Download to read offline

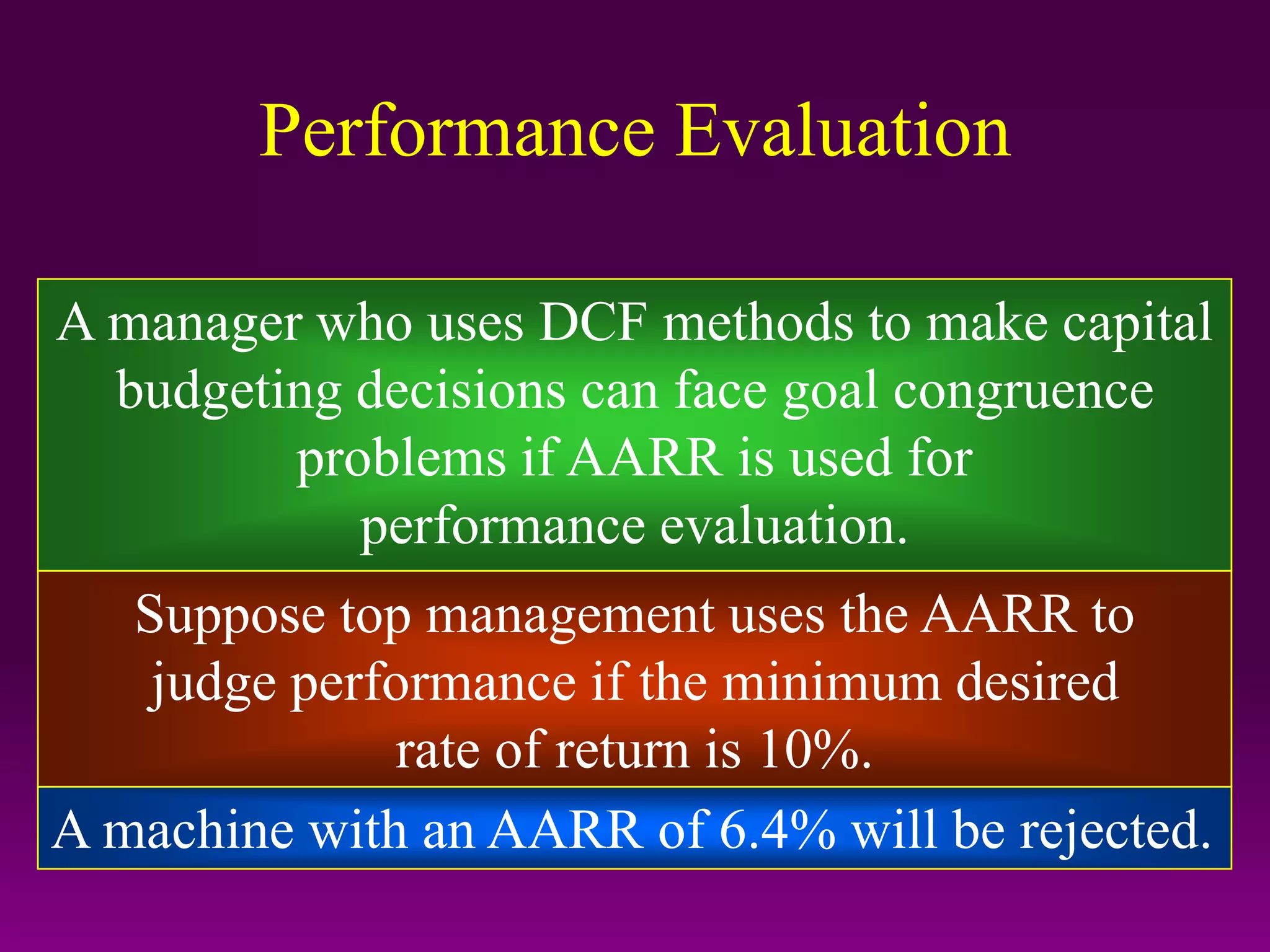

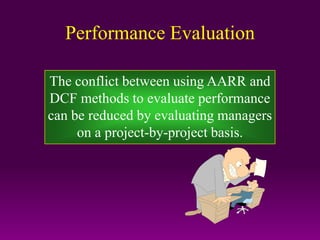

A manager using discounted cash flow methods for capital budgeting can face conflicts if accounting rate of return is used for performance evaluation. Specifically, a project with an accounting rate of return below the desired minimum threshold will be rejected, even if it has a positive net present value using discounted cash flow methods. This goal incongruence can be reduced by evaluating managers' performance on a project-by-project basis instead of using accounting rate of return.