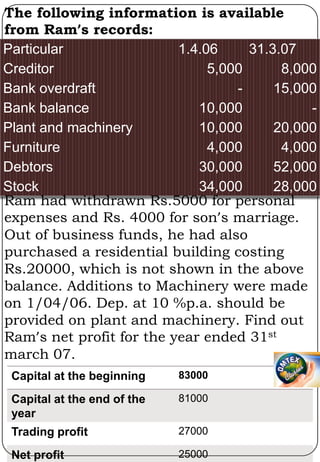

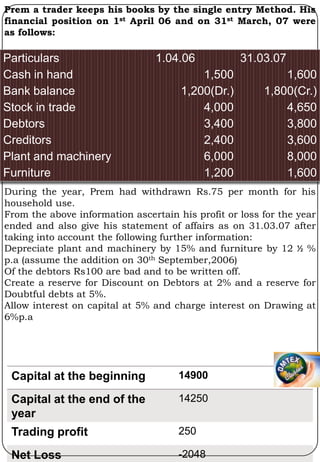

Downloaded 210 times

![Mr. Prabhakar is a retail trader. He had no proper methods of

accounting. But the following information is made available to

you. [March 2012]

Particulars

Amount Rs.

1.4.2009

Sundry Debtors

Sundry Creditors

Bank Overdraft

Stock

Cash in hand

Bills Receivable

Furniture

Motor van

Computer

10% Govt. Bonds

Amount Rs.

31.3.2010

45000

60000

80000

65000

2000

60000

10000

80000

60000

50000

70000

40000

80000

8000

80000

10000

80000

120000

10000

Adjustments.

On 1st October, 2009 Mr. Prabhakar had withdrawn Rs. 40000 for

his personal use. 10% Government Bonds were purchased of Rs.

10,000 on 1st October, 2009. He had also withdrawn Rs. 30000 for

his daughter’s marriage. Depreciate furniture by 10% and write off

Rs. 2000 from motor van. Rs. 2000 is written off as bad debts and

provide 5% R.D.D. on debtors. Allow interest on capital at 10%

p.a. Charge interest on drawings Rs. 2,000.

Prepare after taking into consideration the adjustments.

Opening statement of affairs of 1.4.2009.

Closing statement of affairs of 31.3.2010.

Statement showing Profit or Loss for the year ended on 31.3.2010.

Capital at the beginning

182000

Capital at the end of the

year

328000

Trading profit

216000

Net profit

192900](https://image.slidesharecdn.com/singleentryaccountingsystem-140125044819-phpapp01/85/Single-entry-accounting-system-7-320.jpg)

Mr. Raj's records from March 2006 to March 2007 are presented using a single entry system. Depreciation is to be provided for plant and machinery and furniture. Statements of affairs as of March 2006 and March 2007 and a statement of profit and loss for the year ended March 2007 are to be prepared. Capital decreased from Rs. 116,900 to Rs. 114,700 while trading profit was Rs. 8,800 and net profit was Rs. 3,325.