Downloaded 36 times

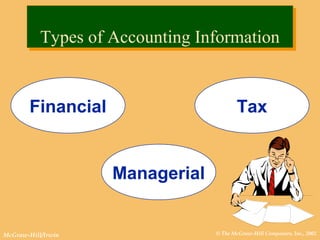

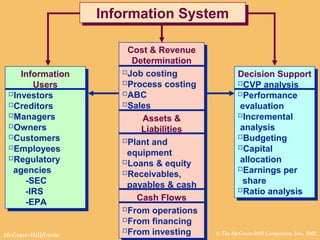

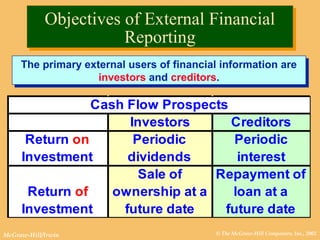

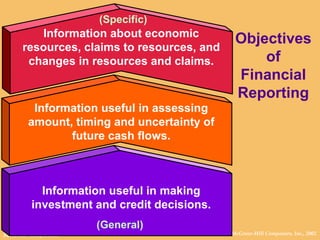

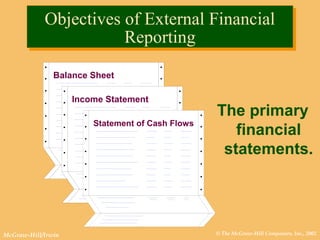

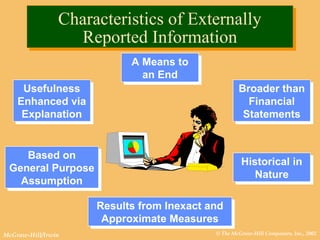

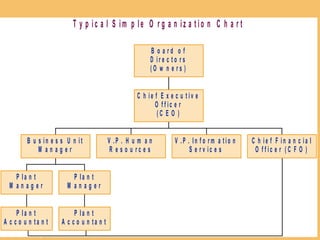

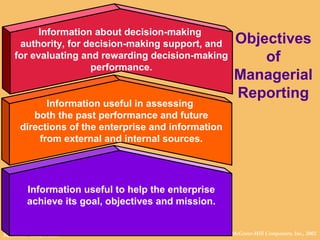

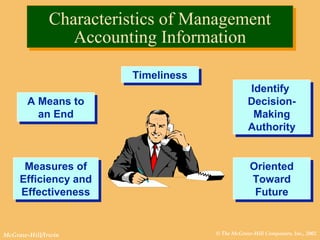

This document discusses accounting information and its uses. It explains that accounting links decision makers with economic activities and results. There are three main types of accounting: financial, managerial, and tax accounting. Accounting information has both external users like investors and creditors, and internal users like managers and owners. The objectives of financial reporting are to provide information about resources, claims on resources, and cash flows to help investors and creditors make decisions. Managerial accounting objectives are to provide information about decision making, performance evaluation, and helping the enterprise achieve its goals.