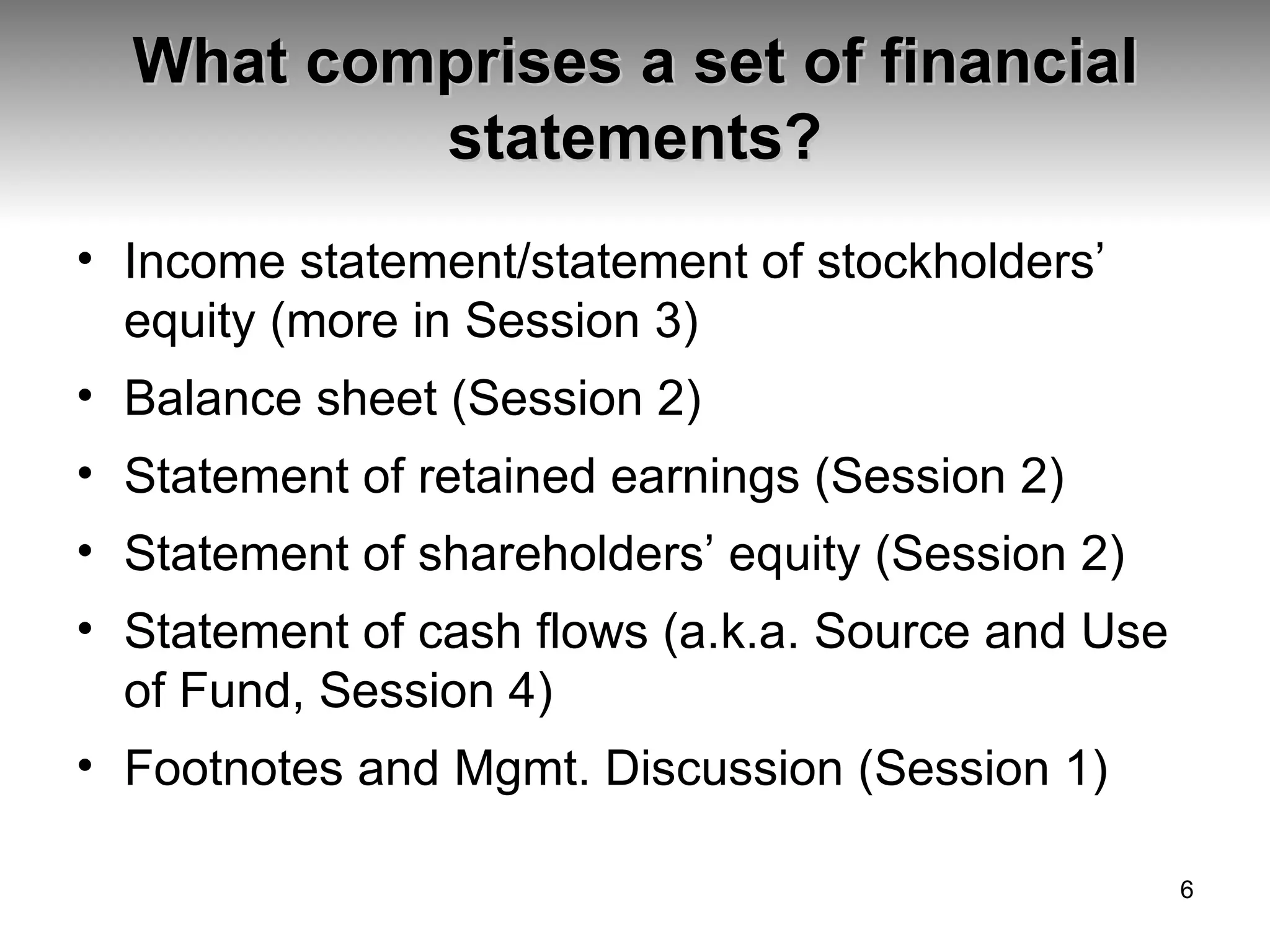

This document provides an overview of financial statement analysis, including: 1) Financial statements form the basis for understanding a business's financial position and assessing historical and prospective performance. 2) Financial analysis includes ratio analysis, cash flow analysis, and trend analysis to understand a business's financial soundness from different perspectives. 3) Financial statements have different meanings and uses for various stakeholders like stockholders, management, creditors, and bankers.