Downloaded 57 times

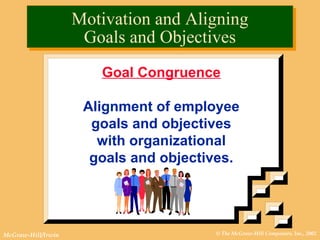

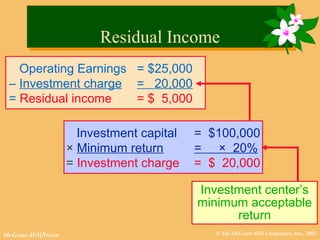

This document discusses various performance measurement and compensation systems for businesses. It covers topics like goal congruence, feedback, return on investment, residual income, economic value added, balanced scorecards, and components of management compensation like salary, bonuses, profit sharing, and stock options. The key themes are how to align employee and company goals, measure performance, and reward performance in a way that maximizes shareholder value.