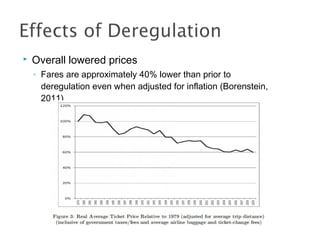

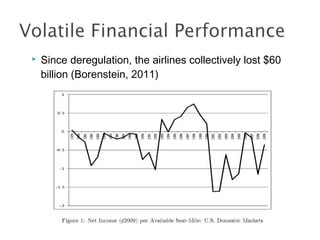

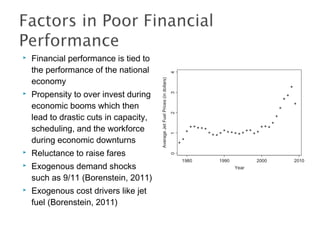

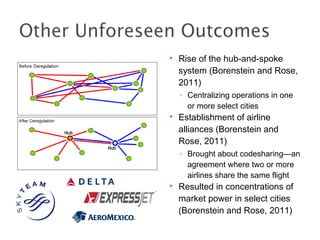

The document discusses the deregulation of the airline industry in the United States. It provides background on the history of airline regulation and the role of the Civil Aeronautics Board. Deregulation began in 1978 with the Airline Deregulation Act and aimed to lower prices and reduce barriers to entry. While deregulation succeeded in lowering airfares, the airline industry has struggled financially since losing over $60 billion collectively. Airlines must invest more moderately, improve labor relations to enhance customer service, and raise prices to achieve financial sustainability.